Throughout much of last year, critics of the White House darkly warned that “Trump sabotage” of Obamacare would result in steep increases in premiums for Obamacare plans.

They predicted that Congress’ repeal of the tax penalty on the uninsured, coupled with an administration rule lifting federal restrictions on short-term policies, would lead to double-digit premium increases in 2019.

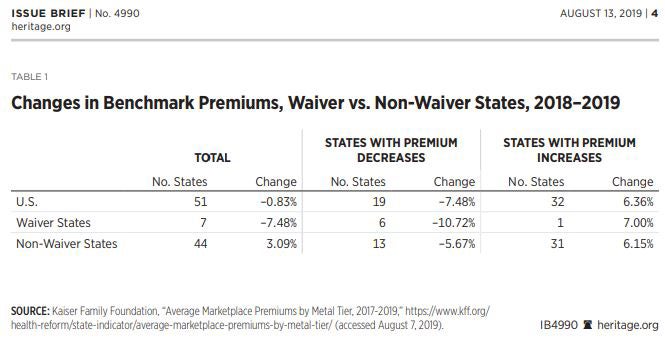

The good news is that none of that has happened. To the contrary, average premiums for “benchmark” plans—policies whose premiums are used in calculating premium subsidies—declined slightly (0.83%) in 2019, for the first time in the program’s history.

The better news is that this overall decline was driven by seven states (Alaska, Maine, Maryland, Minnesota, New Jersey, Oregon and Wisconsin) that obtained waivers to deviate from certain Obamacare mandates.

Premiums in those states fell by a median of 7.48%, while premiums in the other 44 states and the District of Columbia rose by a median of 3.09% (see chart).

The message for policymakers is clear: Innovation by states is the key to more affordable health insurance.

How Obamacare Waivers Work

Section 1332 of the Obamacare statute permits states to seek waivers from certain federal health insurance regulatory requirements.

States can obtain waivers to tap federal money that the government would otherwise have transferred directly to insurance companies as premium subsidies and use that money instead to pursue innovative reforms.

Those arrangements must be budget neutral to the federal government.

The waivers that have been granted most commonly are for risk-stabilization programs. Although these programs vary from state to state, they follow the same general pattern: States blend federal premium-subsidy money with funds from non-federal sources to create a fund that helps pay claims for policyholders at risk of incurring high medical bills.

States must submit actuarial analyses showing that their arrangements would not increase federal spending.

Waivers Are Working

Premiums for benchmark plans in 2019 are lower in six of the seven states that have such waivers in place.

The median premium decrease in those six states was 10.72%. Premiums rose by a median of 6.32% in 31 of the 44 states and the District of Columbia that did not obtain waivers.

The median premium decrease in the 13 non-waiver states in which they declined was 5.67%, much lower than the median decrease in the six waiver states whose premiums fell in 2019.

>>>The Right Way to Overhaul Our Health Care System

As of this writing, five additional states are seeking waivers for the 2020 plan year. Actuarial analyses submitted by those states forecast premium declines ranging from 5.9% to 19.8%.

Obamacare Isn’t Working

These states are pioneering the way toward making health care more affordable by chipping away at Obamacare’s rigidities.

The law’s architects adopted a Washington-knows-best approach, believing that the law’s tangle of mandates, subsidies, and penalties would result in 27 million people enrolling in exchange-based coverage.

They were wrong.

An estimated 13.7 million people have individual health insurance policies, including policies sold on and off the exchanges, roughly half as many as the Congressional Budget Office forecast. That number has been shrinking since 2016, as premiums rose beyond the reach of people who don’t qualify for government subsidies.

One reason Obamacare didn’t work as planned was that the individual mandate didn’t work as predicted. It failed to coerce people into paying an unattractive price for an unattractive product.

Government estimators were slow to recognize this failure. The Congressional Budget Office, for example, last year forecast that mandate repeal would lead to double-digit premium hikes in 2019. That, combined with looser federal regulation of short-term policies, would lead to 16% rise in premiums, according to the Congressional Budget Office.

They were wrong again. Premiums, driven by the seven states that obtained waivers, fell.

There’s little evidence that the mandate repeal or the Trump administration regulations led to an exodus of people in reasonably good health from the exchanges. Exchange enrollment held steady at 10.6 million.

Overall enrollment in the individual insurance policies fell somewhat in the first quarter of 2019, but the decline was far smaller than in 2017 and 2018 when the mandate still was in effect. Average medical claims in the individual market rose by only 5.4% in the first quarter of 2019, compared with the first quarter of 2018, among the smallest increases since Obamacare’s inception.

Had healthy people dropped out in any sizable number, average medical claims would have risen by a far larger amount.

Obamacare’s Washington-centric approach isn’t working. State innovation is working. Risk-mitigation waivers have shown that giving states authority to repurpose a portion of Obamacare funds can reduce premiums.

What Should Be Next for States?

Risk-mitigation waivers are just the beginning of what’s possible.

The Trump administration has invited states to submit bolder waiver ideas. It’s receptive to waiver applications to deliver subsidies through personal accounts and to pursue other creative ways to make health insurance more affordable.

States should take advantage of that opportunity.

What Congress Can Do

Congress should go further by converting Obamacare’s premium subsidies and Medicaid expansion entitlements into fixed grants that states could use to design and administer programs that increase health care choices and reduce costs.

States shouldn’t have to seek Washington’s permission to improve health care for their residents.

The Health Care Choices proposal, endorsed by more than 100 conservative leaders from across the country, outlines how such grants could be structured to finance the development of consumer-centered programs adapted to the circumstances of each state.

Congress should pursue that reform.

Obamacare’s centralized, inflexible structure is failing consumers. Congress should empower states to lead the way to reforms that increase health care choices and reduce costs.

This piece originally appeared in The Daily Signal