Social Security’s main program, also known as Old-Age and Survivors Insurance (OASI), ran a $39 billion deficit in 2014, closing out five years of consecutive cash-flow deficits as the program’s unfunded obligations continue to grow.[1] According to the 2015 annual Trustees’ Report, the 75-year unfunded obligation of the Social Security OASI Trust Fund is $9.43 trillion, a $70 billion increase from last year’s unfunded obligation of $9.36 trillion.[2] After including federal debt obligations recorded as assets to the Social Security trust fund of $2.73 trillion, Social Security’s total 75-year unfunded obligation is nearly $12.2 trillion.

The Social Security OASI program is projected to reach insolvency in 2035. This means that the program is expected to have only enough revenue from payroll taxes, interest on the Trust Fund balance, and repayment of borrowed Trust Fund dollars to pay out scheduled benefits until 2035. This is one year later than projected in last year’s report.[3]

If no action is taken to improve Social Security’s solvency before its Trust Fund runs dry, benefits will either be delayed or reduced across the board by 23 percent. Congress should avoid indiscriminate benefit cuts which would harm the most vulnerable beneficiaries the most by adopting commonsense reforms that modernize the outdated Social Security program.

Social Security Is Already Adding to the Deficit

While Social Security’s OASI program is considered to be solvent on paper through 2035, Social Security’s cash-flow deficit is already adding to the federal budget deficit.

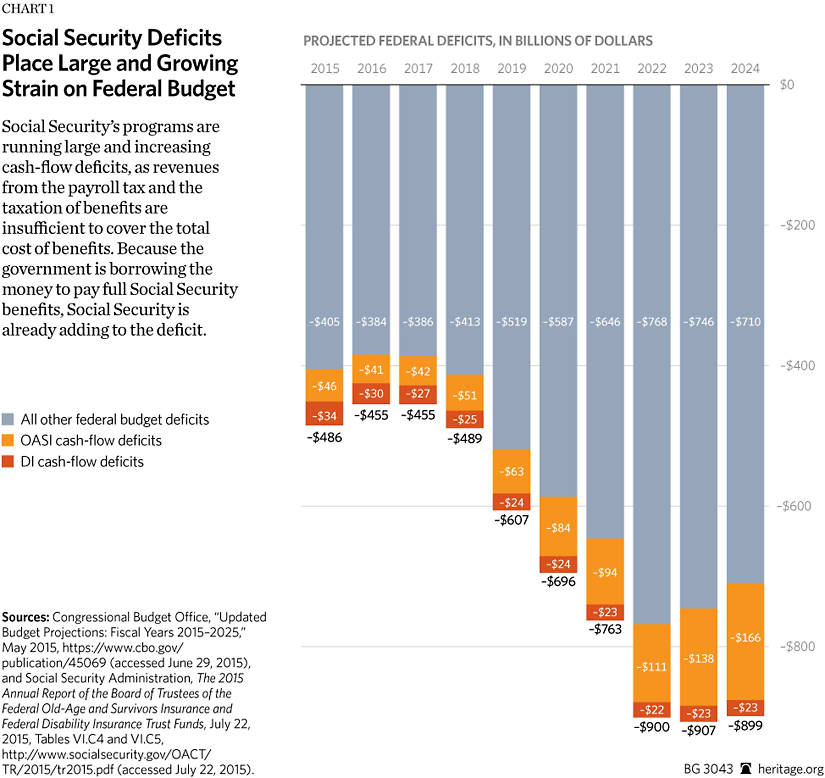

Since 2010, the OASI program has taken in less money from payroll tax revenues and the taxation of benefits than it pays out in benefits, generating cash-flow deficits. The 2014 cash-flow deficit was $39 billion. Over the next 10 years, the OASI program’s cumulative cash-flow deficit will amount to $840 billion, according to the trustees’ intermediate assumptions. For as long as the federal government is running deficits in excess of Social Security’s cash-flow deficits, we can assume that this $840 billion shortfall will be matched dollar for dollar by an increase in the public debt.

Social Security’s cash-flow deficits add to the public debt because, in order to pay full Social Security benefits, the Treasury Department has to raise cash in excess of what it receives from the payroll tax and the taxation of benefits. Cash-flow deficits mean that the Treasury can no longer pay all Social Security benefits from the program’s tax income alone. Instead, Treasury must produce additional cash from taxes or borrowing. With annual federal deficits in excess of Social Security’s cash-flow deficit, the OASI program is already adding to the deficit.

What About the Trust Fund?

In the past, when Social Security ran cash-flow surpluses, the federal government spent those surpluses on other federal spending, and in return, the Treasury credited Social Security’s Trust Fund with special-issue government securities. Although this $2.73 trillion in securities is not counted in the total amount of debt held by the public, it represents real debt that will have to be repaid over the coming decades, unless Congress changes current law.[4]

The Social Security Trust Fund represents legitimate repayments plus interest, but this distinction has no bearing on the federal budget’s bottom line. Congress spent all the excess revenues when Social Security was running surpluses, and now repaying those revenues is adding to deficits. As Chart 1 shows, shortfalls in Social Security’s programs represent a considerable portion of current and future deficits.

Nevertheless, Congress may change current law at any time, including by eliminating the Social Security Trust Fund. Funds earmarked for OASI through its Trust Fund do not represent accrued property rights, even though these funds come from taxing workers’ wages. Congress’s authority to modify the Social Security program was affirmed in the 1960 Supreme Court decision in Flemming v. Nestor, wherein the Court held that individuals do not have a “property right” to their Social Security benefits, regardless of how many years they paid payroll taxes.[5]

Harmful Payroll Tax Increases

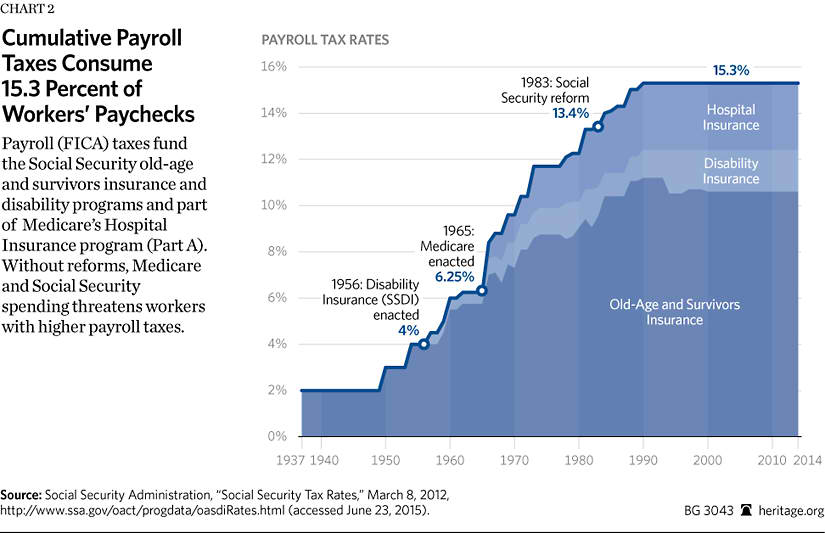

The Congressional Budget Office (CBO) analyzed how large of a payroll tax increase would be necessary, absent benefit reforms, to ensure Social Security’s on-paper solvency for the next 75 years. The CBO identified that the payroll tax would have to be permanently increased immediately from 12.4 percent to 15.9 percent—a nearly one-third increase—to ensure the solvency of Social Security’s combined Trust Funds (OASI and disability insurance).[6]

This substantial tax increase would harm those whom Social Security is intended to benefit the most. Under the 15.9 percent rate, someone earning $50,000 would pay an additional $1,750 per year in payroll taxes (half paid by his or her employer, unless the person is self-employed). This increase would put significant strain on middle-income and lower-income earners and would exacerbate the payroll tax’s disincentives to work.[7] The tax increase would also disproportionately fall on younger Americans. While lifetime payroll taxes would increase by 6 percent to 9 percent for those born in the 1960s, the new rate would amount to a 27 percent lifetime increase in payroll taxes for Americans born after 2000.[8] Moreover, a payroll tax increase would leave workers with even fewer resources to spend or save in accordance with their own needs and desires.

Another proposal suggests raising or eliminating the payroll tax cap. Social Security payroll taxes apply to the first $118,500 in wage earnings to prevent workers with very high incomes from receiving unnecessarily high benefits under the current benefit formula.

Raising, or eliminating, the payroll tax cap would not solve Social Security’s financial shortfalls. It would impose economically damaging marginal tax rates on middle-income and upper-income earners, which would reduce incomes and overall economic growth while generating very little net revenue.

Had Congress eliminated the cap in 2015, workers earning $150,000 would have experienced a 27 percent payroll tax increase, amounting to an extra $3,906 on their tax bills. A single-earner family with $250,000 income would pay $16,306 more in payroll taxes—more than doubling their current payroll tax burden.[9] This tax hike would be in addition to income taxes, which already disproportionately tax high-income earners. Moreover, this option would generate surpluses in the early years of adoption, which Congress would immediately spend, thus generating largely on-paper savings without markedly improving future deficits. Empirical evidence suggests that Social Security surpluses, rather than being saved, have gone toward higher spending or lower tax revenues than would have otherwise been the case.[10] Thus, options that create temporary Social Security surpluses merely give the appearance, on paper, of financial improvement in Social Security.[11]

Dismal Returns for Current and Future Retirees

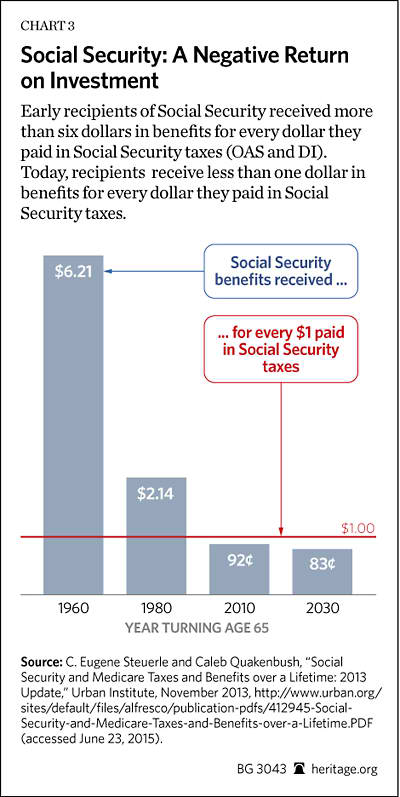

For decades, Social Security recipients received more in benefits than they paid into the system, but this is no longer the case for recent and future recipients. An analysis by the Urban Institute revealed that an average-earning male who reached age 65 in 1960 received $6.21 in Social Security benefits for every dollar he paid in Social Security taxes. This ratio has declined over time to $2.14 per dollar paid by workers who reached age 65 in 1980. For recent and future recipients, Social Security will provide a negative rate of return: Workers who reached age 65 in 2010 will receive 92 cents for every dollar paid in taxes, and workers who reach age 65 in 2030 will receive only 83 cents for every dollar in payroll taxes paid.[12]

As Social Security has shifted from a program to protect the elderly from poverty to a potential decades-long income subsidy, current workers and younger generations will inevitably bear the burden of Social Security’s drain on the federal budget. Raising payroll taxes on today’s and tomorrow’s workers to cover Social Security’s funding shortfall would further add to their burden, while also harming the economy.

Social Security Benefit Reforms

The sooner lawmakers address Social Security’s massive and growing cash-flow deficits, the lower the burden will be on current and future workers. Four important reforms could help resolve Social Security’s financial shortfall and return the program to its original purpose of protecting seniors against poverty. Congress should:

- Fix Social Security’s cost-of-living adjustment. Social Security’s cost-of-living adjustment (COLA) is based on an outdated measure of changes in the cost of living that fails to account for how people react to changes in prices. Lawmakers should index Social Security’s COLA to the chained consumer price index (CPI), which acknowledges that people choose less expensive and different goods and services in response to changes in prices. This would more accurately protect the value of benefits against changes in the cost of living while improving Social Security’s finances.[13]

- Raise the early and full retirement ages. Since 1950, life expectancy at birth in the United States has increased by more than 10 years, while life expectancy at age 65 has increased by more than five years.[14] At the same time, work in the United States has become less physically demanding and individuals have become healthier.[15] Yet Social Security’s full retirement age will gradually increase by only two years by 2027, to 67, and the early retirement age has not increased at all. Social Security’s retirement age serves as an implicit guideline for actual retirement, as nearly two-thirds of eligible workers choose to receive Social Security benefits between the early and full retirement age. For Social Security, this means greater financial strain, and for the economy, it means a smaller workforce, lower economic growth, less retirement security, and lower revenue. Lawmakers should gradually and predictably increase the early and full retirement ages to 65 and 70, and then index both to increases in life expectancy.

- Focus Social Security benefits on those who need them most. Social Security was first proposed as a program to protect the elderly from poverty, yet today it pays benefits to more than 47,000 millionaires and leaves many low-income recipients in need of additional welfare benefits.[16] Lawmakers should phase out benefits for retirees with high levels of non–Social Security income and provide a true system of social insurance that focuses on seniors who need it most.

- Implement a flat benefit structure. Congress should put Social Security benefits on a schedule to gradually arrive at a flat payment structure for those who work more than 35 years. This flat benefit payment should be sufficient to keep eligible seniors out of poverty throughout their retirement. Changing Social Security to this flat benefit that provides real insurance against poverty in retirement would provide certainty for seniors and ease the future tax burden on American workers. By enabling more Americans to accrue personal savings in private retirement accounts to complement Social Security’s flat benefit, lawmakers can reduce Americans’ reliance on government in retirement. Moreover, because savings invested in the productive sectors of the economy accrue larger returns than what most Americans can expect to receive from their Social Security payroll taxes, Americans will be able to afford more generous retirements or save less to maintain current benefit levels.

Social Security Needs Reform Today

Social Security is approaching insolvency in less than 20 years. The largest and growing federal entitlement program is increasingly contributing to annual deficits. Absent reform, Social Security benefits will be cut across the board by 23 percent in 2035. Action should be taken this year to protect Social Security’s most vulnerable beneficiaries from such drastic cuts without burdening younger generations with higher taxes or unsustainable debt. Lawmakers should immediately replace the current COLA with the more accurate chained CPI, raise the early and full retirement ages gradually and predictably, focus Social Security benefits on those who need them most, and enable more Americans to save for the future in private retirement accounts.

—Romina Boccia is Grover M. Hermann Research Fellow in Federal Budgetary Affairs and Research Manager in the Thomas A. Roe Institute for Economic Policy Studies, of the Institute for Economic Freedom and Opportunity, at The Heritage Foundation.