INTRODUCTION

Designed to operate as a federally run health insurance program for America's elderly, Medicare was heralded by proponents as both "historic" and "fiscally responsible."1 Now, however, Medicare is essentially bankrupt, and its ability to maintain the quality of its services is in doubt. According to the 1995 Trustees Report, if Medicare is not reformed the cash flow of the HI trust fund (Part A), which finances hospital benefits for the elderly, will go into the red in fiscal year 1997 and the fund will run out of money and become insolvent in the year 2002.2 The report provides some sobering information on how payroll taxes (which finance the HI program) would have to rise to keep the program afloat without reform. "To bring the HI program into actuarial balance even for the first 25 years,"3 a new 1.3 percent payroll tax would have to be added on top of the current 2.9 percent Medicare payroll tax. Based on the trustees' estimates for revenues under the current tax rate, this would raise payroll taxes -- and hence the cost of employing Americans -- by an estimated $263 billion over five years and $388 billion over seven years. A worker earning $45,000 would have to pay an additional payroll tax of $585 per year.

To achieve long-term actuarial balance of the HI trust fund without reforming the program -- that is, to put it on a permanently sound footing -- an immediate additional payroll tax of 3.52 percent would need to be levied on top of today's 2.9 percent rate. That would raise t axes by $711 billion over five years and $1.050 trillion over seven years. The payroll taxes of a worker earning $45,000 would increase by $1,584 per year.

And this is only to bail out the hospital program and enable those benefits to be paid. Part B also will require a rapidly increasing subsidy from general revenues to continue paying for physician services. "Growth rates have been so rapid," explain the trustees, "that outlays of the program have increased 53 percent in aggregate and 40 percent per enrollee in the last five years. For the same period, the program grew 19 percent faster than the economy despite recent efforts to control the cost of the program."4 With the trustees' "intermediate" estimates of future program growth, the annual taxpayer subsidy will grow from an estimated $38 billion in this fiscal year to an estimated $89 billion in five years and $147 billion in FY 2004.5

Trying to hold down Medicare's costs through price controls on health providers and through stringent regulations is no answer. Not only has this strategy failed to control costs, it encourages physicians and hospitals to "game" the government rather than properly serve their patients. Moreover, price controls have shifted costs to the private sector, driving up premiums for working individuals and families.

Instead of trying to tighten current controls and regulations, the proper reform is to create a very different dynamic and set of incentives to drive the Medicare program. Specifically, the bureaucratic, standardized, command-and-control structure of today's Medicare must be replaced with consumer choice among competing plans offering different benefits. This is the same dynamic that has allowed health costs to be brought under control while improving quality in the private sector -- and in the government-sponsored health plan enjoyed by Members of Congress and other federal employees.

The way to achieve the same results in Medicare is to pattern it broadly after the existing Federal Employees Health Benefits Plan (FEHBP), which covers almost nine million federal employees, families, and retirees, including present and former Members of Congress. This new program, perhaps renamed "Medi-Choice," would replace today's defined benefit program with a defined contribution program that gives America's seniors an unprecedented opportunity to choose their own health plan and range of benefits, just as retired Members of Congress and other federal retirees do. Under such a system, unlike today's Medicare program, the nation's elderly and disabled could choose sound health insurance from a variety of managed care and fee-for-service arrangements. And retirees could choose coverage for services not covered by today's standardized Medicare program -- such as a prescription drug benefit -- by accepting, say, higher copayments for other covered services. One of the great ironies of the Medicare debate is that those who oppose reform are denying the elderly the chance to receive many basic medical services already available to working Americans, and even to the indigent.

The key financial difference is that the government would make a defined financial contribution to the plan of the retiree's choice, rather than reimburse each Washington-approved service according to a fee schedule that defies comprehension and ignores market realities.6 This incentive encourages beneficiaries to pick plans with the best value for money, pocketing part of the savings from choosing more efficient coverage. It already has enabled spending in the FEHBP to increase at half the rate of Medicare, in addition to which federal workers and retirees this year were treated to premium reductions averaging 3.3 percent. Introducing the same incentive system into a reformed Medicare program would save hundreds of billions of dollars over the next decade, putting the program on a sound financial footing so that it can serve both today's elderly and the next generation of Americans.

Congress in reality has only two choices when considering the future of Medicare. One choice is to make no significant change in how Medicare is run and try to pay for future trust fund shortfalls either by raising payroll and other taxes or by diverting money from other programs. This means Medicare survives only by draining money from the rest of the budget or by raising taxes dramatically.

The second choice is to change the way Medicare is run so that benefits are delivered more efficiently, avoiding future tax increases or a diversion of money from other programs. Making the program more efficient not only will reduce the financial burden Medicare places on the next generation, but also will improve the quality of benefits and choices available to America's senior citizens.

HOW TODAY'S MEDICARE SYSTEM WORKS

Today's Medicare program pays doctors, hospitals, and other health care providers for inpatient hospital care, some inpatient care in a skilled nursing facility, home health care, hospice care, physician and supplier services, and outpatient services. In providing these services to the elderly and disabled, the program is divided into two parts. Part A finances the hospital insurance (HI) portion. Part B finances the supplemental medical insurance (SMI) portion, which covers physicians' fees.

Part A of Medicare provides premium-free coverage for part of the costs associated with certain hospital stays and limited follow-up services. Part A is financed currently through mandatory payroll taxes, which are paid into a trust fund by both employers and employees. When Medicare began in 1966, federal actuaries estimated future expenditures for Part A so that a payroll tax could be established based on potential costs. But the government's estimates fell far short of the actual costs of running this portion of the Medicare program.

The Medicare trustees recently issued a stunning report which reveals that the Part A trust fund will be insolvent by the year 2002. The reasons for this looming fiscal crisis include congressional mandates expanding covered benefits (such as adding coverage for the disabled population beginning in 1973) without providing offsetting changes in copayments or coinsurance, general medical inflation, and increased utilization by an aging population with longer life expectancies.

Part B is voluntary. All persons age 65 or over may choose to enroll in the supplemental medical insurance program by paying a monthly premium. The current contribution level ($46.10 per month as of January 1, 1995) constitutes just 29 percent of the actual cost of the Part B program. The remaining 71 percent is provided by the taxpayers. Part B covers physician services, laboratory services, outpatient hospital services, and other medical services. The program pays 80 percent of the allowed charge (after the annual $100 deductible is met); beneficiaries are responsible for the remaining 20 percent coinsurance required by law. In sharp contrast with typical plans in the private sector, as well as the FEHBP which covers retired Members of Congress and federal workers, Medicare has all of the undesirable features of a bureaucratic system.

1) Medicare relies on ineffective price controls to try to curb costs.

Medicare is a classic example of the failures of price controls to slow the growth of prices and expenditures. Not surprisingly, the program exhibits all the chronic distortions and inefficiencies that typically accompany a price control system.7 It is ironic that as countries around the world are abandoning price controls and central planning, America tries to use them to deliver health care to the elderly. It is also rather astonishing to find some lawmakers surprised at the inability of these tools to keep Medicare's expenditures under control.

Price controls in Medicare take such forms as the diagnostic related group (DRG) system for hospital payments and the resource-based relative value scale (RBRVS) system for physician services -- the latter remarkably similar to the obsolete labor theory of value, which is the basis of socialist economics.8 Under the DRG system, hospitals are reimbursed according to a complex system of fees based on the illness being treated, while physicians are subject to a fee schedule according to the procedure being used. The "value" of a doctor's labor, along with the "value" of other statistically weighted "resource inputs" into the provision of a medical service, is calculated according to the statistical methods of social sciences. Fees are set on the basis of this statistical calculation, as applied to each of approximately 7,000 medical procedures, as measured and weighed by experts at HCFA.9 Needless to say, the consequences, such as cost shifting and similar distortions, have not proven any different from those resulting from the imposition of price controls in any other sector of the economy.10 Controls have not worked, and the SMI program is growing at an unsustainable rate under current legislation and rules.

This elaborate system of controls has failed to hold the rate of growth in Medicare expenditures to a degree comparable to the private sector. For example, Medicare has experienced 10 percent overall growth and is projected to grow at approximately the same rate over the next five years. Contrast this with the private sector, where employer health premiums in 1995 dropped by 1.1 percent while medical inflation increased by only 4.7 percent. Price controls also have led to distortions and inefficiencies familiar to any student of such controls. For example:

- Government action to squeeze payments to Medicare hospitals and physicians has led to significant cost shifting (or, more accurately, "price shifting") to non-Medicare services.

- Price controls have encouraged providers to try to make up for low fees by increasing the volume of services (such as calling patients in for additional office visits or conducting tests of marginal value) or by such actions as reducing the average duration of office visits. The government's response -- typical of responses to this form of price control evasion -- has been to introduce elaborate "expenditure controls," with the result that honest physicians are penalized for hard work and attention to their patients.

- Diagnosis codes are modified subtly by physicians and hospitals to qualify for better payments. Indeed, software packages are marketed routinely to hospitals and doctors to show them how to maximize reimbursements from Medicare by choosing one diagnosis code rather than another for the same medical problem.

The experience of price controls in Medicare is the experience of price controls throughout history. Providers, and sometimes patients, react to each control by seeking ways to evade it, with a general loss of efficiency; then government introduces a new, more elaborate control in an attempt to address the deficiencies of the first. The cycle continues as the providers find a way around that control. Meanwhile, efficiency suffers and expenditure targets are exceeded.

2) Government limits the benefits available to the elderly.

Unlike congressional and federal retirees, who are covered under a variety of plans in the FEHBP, most other senior citizens are locked into the "one-size-fits-all" Medicare program. There is no freedom to choose levels of benefits, or to choose alternative benefits, within today's Medicare. Beyond electing to participate in the voluntary supplemental insurance program (SMI, or Part B) with its standardized benefits, the only choice most elderly Americans make in health insurance is whether they will purchase a "Medi-gap" policy for services and benefits not covered in the Part B program. But retired Members of Congress and federal workers, just like active members of the federal workforce, can choose from health insurance plans ranging from fee-for-service coverage, to union-sponsored plans, to various forms of managed care. Moreover, they can choose plans with different covered services, such as dental benefits and drug coverage, that generally are not available under Medicare.

Another important benefit found routinely in private plans but not in Medicare is catastrophic coverage. This crucial benefit protects individuals against high costs associated with catastrophic illness or accidents. Among the other benefits not covered by Medicare but covered by the FEHBP's popular Blue Cross Blue Shield Standard Plan are (to take one example):

- Preventive screening, stool tests for blood, prostate specific antigen tests, and related office visit charges.

- Routine physical exam, including a history and risk assessment, and a serum cholesterol test, once every year.

- Home nursing care.

- Smoking cessation.

- Home physician visits.

3) Medicare resists innovation in the delivery of care.

In addition to its implicit distortions and evasions, a price control system fails to control costs because its bureaucratic nature reduces the pace at which efficiency-improving innovations are introduced. In a competitive market-based system, choice and competition lead to a decentralized, continuous, and rapid introduction of ideas to improve the ratio of quality to price. These are accepted or rejected to the degree that buyers and sellers agree they are an improvement.

In a centrally planned system like Medicare, the process is entirely different. Proposed changes must "trickle up" to senior officials responsible for the program, after which they typically must be evaluated by bureaucrats and boards, proposed to politicians, and subjected to the pressures of competing interests before they take effect. The result is slow and encourages politically influenced decisions. Moreover, private sector managers are motivated by competition to find the best way to satisfy the patient at the lowest cost. Bureaucrats are motivated by the incentive to avoid risk and controversy, which results in the denial of many new services and procedures to Medicare patients.

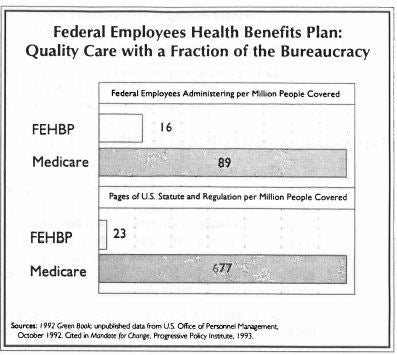

Medicare is run by the Health Care Financing Administration (HCFA), an agency of the U.S. Department of Health and Human Services. HCFA's more than 4,000 employees issue and enforce hundreds of pages of regulations and thousands of pages of guidelines, managing virtually every aspect of the delivery and financing of the health care to the elderly.11 While Medicare claims an overhead cost of just three percent, the rules and regulations emanating from HCFA merely shift large administrative costs to hospitals and physicians. Moreover, Medicare requires far more federal administrators and rules for its operation than does the FEHBP, which also is run by the government -- but on very different principles.

In keeping with Medicare's central planning/price control design, Congress and HCFA systematically fail to introduce service delivery innovations while depriving seniors of state-of-the-art medical technology. For example:

Medicare will refuse all reimbursements to hospitals conducting clinical studies on Medicare patients, so seniors are denied access to medical innovations developed in the United States. As highlighted in USA Today, "Faced with possible federal charges and potentially millions of dollars in fines, hospitals slammed on the brakes... shutting down all device studies or excluding Medicare patients from them. Doctors were no longer able to provide what they considered the latest treatments to many older patients."12

This happens not only because HCFA must formulate guidelines for every category of medical equipment, but also because it must decide whether each new medical device or treatment meets the criteria for coverage under Medicare Part B. This highly regulatory process has proven extremely expensive for taxpayers and dangerous for patients.

Dr. John Rowe, President of New York's Mt. Sinai Medical Center, recently gave the Senate Finance Committee a graphic example of what this means in practice. He asked the committee to consider a hospital performing major heart surgery under Medicare and a patient who needed a pacemaker inserted on his twentieth day in the hospital. If a clinical test happened to be underway on pacemakers to test the effectiveness of alternative electrical leads, HCFA might well rule this treatment experimental and deny reimbursement for the patient's stay in the hospital.13

- Medicare is essentially a "fee-for-service" program. It has made little progress in allowing, as an option to the elderly, managed care plans such as health maintenance organizations (HMOs) or competitive medical plans (CMSs). Moreover, with the rigid guidelines established by the HCFA, Medicare's payment scheme to HMOs is crude.14 As a result, former HCFA Administrator Gail Wilensky has testified before the House Ways and Means Committee that inadequate adjustments appear to have produced large overpayments to many HMOs and underpayments to others.15

- Non-HMO managed care options are very limited. For example, risk-based "carve-outs" like the package-priced heart bypass operation are not allowed except on a demonstration basis.

Slow service design innovation is endemic to Medicare's price control/central planning system. While the process conceivably could be accelerated, it cannot even theoretically match the pace of innovation in a competitive marketplace.

THE SCOPE OF MEDICARE'S FINANCIAL CRISIS

According to the Medicare Trustees, the financial soundness of the HI and SMI trust funds is of great concern due to their past and projected rapid rates of growth. This concern is heightened by the major demographic shifts in the workforce which supports the Medicare population. Currently, 4.7 workers support each beneficiary, but this ratio is expected to decrease significantly: by the year 2030, only two workers will be supporting each beneficiary. Given the trust funds' inadequate level of reserves and weak financing structure, however, the HI trust fund is projected to reach insolvency long before this demographic change takes place.

Medicare has become the second largest entitlement program, after Social Security, in the federal budget. It is in long-term financial crisis because payroll taxes and other revenues do not cover costs, so net outlays must be covered by new taxes or by diverting money from other programs in the budget. Such net outlays totaled $144.7 billion in 1994. Government actuaries project that under current law Medicare will cost taxpayers $198.7 billion by 1997 and $263.6 billion by 2000. It is little wonder that the trustees, who include three Clinton Administration Cabinet secretaries and two other senior Administration officials, called on Congress to take "prompt, effective and decisive action" to curb the program's escalating costs.16

These general problems appear in both parts of the Medicare program.

The Mess in Medicare Part A (HI)

Medicare Part A (HI) is financed through payroll taxes on current employees, their employers, and the self-employed. Before January 1, 1994, HI tax rates of 1.45 percent on employees, 1.45 percent on employers, and 2.9 percent on the self-employed were applied on earnings up to $135,000.17 As part of his Administration's effort to reduce the deficit, President Clinton proposed that all earnings be subject to the HI tax, beginning in 1994. But despite lifting the limit on earnings subject to the HI tax to yield additional revenues, the Administration targeted the additional tax toward deficit reduction, not the HI trust fund. Since the HI tax took effect in 1966, the maximum taxable income level has been increased 23 separate times.18

Contrary to widespread belief, HI revenues and expenditures do not go through a real trust fund. As a matter of fact, no trust fund with money in it actually exists.19 The "fund" is merely an obligation on the government to find the money, through taxes, to pay for future benefits. As the Annual Report by the Board of Trustees of the Federal Hospital Insurance Program explains, the government has never saved the necessary tax revenues to cover the future health care needs of private sector employees. The reason: Medicare began paying out HI benefits at the same time it began collecting taxes.20 Younger workers on average contribute more to the Social Security and HI fund each year as their earnings increase. These contributions, however, are not saved. Instead, they are transferred and spent almost immediately on the current Medicare population.21 Moreover, the elderly typically receive far more in benefits than they have paid in payroll taxes.

Long-range HI projections show that Medicare hospital costs will rise much more quickly than inflation. The most recent projections by the Board of Trustees of the HI trust fund use three alternative sets of assumptions: low cost, intermediate, and high cost. The intermediate set of assumptions is said to represent the trustees' best estimate of the future economic and demographic trends that will affect the program's financial status. Under this option, the present financing structure is sufficient to ensure the payment of HI benefits only over the next seven years: "As a result, the HI trust fund does not meet the trustees' short-range test of financial adequacy."22 Under the high cost (pessimistic) option, the fund will be exhausted in 2001. Under the low cost (optimistic) option, the fund will be exhausted in 2006. When the trust fund is fully depleted, Medicare is legally obliged to stop reimbursing providers.

Medicare Part B's Exploding Costs

Congress established the Medicare Part B (or SMI) program in 1966 to create a taxpayer subsidy for the premiums paid by the nation's elderly, setting it at 50 percent of premium cost. Until 1973, SMI premiums continued to finance 50 percent of the benefit and administrative costs of the program, plus a small contingency amount in a separate trust fund.

When Part B costs began to increase faster than inflation, Congress decided to limit increases in the premium to the same percentage as Social Security cost of living adjustments. Under this new formula, revenues from Part B premiums for beneficiaries decreased from 50 percent to 25 percent of the expenditures because costs increased at a faster rate than inflation as measured by the Consumer Price Index (CPI), used to calculate Social Security adjustments. Beginning in the early 1980s, Congress has voted consistently to set Part B premiums at a level which would cover only 25 percent of costs. As a result, Medicare enrollees in 1995 pay only $46.10 per month for generous insurance that covers 80 percent of allowable charges with a deductible of only $100. The illusion that comprehensive health insurance is inexpensive means that Americans aged 65 or over have no incentive to control costs.

In their report to Congress, the trustees "[n]ote with great concern the past and projected rapid growth in the cost of the program. Growth rates have been so rapid that outlays of the program have increased 53 percent in aggregate and 40 percent per enrollee in the last five years. For the same time period, the program grew 19 percent faster than the economy despite recent efforts to control the cost of the program."23 As a result of the escalating cost of this portion of Medicare, expenditures are projected to increase from 0.93 percent of the Gross Domestic Product (GDP) in 1994 to 4.29 percent of GDP in 2069. With the trustees' "intermediate" estimates of future program growth, the annual taxpayer subsidy will rise from an estimated $38 billion in this fiscal year to an estimated $89 billion in five years and $147 billion in FY 2004.24

HOW TO REFORM MEDICARE

In grappling with Medicare's emerging fiscal crisis, Congress needs to pursue both short-term budgetary measures and a long-term strategy of structural change. Short-term measures are needed to deal with the program's injustices and glaring shortcomings. Long-term reform is needed to deal with structural financial problems and to improve the quality of care for America's seniors. Moreover, to deal with public confusion about the status of the Medicare system and the purpose of reform, Congress must educate the American people about the true dimensions of the problem, including the potential tax burden facing working Americans if action is not taken. This can be accomplished in two ways:

First, Congress should order the Health Care Financing Administration (HCFA) to notify America's senior and disabled citizens that their Medicare hospitalization program faces bankruptcy as early as 2002, according to the Medicare Trustees Report. HCFA should explain that to keep the program going without reforms will mean billions of additional tax dollars taken from the paychecks of working Americans or diverted from other programs.

Second, Congress should order HCFA to inform the elderly that the premiums they pay for their Medicare supplementary insurance Part B represents only 25 percent of the premium income for those services and that their children and grandchildren, young working families, are paying for the bulk of these Medicare benefits out of general tax revenues. Most elderly believe that they are paying the full cost of their Medicare benefits; the truth about Medicare's financial condition and circumstances can only improve the quality of the necessary public debate.

Short-Term Reform of Part

Congress should act immediately to reduce the heavy taxpayer subsidy of Medicare's Part B premiums.

OPTION #1: The simplest, though not necessarily the best, option would be to restore the premium to the original 50 percent level. This could be done by gradually phasing down the current level of taxpayer subsidies by five percent per year over a five-year period, which would save taxpayers approximately $37.27 billion over the next five years.25 By financing one-half of Part B program costs, Congress would return to the spirit of the original 1965 "contract" with America's taxpayers.

Reducing the taxpayer subsidy would encourage many enrollees to compare the costs and benefits of more efficient private alternatives with the costs and benefits of the Part B program. The more the subsidy is reduced, the more level the playing field between the private sector and government. The elderly would have incentives to choose more efficient plans in the private sector. The likely result: not just a reduction in the subsidy, but also a significant reduction in gross budget outlays for Medicare Part B.

One problem with simply reducing the subsidy across the board is that it would impose some hardship on many lower-income Americans while continuing taxpayer support (albeit reduced) for the more affluent. It also would raise the cost to states of enrolling in Medicare some individuals already on Medicaid.

OPTION #2: An alternative would be to reduce the current subsidy as income rises and perhaps raise the level of subsidy for the elderly with very low incomes. The savings from such a change would vary widely, depending on what method of means-testing was introduced. At, say, $65,000 adjusted gross income for individuals and $85,000 for couples, the subsidy might be phased out in increments of three percentage points per $1,000 of income above the threshold. The full premium would be paid by individuals above $98,000 in AGI and couples above $118,000 in AGI.

Not a Tax. Contrary to what liberals in Congress may say, a higher Part B premium represents not an increase in taxes, but a reduction in a large direct subsidy. It is not a tax increase because Medicare Part B is a voluntarily chosen service that can be provided just as easily by the private sector. Part B is a subsidized commercial service provided by the federal government in competition with the private sector. If Members of Congress believe it necessary to give high levels of subsidies to enrollees, those subsidies should be targeted not to everyone over 65, but to elderly citizens who cannot afford an acceptable level of physician services and other services now available under Part B.

A POSSIBLE MODEL FOR LONG-TERM REFORM -- THE FEHBP

Members of Congress searching for an alternative model for Medicare reform do not have to look far. For well over three decades, Members of Congress and federal employees -- and federal retirees -- have been enrolled in a unique consumer-driven health care system called the Federal Employees Health Benefits Program (FEHBP). Unlike Medicare, it is not run on the principles of central planning and price controls. Instead, it is based on the market principles of consumer choice and competition.26 Beginning in 1960 with 51 plans for the federal workforce, the FEHBP now encompasses over 400 private health insurance plans nationwide, ranging from traditional indemnity insurance and fee-for-service to plans sponsored by federal unions and employee organizations to different forms of managed care, including health maintenance organizations (HMOs) and preferred provider organizations (PPOs). In the Washington, D.C., metropolitan area, half of all persons with health insurance are covered by one of the 35 plans competing in the FEHBP.

The FEHBP is entirely different from Medicare. For one thing, Medicare is a defined benefit program, meaning each enrollee has access to a specific set of health services which are paid for, in total or in part, by the federal government. The FEHBP, on the other hand, is a defined contribution program in which the government agrees to provide federal workers or retirees with a financial contribution they can use to purchase the health coverage of their choice.

Even more important, and unlike Medicare, the FEHBP does not attempt to constrain costs by controlling prices and specifying a comprehensive set of services. It sets only minimal guidelines over how plans must be structured and marketed. The law specifies only a brief category of core benefits, permitting federal workers and retirees to choose the plans and benefits that are right for them. Cost restraint is achieved not with an army of Medicare-style price controllers, but through the operation of consumer choice in a market of competing plans. That is why FEHBP spending is projected to increase at about 6 percent per year while spending for Medicare is expected to grow at 10 percent per year.

Choices for Federal Retirees. The FEHBP is open to all congressional and federal retirees who retired after July 1, 1960. Under current rules, congressional or federal retirees are eligible to enroll in an FEHBP plan if they retired on an annuity with at least five years of continuous service at the time of retirement, or if they retired on a Civil Service disability. They also can assure coverage for spouses by electing survivor benefits, and any survivor annuitant can request coverage for grandchildren, under certain conditions, on or after August 11, 1994.27

Significantly, while private sector firms have been cutting back, or even eliminating private health insurance for retirees altogether, the FEHBP has improved its coverage. Moreover, while the number of active employees has remained fairly constant over the past ten years, the number of retirees has grown from 1.3 million to 1.6 million.28 Congressional and federal retirees and their dependents now make up 40 percent of total enrollment,29 enjoying access to choices and services denied to Americans enrolled in Medicare. Among the features of the FEHBP:

- Wide Choice of Health Plans. No other group of Americans enjoys the range of personal choice over health plans available to active and retired congressional and federal employees. Their private plans range from fee-for-service to managed care. They can obtain plans through organizations they trust. Plans sponsored by federal unions and employee organizations are particularly popular among federal workers and retirees -- almost one-third are enrolled in such plans. Among the managed care plans, which have become quite popular in recent years, there are many different options, including "point of service" plans in which retired federal and congressional workers can choose to use a personal physician outside the HMO network for a higher copayment.

The FEHBP is very popular among federal retirees -- so popular that a significant number of federal retirees who enroll in Medicare keep their existing federal coverage as a "wraparound" plan. While Medicare is their primary source of insurance, the additional benefits included in the FEHBP (such as prescription drugs, catastrophic coverage, and preventive care) serve as more than adequate protection. As the National Association of Retired Federal Employees states in its 1995 guide to federal health plans for retirees, "All FEHB plans are good.... You can't make a serious mistake in choosing a FEHB plan unless you choose a high cost plan or option when you don't need one."30

Choice of Health Benefits. Federal retirees do not have merely a choice of plan. Unlike virtually all other Americans, active or retired, congressional and federal retirees also have the freedom to choose the services they want. Unlike Americans enrolled in Medicare, they are not locked into a single, government-standardized benefits package. Beyond the normal range of typical hospitalization and physician services, they can pick from a variety of plans that cover such items as skilled nursing care and home health care by a nurse, dental care, outpatient mental benefits, routine physical examinations, durable medical equipment and prostheses, hospice care, chemotherapy, radiation, physical and rehabilitative therapy, prescription drugs, mail order drugs, diabetic supplies, treatments for alcoholism or drug abuse, acupuncture, and chiropractic services. And FEHBP plans include catastrophic coverage -- in sharp contrast to Medicare.

Advice and Consumer Information. Congressional and federal retirees are not on their own in making a choosing a plan. They receive advice from private federal employee and retiree organizations on the best plans and best benefit options.

In particular, retirees and workers are advised by consumer organizations such as the National Association of Retired Federal Employees (NARFE). Washington's Consumer Checkbook, a consumer organization, advises retirees on the best options, such as enrolling in plans that coordinate with Medicare. Various other groups rate plans and provide information on services, quality, and levels of benefits.

For example, NARFE advises federal retirees on the range of catastrophic coverage options available to them. Among other tips, it points out to retirees that the High Option Blue Cross Blue Shield plan, while expensive, has "home health care benefits that the Standard Blues plan doesn't have"; that the Alliance Plan covers up to 90 Cardiac Rehabilitation visits for angina pectoris, myocardial infarction, and coronary surgery; that the most comprehensive dental coverage is available from the Mail Handlers high option plan, as well as the Postmasters and National Association of Letter Carriers high option plans; that the Government Employees Health Association offers the best value in home health care services; that the Blues offer the best hospice care; and that the best skilled nursing benefits are offered by the Postmasters.31

Choice of Price. Unlike the limited or non-existent choices available to private sector workers and retirees, and unlike the rigidly controlled pricing under Medicare, FEHBP premiums, coinsurance, or copayments represent a wide range of options. Under the FEHBP's financing formula, the federal government will contribute up to 75 percent of the cost of a plan, up to a maximum of $1,600 for individuals and $3,490 for families.

If congressional and federal retirees wish to choose a very expensive "Cadillac" plan with a rich set of benefits, they may do so, but they make the decision to pay extra. If, on the other hand, they pick a less expensive plan, they save money on their portion of the premium. Private health plans compete directly for these consumers' dollars.

Needless to say, the dynamics of a competitive market in the FEHBP have had a positive impact on premium prices for federal employees and retirees. According to the Congressional Budget Office:

Over the past five years, FEHB plan premiums have increased an average of 6.8 percent a year, whereas the premiums paid by medium and large firms surveyed by Hay/Huggins Company, a benefits consulting firm, increased by 10.8 percent a year. Furthermore, FEHB premiums are expected to decline by 3.3 percent in 1995; the Congressional Budget Office projects, however, that aggregate private health premiums are likely to rise by about 5 percent.32

According to the CBO, Medicare hospitalization (HI) costs will rise 8.4 percent per annum between 1995 and 2000, and Medicare supplemental medical insurance (SMI) costs will rise at 12.9 percent per year.33

Deficiencies of the FEHBP. The FEHBP is not without deficiencies.34 The most significant is that plans must offer a form of community-rated premiums, meaning they must offer a plan to a healthy 19-year-old at exactly the same premium as a very sick 89-year-old. This inevitably leads to adverse selection. Still, the FEHBP functions so well that even this problem does not undermine the program, although it does introduce distortions and perverse incentives that prevent it from functioning as effectively as it should. A wise reform would be to vary the degree of assistance to FEHBP enrollees at least according to their age and to permit plans to vary premiums, also by age. That would allow plans to compete more effectively and to offer services with less vulnerability to adverse selection.

A REFORM AGENDA FOR MEDICARE

Congress has committed itself to curbing the growth of Medicare spending in order to restore financial stability and prevent out-of-control spending from draining money from other programs or forcing huge increases in taxes. To carry out this wise commitment, Congress can proceed in two ways. It can impose tighter regulation and stricter price controls while cutting medical services for the elderly, as it has in the past. But experience shows that this strategy yields only short-term spending reductions at best. In the long run, it does nothing to curb runaway spending and undermines the quality of care for the elderly.

The other option for Congress is to achieve spending restraint by giving the elderly greater control over their Medicare dollars and greater opportunity to use their dollars to select the health care plans and services that are right for them. Such a reform, modeled after the system serving federal retirees, would use consumer choice and competition to curb waste and improve care.

Such a reform would include three principles:

- PRINCIPLE #1: Medicare should be changed from a defined benefit program to a defined contribution program.

- PRINCIPLE #2: The elderly should be allowed to use their Medicare dollars to enroll in a plan with health services that they choose, not services that bureaucrats or politicians have chosen for them.

- PRINCIPLE #3: Cost control should be achieved through consumer choice and competition, not central planning and price controls. HCFA's complex system of price controls and other restrictions should be phased out.

One reform incorporating these principles would be to provide Americans eligible for Medicare with a voucher to purchase the Medicare plan of their choice. The sum provided would be the combination of two amounts, reflecting the financing of today's Part A and a reformed Part B. The two elements of the voucher would be:

Portion (A) Part of the voucher would be an amount -- adjusted by age, sex, reason for entitlement (age or disability), institutional status, ESRD (end-stage renal dialysis) status, and geography -- intended to cover the actuarial equivalent of the hospital and other services in today's Part A of Medicare. This portion would not be means-tested.

Portion (B) The other part of the voucher would be based on an amount -- adjusted by age, sex, and geography -- intended to cover the actuarial equivalent of the services currently in Part B. This base would be means-tested to determine the dollar amount of this element. Since today's Part B is voluntary, the elderly should be allowed to decline this portion of the voucher if they so choose.

An alternative form of defined contribution would be for Medicare to cover a certain percentage of the premium for the plan of the elderly's choice, up to a maximum dollar amount. This would be more like the FEHBP but would mean somewhat less financial assistance for the lower-income elderly.

The elderly could use the voucher (or percentage contribution) to purchase a Medicare-approved health plan of their choice. Medicare would distribute information on the plans to the elderly, as well as a checklist from which they could pick the desired plan. Medicare would then inform the appropriate plan of the retiree's choice.

These plans, somewhat like those offered through the FEHBP to retired federal workers, would have to meet certain requirements to be marketed as Medicare-approved:

Plan Requirement #1. A plan would have to meet certain financial requirements to assure solvency. It would also have to be licensed in the state in which it provided coverage to Medicare enrollees.

Plan Requirement #2. The plan would have to specify its services and costs in a standardized manner to enable the elderly to choose without confusion. It would also have to make this information available to the government for distribution to Medicare beneficiaries.

Plan Requirement #3. Each plan would have to contain a core set of benefits, including basic hospital and physician services with catastrophic coverage. This core would be leaner than today's Medicare, thereby permitting the elderly to purchase a less expensive basic plan and supplement it with optional services or -- with the help of the voucher -- to buy those services directly from providers. As an option, plans could include a Medical Savings Account from which the enrollee could pay directly for services with insurance only for catastrophic expenditures. Funds in a Medical Savings Account could be used only for health care services.

The core benefits for those declining the Part B portion of the voucher would be less extensive and focused on hospital services. Seniors who declined the Part B portion could buy additional insurance or pay for benefits without any requirement that these additional services comply with federal guidelines. Thus, the equivalent of Part B coverage would continue to be non-compulsory.

An alternative would be for Congress to require that, at a minimum, each plan contain the specific services available today under Medicare, yet allow plans to offer additional services -- with perhaps higher copayments for services currently in the Medicare package.

States would be precluded from mandating any benefits or premium structures for plans serving the Medicare population.

Plan Requirement #4. Each plan would have to set premiums according to limited underwriting principles: age, sex, reason for entitlement (age or disability), institutional status, ESRD status, and geography, but not health status.35 One possible exception might be to permit "lifestyle" premium discounts for seniors willing to enroll in sickness prevention and health promotion programs.

Plan Requirement #5. Each plan would have to accept any Medicare-eligible applicant for coverage at its published terms during an annual "open season" enrollment period.

Government's Role

The government's role -- particularly HCFA's -- would be limited but important. HCFA would be precluded by law from regulating either the prices of medical services to the elderly or the premiums for plans. It would have three very important functions:

a) The government would create a federally sponsored corporation to offer a "Medicare Standard Plan" which would offer the standard Part A and Part B benefits available today. The Medicare Standard Plan would be assigned a premium, and any Medicare enrollee would be able to choose it in preference to any of the private plans. Enrollees would have to apply their vouchers toward the plan premium. The standard plan would have to comply with exactly the same disclosure and other requirements as any private plan.

b) Each year HCFA would be responsible for running the "open season," the period in which the elderly and disabled in Medicare chose the health plan they wanted for the following year. Just before the open period, HCFA would send all enrollees information on which to base their choice: the value of their voucher, a list of Medicare-approved plans in their area with a standardized listing of benefits and premiums, and a form for indicating their choice. This is virtually identical to the role played by the Office of Personnel Management in the FEHBP.

c) Once a Medicare retiree had made a choice and returned the form, HCFA would send the voucher to the chosen plan if the premium exceeded the value of the voucher. The enrollee would be responsible for the difference but could choose to have HCFA send the entire premium, paying for the difference by reducing the amount of his Social Security check (this is how most of the elderly now pay their Part B premium). If an individual chose a low-cost plan which cost less than the voucher, HCFA would deposit the difference in a Medical Savings Account of the enrollee's choice. This money could be used only for health care payments.

ADVANTAGES OF THE REFORM

A reform based on this consumer-choice approach would have numerous advantages for the elderly and the taxpayer.

- Freedom to Choose Plans and Benefits. Under a consumer choice Medicare system, elderly Americans could choose the private health insurance that best meets their individual needs. With the advice and counsel of their doctors, they could pick not only the level of benefits above a basic set of hospital and physicians services, but also a broad range of medical services and treatments available on the free market -- for instance, a plan with drug coverage or dental care -- which they do not get under Medicare. Consulting with their doctors, rather than waiting for approval from HCFA bureaucrats, also means the elderly could take advantage of changes in treatments, medical procedures, and service delivery innovations -- something lacking in today's Medicare. The only large elderly group with access to similar breakthroughs today are retired Members of Congress and federal employees.

- Value for Money. Like federal and congressional retirees, Medicare beneficiaries would be able to pocket any savings from their personal decisions. While the cost of health care is considerably higher for the elderly than for active workers and their families, the government contribution to their health plans also would be higher, depending on differences in age, sex, and geography.36

- Controlling Costs. While by no means a perfect market, the FEHBP has been able to control costs better than either private, employer-based insurance or the current Medicare program, according to the Congressional Budget Office and such private econometric firms as Lewin-ICF.37 This success is due in large part to the ability of Members of Congress and other federal workers, families, and retirees to shop among the various health plans in their geographic regions to get the best value for their money. In recent years, even though the FEHBP enrolls approximately 1.6 million higher-cost retirees and dependents and includes progressively higher benefits, outlays have increased at a much slower rate than the Medicare program's.38 With the establishment of a Medi-Choice system similar in structure to the current FEHBP, the powerful market forces of consumer choice and competition should produce similar dynamics and results in the Medicare program.

- Reduced Red Tape and Bureaucracy. To improve administration, Congress could relieve the Health Care Financing Administration of trying to dictate the minutiae of virtually every facet of health care financing and delivery for the nation's elderly. Instead of administering complex, cumbersome, and economically inefficient price controls or promulgating a seemingly endless stream of rules, regulations, and guidelines, HCFA could simply transmit defined contributions, either as vouchers or through electronic transmissions, to the plans chosen by enrollees, certify private plans as meeting basic hospital and physicians benefits, meet fiscal solvency requirements, and guarantee catastrophic coverage (a benefit Medicare does not provide). Moreover, HCFA could promulgate and enforce rules protecting elderly citizens from fraud by insurance companies.

An AARP Health Plan?

Much like the National Association of Retired Federal Employees (NARFE), which rates and grades the quality and benefits of plans offered to congressional and federal retirees, the American Association of Retired Persons (AARP) and other senior citizens' organizations could play an important role in a revamped Medicare system by rating and approving competing plans on the basis of price, service, quality, and benefits. In fact, there is every opportunity for organizations like the AARP to sponsor and market their own health care plans in competition with established insurance carriers, as do certain federal unions and employee organizations within the FEHBP.

CONCLUSION

Unless Congress acts soon, Medicare costs will continue to rise at unsustainable rates and the program will become insolvent. The Medicare program is structurally unsound. It provides a false sense of security for the nation's elderly. Attempts to hold down annual cost increases of more than 10 percent per year through arbitrary price controls have failed. The Health Care Financing Administration has become entrenched, intrusive, and overly bureaucratic, issuing volumes of rules, regulations, and guidelines that are confusing not only to the public and lawmakers, but also to doctors, hospital administrators, and patients.

The new debate over Medicare reform is one of the most important since Congress debated comprehensive health care reform last year. Congress must make decisions that affect the lives of every American, working or retired, rich or poor, healthy or ill. It is imperative that participants in this debate, particularly Members of Congress, focus their attention not only on the financial health, but also on the administrative structure, including the regulatory details, of the Medicare system. While pursuing necessary spending restraints in Medicare and other government programs in order to secure an end to ruinous deficits, lawmakers also must begin a fundamental restructuring of the program with a view toward improving the quality, availability, and security of health services for the elderly well into the next century.

If Congress fails to institute fundamental reform, either the elderly will be faced with a dramatic reduction in the quantity and the quality of their health care coverage, or already overburdened working families will be forced to pay sharply higher payroll taxes just to maintain the current level of benefits. Either consequence is tantamount to fiscal and political disaster. But if Congress uses this historic opportunity to create a new Medicare system based on consumer choice and competition, it will mean health care choice and security for today's elderly and a strong and solvent retirement health care system for future generations of Americans as well.

Endnotes

(1) House Speaker John W. McCormack (D-MA), during floor debate in the U.S. House of Representatives on April 8, 1965.

(2) 1995 Annual Report of the Board of Trustees of the Federal Hospital Insurance Trust Fund, pp. 2, 8.

(3) Ibid., p. 27.

(4) 1995 Annual Report of the Board of Trustees of the Federal Supplementary Medical Insurance Trust Fund, p. 3.

(5) Ibid., p. 9.

(6) Edmund F. Haislmaier and Robert E. Moffit, "The Medicare Relative Value Scale: Comparable Worth for Doctors," Heritage Foundation Backgrounder No. 732, October 25, 1989, p. 11.

(7) See Stuart M. Butler, "The Fatal Attraction of Price Controls," in Robert B. Helms, Health Policy Reform: Competition and Controls (Washington, D.C.: The AEI Press, 1993).

(8) See Haislmaier and Moffit, "The Medicare Relative Value Scale: Comparable Worth for Doctors."

(9) For a discussion of the physicians Medicare reimbursement system, see Robert E. Moffit, "Back to the Future: Medicare's Resurrection of the Labor Theory of Value," Regulation, Vol. 15, No. 4 (Fall 1992), pp. 54-63.; Robert E. Moffit, "Comparable Worth for Doctors: A Severe Case of Government Malpractice," Heritage Foundation Backgrounder No. 855, September 23, 1991.

(10) For a fuller discussion of the unworkability of price controls in the health care sector of the economy, see Edmund F. Haislmaier, "Why Global Budgets and Price Controls Will Not Curb Health Costs," Heritage Foundation Backgrounder No. 929, March 8, 1993.

(11) Robert E. Moffit, Ph.D., "Open Season for America? A Symposium on the Federal Employees Health Benefits Program," Heritage Lecture No. 431, November 9, 1992, p. 1.

(12) Tim Friend, "Clinical Trials in U.S. Called Endangered," USA Today , May 10, 1995, p. 2A.

(13) Response to questions by John Rowe, M.D., before Senate Finance Committee, May 16, 1995.

(14) General Accounting Office, "Medicare, Health Maintenance Organization Rate-Setting Issues," GAO Report to Congressional Committees, January 1989, GAO/HRD-89-46, p. 4.

(15) Gail R. Wilensky, testimony before Subcommittee on Health, Committee on Ways and Means, U.S. House of Representatives, February 7, 1995.

(16) 1995 Annual Report [HI], p. 4; 1995 Annual Report [SMI], p. 3.

(17) In reality the 1.45 percent tax on employers is a tax on employees, since businesses see it as a cost of employment to be deducted from the wages they are willing to pay.

(18) The HI tax was first levied in 1966 at a rate of 0.35 percent (on both employee and employer) on earnings up to $6,600 a year.

(19) David Koitz, "Medicare: President Clinton's Proposal to Eliminate the Hospital Insurance Taxable Earnings Base," CRS Report for Congress, Congressional Research Service, Library of Congress, May 5, 1993, p. 4.

(20) Michelle Davis, "Medicare's Self-Destruction," Citizens for a Sound Economy, Economic Perspective, January 22, 1993, p. 4.

(21) C. Eugene Steuerle, testimony before Committee on the Budget, U.S. House of Representatives, March 22, 1995.

(22) 1995 Annual Report [HI], p. 3.

(23) Ibid.

(24) 1995 Annual Report [SMI], p. 3.

(25) Ibid., p. 9.

(26) This and other short-term budgetary proposals for dealing with the Medicare system are discussed in Scott A. Hodge, ed., Rolling Back Government: A Budget Plan to Rebuild America (Washington, D.C.: The Heritage Foundation, 1995).

(27) See Robert E. Moffit, "Consumer Choice in Health: Learning from the Federal Employees Health Benefits Program," Heritage Foundation Backgrounder No. 878, February 6, 1992.

(28) Whether or not a child will be added to a family plan of a survivor depends upon the family status: "The deciding factor now is whether or not the grandchild would have qualified as a family member if the retired employee were still alive." See National Association of Retired Federal Employees, Federal Health Benefits Information and Open Season Guide, 1995 (Washington D.C., 1994), p. 28.

(29) Carolyn Pemberton and Deborah Holmes, eds., EBRI Databook on Employee Benefits (Washington D.C.: Employee Benefit Research Institute, 1995), p. 278.

(30) Ibid.

(31) See NARFE, Federal Health Benefits Information and Open Season Guide, 1995, p. 11.

(32)Ibid., pp. 55-62.

(33) Congressional Budget Office,Reducing the Deficit: Spending and Revenue Options, A Report to the Senate and House Committees on the Budget (February 1995), p. 184.

(34) Ibid., p. 225.

(35) For example, rather than simply approving insurance carriers, OPM still tries to negotiate rates and benefits for hundreds of plans -- although premium prices in reality must meet the test of market demand. Moreover, reversing a historical pattern of "passive management," the Clinton Administration has in some instances required the inclusion in plans of certain controversial services. And Congress recently imposed the Medicare fee schedule, although it restricted it to services for federal retirees.

(36) The authors believe that the demographic risk factors are sufficient to protect health plans from undue "adverse selection." However, if Congress determined that additional risk adjusters were needed, they could be added.

(37) As noted earlier, one central weakness of the FEHBP is its outdated insurance underwriting practices. It currently uses a crude form of community rating, with no distinction in premium payments for active and retired federal workers and their families. This arrangement also contributes directly to the persistent problem of "adverse selection" in the FEHBP. The problems could be largely eliminated by an adjustment in the FEHBP premium structure that instituted higher premiums for retirees than for active workers, along with an increase in the government contribution to retirees' chosen plans or a tax credit for federal retirees to offset the increased cost. For a discussion of how to improve the FEHBP, see Moffit, "Consumer Choice in Health: Learning from the Federal Employees Health Benefits Program," pp. 17-19; see also Stuart M. Butler, "Reforming Health Insurance: Analyzing Objections to the Nickles-Stearns Bill," Heritage Foundation Issue Bulletin No. 193, June 14, 1994.

(38) Allen Dobson, Rob Mechanic, and Kellie Mitra, Comparision of Premium Trends for Federal Employees Health Benefits Program to Private Sector Premium Trends and other Market Indicators (Fairfax, Va.: Lewin-ICF, 1992).

(39) Office of Personnel Management, Office of Actuaries, Table entitled "Federal Employees Health Benefit Program, 1992 Contracts."