Introduction

Each year, families and individuals pay taxes to the government and receive back a wide variety of services and benefits. A fiscal deficit occurs when the benefits and services received by one household or a group of households exceed the taxes paid. When such a deficit occurs, other households must pay, through taxes, for the services and benefits of the group in deficit. Thus, government functions as a redistributive mechanism for transferring resources between groups in society.

This paper examines fiscal balance in the United States by income class. It estimates the distribution of the full array of government benefits and services including cash and near cash benefits, means-tested aid, education services, and general social services. It also estimates the distribution of all direct and indirect taxes used to finance government expenditure.

The distribution of benefits, services, and taxes is examined among conventional Census income quintiles of households for the year 2004. Of particular concern is the fiscal balance within each quintile. A quintile is in fiscal deficit if the sum of benefits and services received by households within the quintile exceeds the sum of taxes paid. A quintile is in fiscal surplus if the taxes paid exceed the cost of benefits and services received.

The analysis finds that the lowest three income quintiles are in fiscal deficit, while the two highest income quintiles are in surplus. Overall, there was a transfer of roughly $1 trillion in economic resources from the top 40 percent of households to the bottom 60 percent. This sum represents about 9.5 percent of total national income in 2004.

General Methodology and Data

The analysis presented in this paper goes beyond typical measures of income distribution by assessing the distribution of the full array of non-cash benefits and government services, not just cash benefits. The paper also analyzes the distribution of all taxes and revenue sources for federal, state, and local government.

A guiding principle in the analysis is budgetary comprehensiveness and accuracy. The estimating methods ensure that the sum of expenditures on each specific program in the analysis matches the actual expenditure total for that program according to budgetary sources. The analysis also provides budgetary comprehensiveness and accuracy with respect to revenues collected through specific taxes and revenue sources. For a given tax, the sum of taxes paid will match total collections from that tax according to budgetary sources.

Aggregate Federal, State, and Local Spending and Revenues

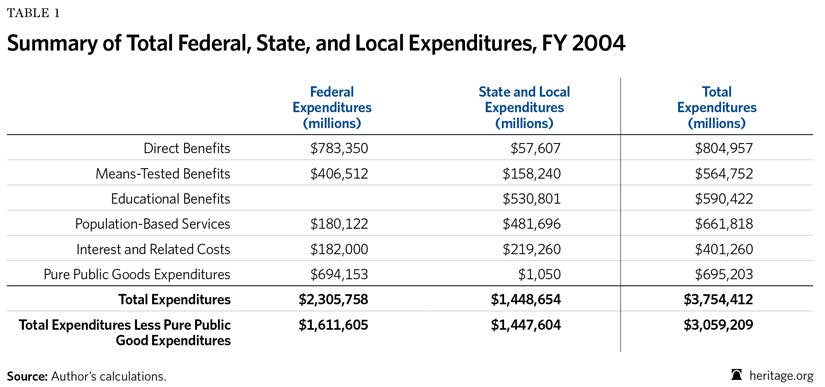

In fiscal year (FY) 2004, the expenditures of the federal government were $2.3 trillion. In the same year, expenditures of state and local governments were $1.4 trillion (after excluding federal grants and spending based on user fees). In FY 2004, the combined value of federal, state, and local expenditures was $3.75 trillion, and total taxes and revenues for federal, state, and local governments amounted to $3.43 trillion.

Types of Government Expenditures

The key to analyzing the fiscal distribution is to determine the beneficiaries of specific government programs and the fiscal cost of those benefits. Some programs, such as Social Security, neatly parcel out benefits to specific individuals. For those programs, both the beneficiaries and the cost of the benefit provided are relatively easy to determine. At the opposite extreme, other government programs (for example, medical research at the National Institutes of Health) do not neatly parcel out benefits to individuals. Determining the proper allocation of the benefits of that type of program is more difficult.

To ascertain accurately the distribution of government benefits and services, this study begins by dividing government expenditures into six categories:

- Direct benefits,

- Means-tested benefits,

- Educational services,

- Population-based services,

- Interest and other financial obligations resulting from prior government activity, and

- Pure public goods.

Direct Benefits. Direct benefit programs involve either cash transfers or the purchase of specific services for an individual. By far the largest direct benefit programs are Social Security and Medicare. Other substantial direct benefit programs are Unemployment Insurance and Workmen’s Compensation.

Direct benefit programs involve a fairly transparent transfer of economic resources. The benefits are parceled out discretely to individuals in the population; both the recipient and the cost of the benefit are relatively easy to determine. In the case of Social Security, the cost of the benefits would equal the value of the Social Security check plus the administrative costs involved in delivering the benefit.

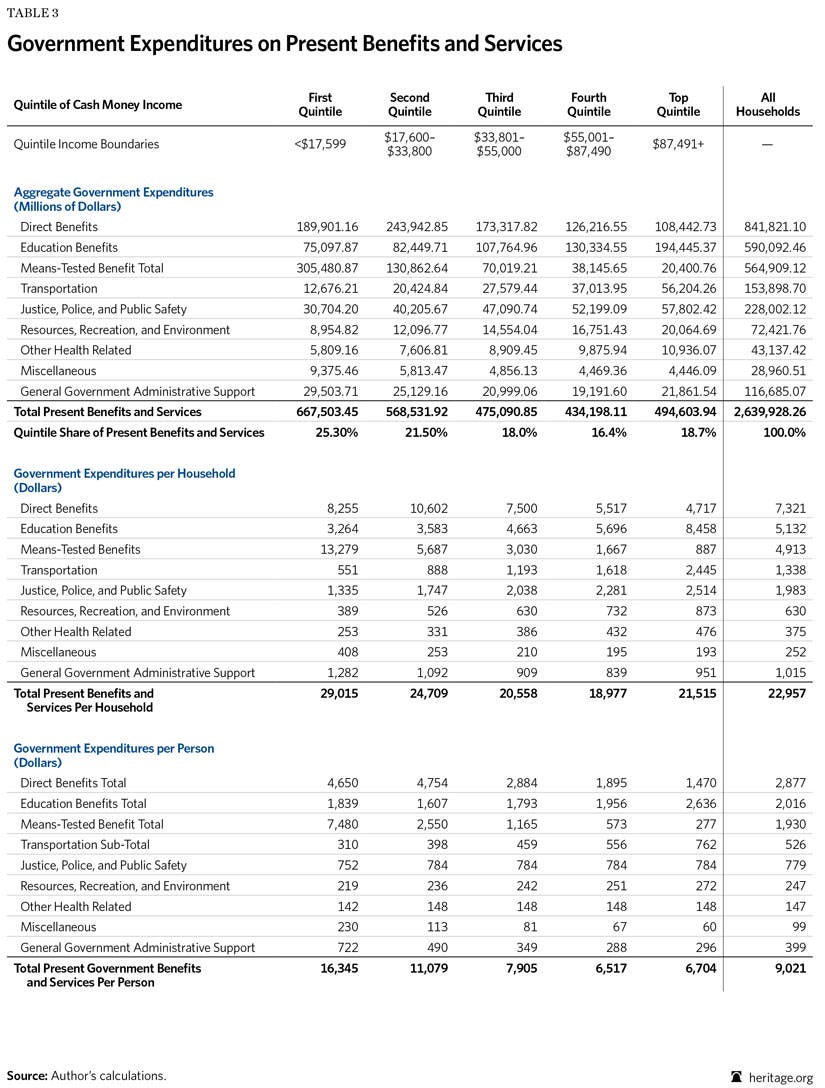

Calculating the cost of Medicare services is more complex. Ordinarily, the government does not seek to compute the particular medical services received by an individual; instead, it counts the cost of Medicare for an individual as equal to the average per capita cost of Medicare services. (The number equals the total cost of Medicare services divided by the total number of recipients.)[1] Overall, government spent $840 billion on direct benefits in FY 2004.

Means-Tested Benefits. Means-tested programs are available only to households that fall below specific income thresholds. The federal government operates over 80 means-tested programs. The largest of these are Medicaid; the Earned Income Tax Credit (EITC); food stamps; Supplemental Security Income (SSI); Section 8 housing and conventional public housing; Temporary Assistance for Needy Families (TANF); the school lunch and breakfast programs; the WIC (Women, Infant, and Children) nutrition program; and the Social Services Block Grant (SSBG). Many means-tested programs, such as SSI and the EITC, provide cash to recipients. Others, such as public housing or SSBG, pay for services that are provided to recipients.

The value of Medicaid benefits is usually counted in a manner similar to the way Medicare benefits are counted. Government does not attempt to itemize the specific medical services given to an individual; instead, it computes an average per capita cost of services to individuals in different beneficiary categories such as children, elderly persons, and disabled adults. (The average per capita cost for a particular group is determined by dividing total expenditures on the group by the total number of beneficiaries in the group.) Overall, the U.S. spent $564 billion on means-tested aid in FY 2004.[2]

Public Education. Government provides primary, secondary, post-secondary, and vocational education to individuals. In most cases, the government pays directly for the cost of educational services provided. In other cases, such as the Pell Grant program, the government in effect provides money to an eligible individual who then spends it on education.

Education is the single largest component of state and local government spending, absorbing roughly a third of all state and local expenditures. The average per pupil cost of public primary and secondary education is about $9,600 per year. Overall, federal, state, and local governments spent $590 billion on education in FY 2004.

Population-Based Services. Whereas direct benefits, means-tested benefits, and education services provide discrete benefits and services to particular individuals, population-based programs generally provide services to a whole group or community. Population-based expenditures include police and fire protection, courts, parks, sanitation, and food safety and health inspections. Another important population-based expenditure is transportation, especially roads and highways.

A key feature of population-based expenditures is that such programs generally need to expand as the population of a community expands. (This quality separates them from pure public goods, described below.) For example, as the population of a community increases, the number of police and firemen will generally need to expand proportionally.

In its study of the fiscal costs of immigration, The New Americans, the National Academy of Sciences argued that if service remains fixed while the population increases, a program will be “congested,” and the quality of service for users will deteriorate. Thus, the NAS uses the term “congestible goods” to describe population-based services.[3] Highways are an obvious example. In general, the cost of population-based services can be allocated according to an individual’s estimated utilization of the service or at a flat per capita cost across the relevant population. Government spent $662 billion on population-based services in FY 2004.

Interest and Other Financial Obligations Relating to Past Government Activities. When government revenues do not cover the full cost of government benefits and services, a portion of annual costs is passed on to be paid in future years through two mechanisms.

First, when government expenditures exceed revenues, the government runs a deficit and borrows funds. The cost of borrowing is passed to future years in the form of interest payments and repayments of principal on public debt.

Second, when a government employee provides a service to the public, part of the cost of that service is paid for immediately through the employee’s salary, but the employee may also receive government retirement benefits in the future in compensation for services provided in the present. To a considerable degree, expenditures on public-sector retirement systems are present payments in compensation for services delivered in the past.

The expenditure category “interest and other financial obligations relating to past government’s activities” thus includes interest and principal payments on government debt and outlays for government employee retirement. Total government spending on these items equaled $401 billion in FY 2004.

The allocation procedure for these costs associated with past services among the present-day population is uncertain. Consequently, such costs have been excluded from the analysis in this paper; the costs do not appear in any of the tables or figures provided.

Pure Public Goods. Economic theory distinguishes between “private consumption goods” and pure public goods. Economist Paul Samuelson is credited with first making this distinction. In his seminal 1954 paper, Samuelson defined a pure public good (or what he called a “collective consumption good”) as a good “which all enjoy in common in the sense that each individual’s consumption of such a good leads to no subtractions from any other individual’s consumption of that good.” By contrast, a “private consumption good” is a good that “can be parceled out among different individuals.”[4] Its use by one person precludes or diminishes its use by another.

A classic example of a pure public good is a lighthouse. The fact that one ship perceives the warning beacon does not diminish the usefulness of the lighthouse to other ships. Another clear example of a governmental pure public good would be a future cure for cancer produced by government-funded research. The fact that non-taxpayers would benefit from this discovery would neither diminish its benefits nor add extra costs to taxpayers. By contrast, an obvious example of a private consumption good is a hamburger: When one person eats it, it cannot be eaten by others.

Formally, all pure public goods will meet two criteria:[5]

- Non-rivalrous Consumption. Everyone in a given community can use the good; its use by one person will not diminish its utility to others.

- Zero-cost Extension to Additional Users. Once a pure public good has been produced, it requires no extra cost for additional individuals to benefit from the good. Expansion of the number of beneficiaries does not reduce its utility to any initial user and does not add new costs of production. As Economist James Buchanan explains, with a pure public good, “additional consumers may be added at zero marginal cost.”[6]

The second criterion is a direct corollary of the first. If consumption of a good is truly non-rivalrous, then adding extra new consumers will not reduce utility or add costs for the initial consumers.

Government pure public goods are rare. They include scientific research, defense, spending on veterans, international affairs, and some environmental protection activities such as the preservation of endangered species. Each of these functions generally meets the criterion that the benefits received by non-taxpayers do not result in a loss of utility for taxpayers. Government pure public good expenditures on these functions equaled $695 billion in FY 2004. Because one person’s use of these services provided with this funding does not diminish the use by others, pure public goods expenditures are not included in the analysis in this paper; no attempt is made to allocate such expenditures among households or quintiles.

For additional details, see Table 3 in the Appendix.

Taxes and Government Revenues

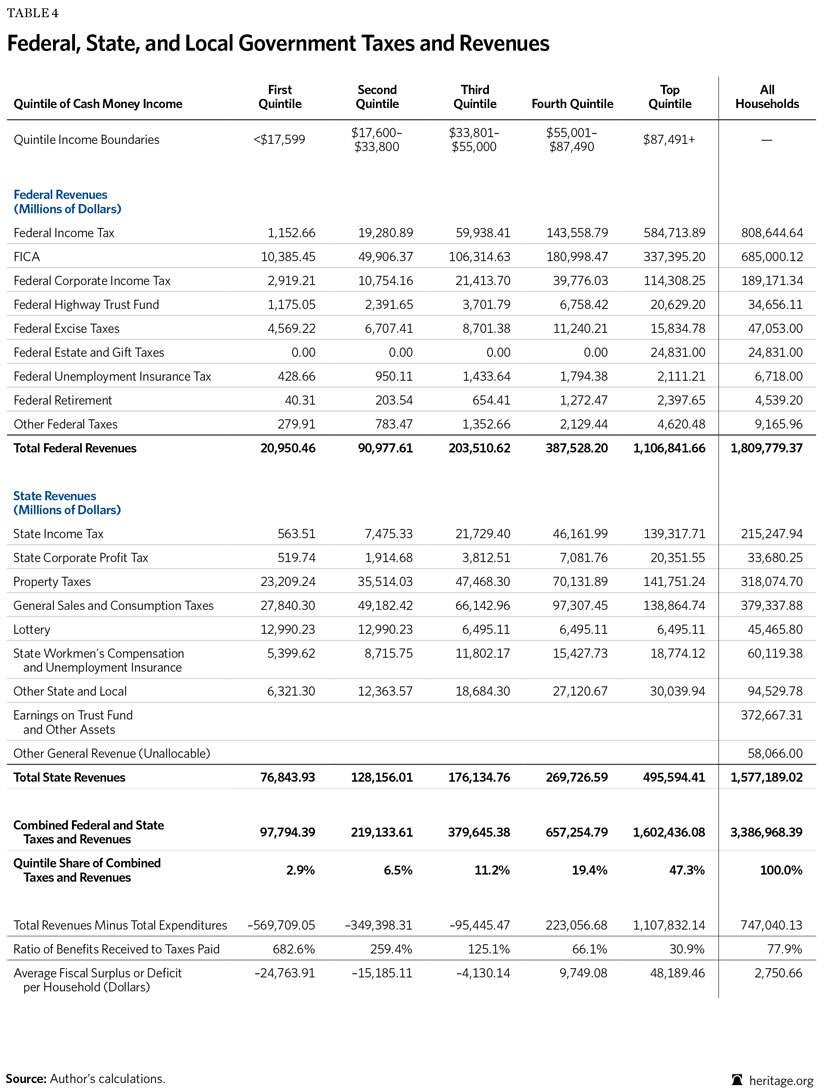

Total federal, state, and local tax revenue in 2004 came to $3.38 trillion. (See Table 4 in the Appendix.) The analysis in this paper computes 35 different taxes and revenue sources separately. The most important tax and revenue sources can be divided into the following broad categories:

- Direct Personal Taxes. These taxes include federal, state, and local personal income taxes and both the employee’s and the employer’s share of federal FICA taxes. Total tax revenue from these sources equaled $1,708 billion in 2004.

- General Sales Taxes, Consumption Taxes, and Excise Taxes. Revenues from these taxes equaled $428 billion in 2004.

- Property Taxes. State and local property taxes equaled $318 billion in 2004.

- Federal and State Corporate Income Taxes. Total revenues from these taxes in 2004 equaled $222 billion.

- Workmen’s Compensation and Other Employment Taxes. Revenue from workmen’s compensation fees paid by employers and Unemployment Insurance fees equaled $67 billion in 2004.

- State Lottery Ticket Sales. State lottery ticket sales generated net revenue of $45 billion in 2004.

- Federal Highway Taxes. Federal highway taxes equaled $35 billion in 2004.

- Federal Estate and Gift Taxes. Revenues from these taxes came to $25 billion in 2004.

Framework of Analysis: Money Income Quintiles

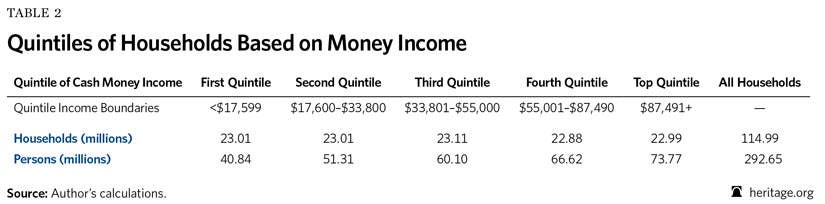

The framework of the present distribution analysis is household money income quintiles as conventionally reported in the Census Current Population Survey (CPS).[7] The Census income quintiles were used because they are the most widely used format for presenting income distribution statistics in the U.S.

Following the normal Census procedures, households in the March 2005 CPS were ranked from low income to high income according to money income and then divided into five groups or quintiles with an equal number of households in each group.

Table 2 shows the income boundaries of the adjusted quintiles and the number of households and persons in each. It is important to note that there are substantially more persons in the top income quintile than in the bottom. This has a significant impact on the measurement of the distribution of government spending, taxes, and income.

Distribution of Benefits and Taxes

The paper estimates the distribution of government benefits, services, taxes, and other revenues among the Census income quintiles. The estimation procedures for describing the taxes paid and benefits and services received are described in the Appendix.

The primary goal of the analysis is to determine the aggregate fiscal balance for each income quintile: the aggregate value of taxes and revenues paid by the quintile minus the cost of all benefits and services received. A quintile is in fiscal deficit if the cost of benefits and services received exceeds the taxes and revenues paid. Conversely, a quintile is in fiscal surplus if taxes and revenues paid exceed the cost of benefits and services received.[8]

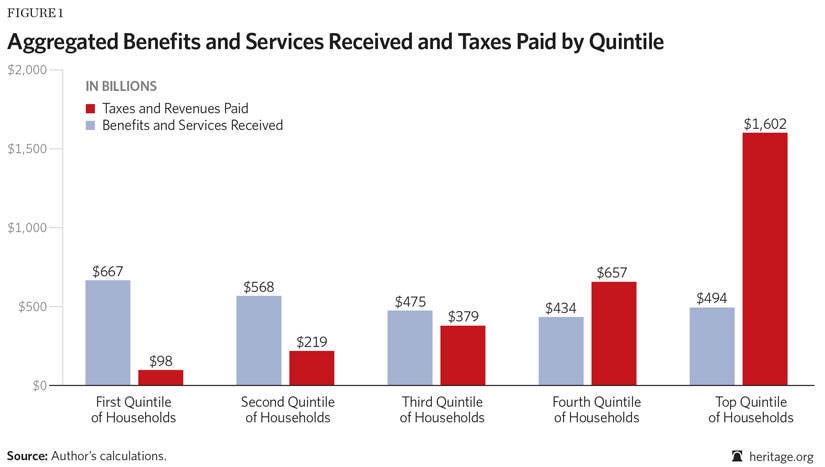

Figure 1 summarizes the allocation of government goods and services (including direct benefits, means-tested benefits, education services, and general population-based services) and allocation of government taxes and fees among the income quintiles. The distribution of government benefits and services appears on the surface to be comparatively flat. For example, in 2004, the bottom quintile received $667 billion in government benefits and surfaces, while the top quintile received only slightly less at $494 billion.

However, the apparent flatness of the distribution of government benefits and services is misleading. The bottom quintile, which has a disproportionate number of one- and two-person households, contains significantly fewer persons than the other quintiles. For example, as Table 1 shows, the bottom quintile contains 45 percent fewer persons than the top quintile. The comparatively small number of persons within the bottom quintile reduced the aggregate benefits and services received. Measured on a per capita basis, the bottom quintile actually received 2.4 times more government benefits and services than the top quintile received. (See Figure 5.)

In contrast to the distribution of benefits, the distribution of total taxes and revenues was highly unequal. As Figure 1 shows:

- Taxes and revenues paid by the bottom quintile of households were $98 billion.

- Taxes and revenues paid by the top quintile amounted to $1.6 trillion, 16 times more than the payments made by the bottom quintile.

- The $1.6 trillion in taxes and revenues paid by the top quintile represented approximately 30 percent of the pre-tax income of that group.

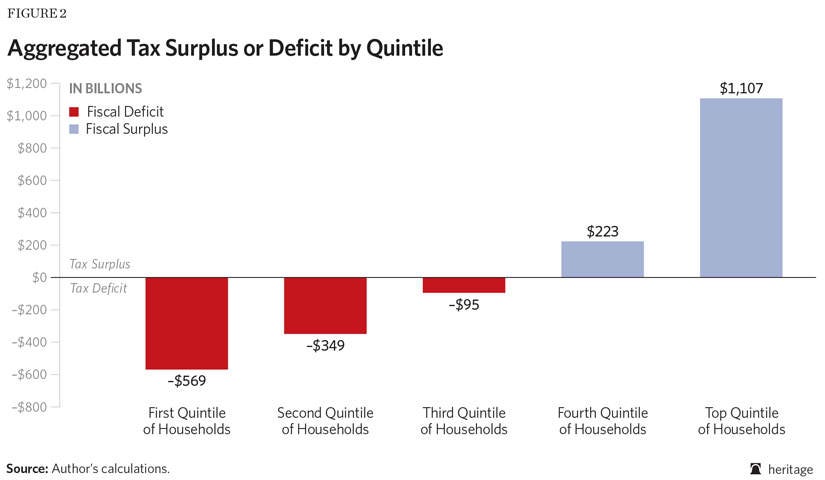

The rough equality in benefits and services received, combined with the asymmetry in taxes paid, generated a substantial redistribution of economic resources from higher-income households to lower-income households. The aggregate fiscal deficits or surpluses of each quintile are shown in Figure 2. The lowest income quintile received $569 billion more in benefits and services than it paid in taxes. By contrast, the top quintile paid $1.1 trillion more in taxes than it received in benefits and services.

Overall, as Figures 1 and 2 show, there was a transfer of roughly $1 trillion in economic resources from the top two quintiles to the bottom three. The lowest three quintiles received some $1.7 trillion in benefits and services while paying only around $700 billion in taxes. This resource gap of $1 trillion, equaling some 9.5 percent of national income, was financed by higher-income groups.

The fourth quintile and the fifth or top income quintile received some $928 billion in government benefits and services while paying $2.25 trillion in taxes, thereby generating a fiscal surplus of around $1.3 trillion. This surplus was used to fund benefits for lower-income households, to pay debt obligations, and to fund public goods expenditures.

The top quintile alone generated a net fiscal surplus of $1.1 billion that was used to finance benefits for lower-income groups, to pay interest on the government debt, and to fund public goods. This fiscal surplus equaled approximately 20 percent of the pre-tax income within the quintile.

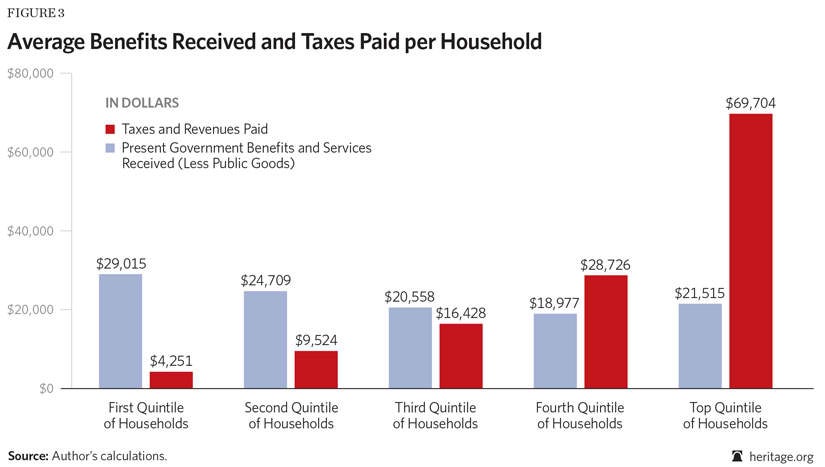

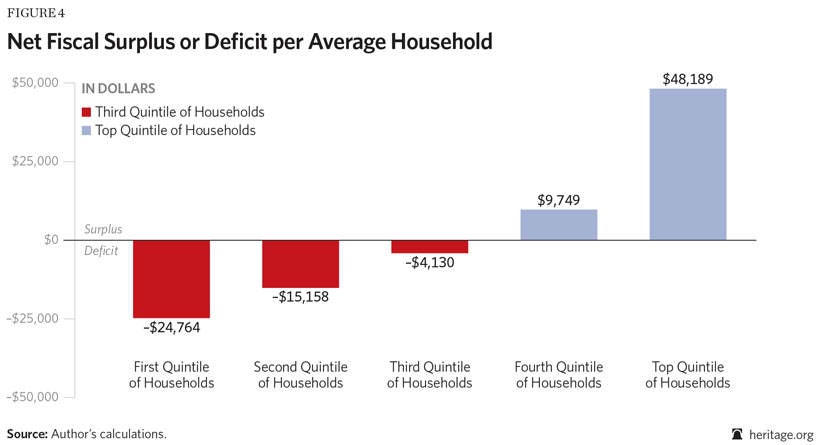

Benefits and Taxes per Household

Figures 3 and 4 repeat the analysis in Figures 1 and 2. However, Figures 3 and 4 show the benefits and services received and the taxes and revenues paid by the average household within each quintile.

- In the bottom quintile, the average household received $29,015 in benefits and paid $4,251 in taxes, generating an average fiscal deficit of $24,764 per household.

- In the middle quintile, the average household received $20,588 in benefits while paying $16,428 in taxes, generating an average deficit of $4,160.

- In the top quintile, the average household paid $69,704 in taxes and received $21,515 in benefits and services, yielding an average fiscal surplus of $48,189 per household.

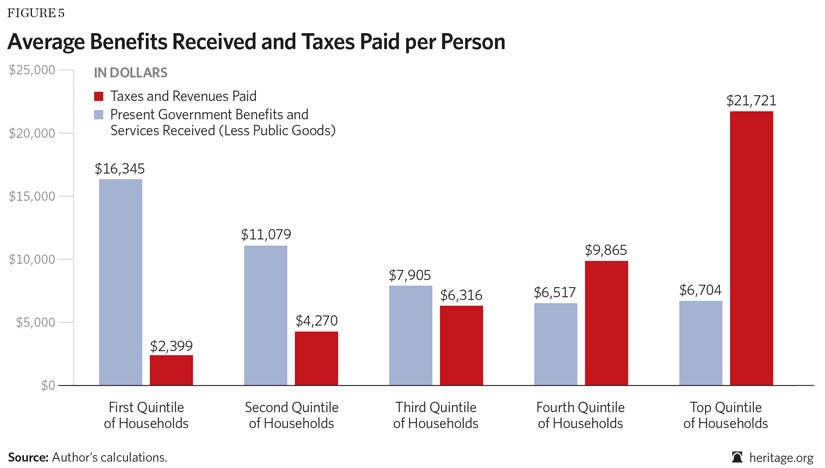

Benefits and Taxes per Person

Figure 5 repeats the analysis but now shows the average benefits and taxes per person within each quintile. Compared to the figures per household in Figure 3, the benefits per person for the first and second quintiles are far higher relative to the other quintiles. This is due to the fact, previously noted, that there are relatively few persons in the households in the bottom two quintiles.

- The average individual in the bottom quintile received government benefits and services costing $16,345 in 2004 while paying $2,345 in taxes and revenues to the government.

- The average person in the middle quintile received $7,905 in benefits and services and paid $6,316 in taxes.

- By contrast, the average individual in the top income quintile received $6,704 in government benefits and services while paying $21,721 in taxes and revenues.

Overall, the per capita benefits and services received in the bottom quintile were 2.4 times greater than those received in the top quintile.

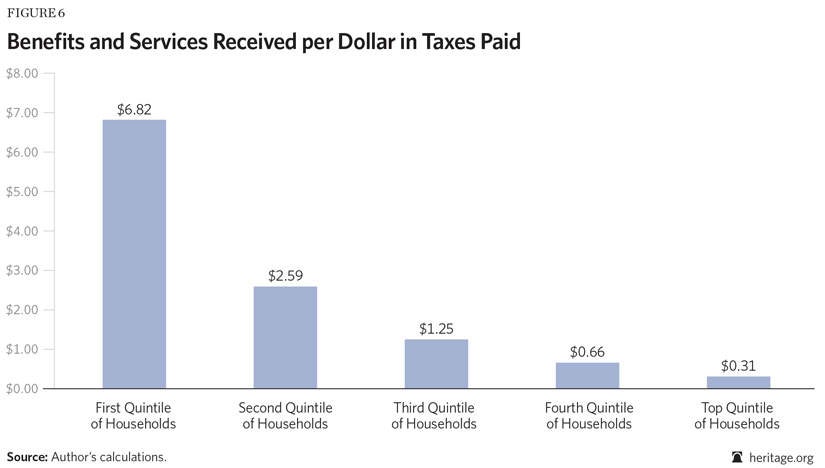

Ratio of Benefits to Taxes Within Each Quintile

Figure 6 expresses the ratio of benefits received to taxes paid within each quintile. Specifically, it shows the dollar cost of benefits and services received per $1.00 in taxes paid. This could be called the taking to giving ratio.

- The bottom quintile of households received $6.82 in benefits and services for each $1.00 in taxes paid;

- The second quintile received $2.59 in benefits and services for each $1.00 in taxes paid;

- The middle quintile received $1.25 in benefits and services for each $1.00 in taxes paid;

- The fourth quintile generated a fiscal surplus, receiving 66 cents for every dollar of taxes paid; and

- The top quintile received 31 cents in benefits and services for every $1.00 in taxes paid.

These figures summarize the overall redistributive nature of benefits and taxes. The ratio of benefits to taxes in the bottom quintile is 20.6 times higher than the ratio in the top quintile.

Discussion

The current analysis suggests certain caveats and directions for future research.

First, the ranking of households into quintiles based on Census money income is not a true pre-transfer ranking because the Census includes Social Security and some other government cash benefits in its measure of money income. An analysis that employed a true pre-transfer definition of income for the initial ranking of households would probably show a greater magnitude of redistribution from the top to the bottom.

Second, a portion of the redistribution reflected in these numbers represents transfers from working-age adults to retired adults. Redistribution between individuals over a lifetime may be less than redistribution over a single year.

Conclusion

For a century or more, the redistribution of economic resources has been a major, if implicit, function of modern government. Economic redistribution involves the transfer of economic resources from higher-income households to lower-income households. Economic redistribution occurs when a household receives a government benefit or services for which it has not paid; the cost of those benefits and services obviously must be borne by other households.

A household has a fiscal deficit if the total government benefits and services it receives exceed the total direct and indirect taxes it pays; part of the benefits and services used by such a household must be financed by other households. By contrast, a household generates a fiscal surplus if the taxes it pays exceed the benefits and services it receives. The household’s surplus will be used to finance benefits and services for other households, to pay for interest on the national debt, and to fund public goods.

The analysis presented in this paper shows that the lowest three income quintiles of households are in fiscal deficit (benefits received exceed taxes paid), while the two highest income quintiles are in fiscal surplus (taxes paid exceed benefits received).

The average household in the bottom quintile received $29,015 in benefits and paid $4,251 in taxes, generating an average fiscal deficit of $24,764 per household. In the top quintile, the average household paid $69,704 in taxes and received $21,515 in benefits and services, yielding an average fiscal surplus of $48,189 per household. The bottom quintile of households received $6.82 in benefits and services for each $1.00 in taxes paid. By contrast, the top quintile received 31 cents in benefits and services for every $1.00 in taxes paid.

The top quintile of households generated a fiscal surplus of $1.1 trillion. This sum equaled about one-fifth of total pre-tax income in that quintile. By contrast, the bottom quintile had a fiscal deficit of $569 billion. The government benefits and services received by this quintile (net of taxes paid) were roughly six times greater that the quintile’s non-government income.

Overall, there was a transfer of roughly $1 trillion in economic resources from the most affluent 40 percent of households to the lower-income 60 percent of households. This sum represented about 9.5 percent of total national income in 2004. Further, public good expenditures (such as national defense and scientific research) and interest payments on the debt are financed solely by the two highest income quintiles. Lower-income households benefit from these expenditures but do not pay sufficient taxes to support them.

—Robert Rector is a Senior Research Fellow in the Institute for Family, Community, and Opportunity at The Heritage Foundation. This paper was first presented on October 24, 2014, in Indianapolis, Indiana, at a Free Market Forum hosted by Hillsdale College titled “Markets, Government, and the Common Good.”

Appendix 1

Appendix 2: Allocation of Benefits and Taxes Among Quintiles

In the analysis presented in this paper, over 40 specific government expenditure categories and 35 tax and revenue sources are allocated among households in the five income quintiles. The details of these allocations are presented in a longer academic paper, “How the Wealth Is Spread: The Distribution of Government Benefits, Services and Taxes by Income Quintile in the United States.”[9] However, the main procedures can be summarized as follows. Direct and means-tested benefits are allocated among quintiles according to household receipt of benefits reported in the Current Population Survey of the U.S. Census Bureau. Data on child attendance in elementary and secondary schools are taken from the CPS. Each child attending a public primary or secondary school is assigned the average per pupil public education cost for the state in which the child resides. Household use of roads and highways is prorated in proportion to the household share of gasoline expenditures reported in the Consumer Expenditure Survey (CES) conducted by the U.S. Bureau of Labor Statistics (BLS). Government subsidies for public utilities and public transit are allocated in proportion to consumption data in the CES. The cost of other population-based services is allocated on a flat per capita basis.

The analysis makes the following assumptions concerning tax incidence. All personal income taxes are paid by the individual. Both the employer’s and the employee’s share of FICA tax are paid by the worker. Half of federal and state corporate income taxes are paid by business owners, and half are paid by workers. General sales taxes, consumption taxes, and excise taxes are assumed to be paid by consumers in proportion to their share of the overall expenditures of the items taxed. Property taxes on owner-occupied residential property are assumed to be paid by the owners. Renters are assumed to pay the property taxes on residential rental property. Business owners and consumers are assumed to split the costs of taxes on business property. Workmen’s compensation and other employment taxes are assumed to be borne by workers. Net revenue from state lottery ticket sales is assumed to be paid by the ticket purchasers.

Federal highway taxes paid by business vehicles are assumed to be split between business owners and consumers. Highway taxes paid by the owners of private vehicles are assumed to be paid by the vehicle owner in proportion to the share of gasoline purchased by the household.

Federal estate and gift taxes are assumed to be paid by households in the top income quintile.

Taxes and government fees are assigned to quintiles in the following manner. Direct personal taxes are assigned according to household tax data reported in the CPS. Residential property taxes for homeowners and renters are allocated according to mortgage and rental payment data in the CES; higher rent and mortgage payments are assumed to correspond to higher property values and higher taxes. General sales taxes are allocated among quintiles according to the overall distribution of consumer expenditures in the CES, excluding consumer items generally exempt from sales tax. Specific sales and excise taxes for specific consumer items are allocated according to the household expenditures on those items reported in the CES; for example, tobacco excise taxes are allocated among income quintiles in proportion to the distribution of consumer spending on tobacco reported in the CES. Corporate profit taxes, property taxes, and other taxes borne by business are prorated in proportion to property and business income reported in the CPS.