More than 80 years ago, Congress passed a series of laws that significantly expanded the federal government’s presence in the housing finance system. These federal programs have grown and contributed to an explosion of mortgage debt over the past few decades. Homeownership rates, however, have barely changed since the late 1960s.

The long-term increase in mortgage debt spurred by these federal programs exposes homeowners and taxpayers to significant financial risks. The government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, which still reside in federal conservatorship, received significant attention after a $200 billion bailout in 2008. Less known is that the Federal Housing Administration (FHA) needed an infusion of $2 billion in taxpayer money in 2013.

Created in 1934, the FHA is a federal agency responsible for several mortgage insurance programs. The FHA charges fees to provide lenders with full loan-loss coverage on mortgages. This coverage allows lenders to recover the full amount of the loan from the FHA when a borrower defaults on a loan. The FHA charges borrowers fees to cover the cost of this loan insurance, but the FHA has a history of not charging high enough fees to cover all of its losses. Taxpayers are liable for the difference, and private firms are crowded out of the market because they cannot easily compete with underpriced government insurance. Despite various reform initiatives since the 1930s, the FHA has consistently had trouble meeting safety and soundness guidelines, has undermined the stability of the housing market, and in recent years has needed several billion dollars to cover its losses.

In return for the substantial costs to taxpayers, the FHA’s mortgage insurance programs have had minimal impact on homeownership rates. This suggests that additional FHA reforms will, at best, provide merely temporary financial improvements to the agency without adding appreciable benefits to the housing market. Congress should take the steps necessary to get the federal government out of the home financing business.

Origins of FHA and Federal Home Financing Policy

Before the 1930s, many homeowners had various types of interest-only, short-term mortgages with balloon payments that often required refinancing. State laws before the Great Depression dictated a variety of specific provisions in loan contracts, such as the length of the contract (the term) and the loan-to-value (LTV) ratio. With no particular pattern, some states prohibited banks from loaning more than 50 percent, 67 percent, or 80 percent of the value of a home for terms typically between five years and 15 years. For example, in Pennsylvania from 1913 to 1937, banks could not legally lend more than two-thirds of the property’s value (i.e., an LTV of 66.7 percent), and loans could not exceed a term of 15 years.[1]

A great deal of private innovation led to a general lengthening of loan terms and products that allowed people to finance a larger portion of a home’s purchase price, but the practice of frequent refinancing persisted throughout the 1920s.[2] This refinancing feature, along with massive job losses and a collapse in home prices, contributed to the failure of many banks and private mortgage insurance companies during the 1930s. Naturally, many of the more activist polices of the 1930s addressed this very aspect of home financing because it became such a problem during the Depression, with many banks becoming insolvent when homeowners defaulted on home mortgages that exceeded the value of the underlying homes.

One of the principal federal agencies created to deal with this issue in 1934 was the Federal Housing Administration. The FHA provided lenders with mortgage insurance on “approved” loans, the very first of which was a 20-year fixed-rate mortgage with a 20 percent down payment (for no more than $16,000). This maximum loan amount was approximately three times the median home price in 1934, a fact that underscores that a main goal of the FHA was to stimulate construction jobs, not to assist low-income individuals.[3] Legal scholar Richard Bartke notes:

The primary purpose of the Act [that created the FHA] was to stimulate building and thereby increase employment. The increase in the amount and quality of housing in the country was merely a secondary consideration.[4]

When the federal government created the FHA, it also undertook policies to induce private companies (called associations) to purchase mortgages from banks, thus lowering banks’ financial risk while providing funds to build homes. When these private associations largely failed to materialize, the federal government created the Federal National Mortgage Association (Fannie Mae) in 1938.[5] Congress initially authorized Fannie Mae to purchase only FHA-insured loans to bring into the secondary market, but it was not supposed to make direct loans. However, Fannie effectively became a lender that competed with savings and loan associations (S&Ls), a main source of mortgage funding after the Depression.[6]

By the late 1930s, the S&Ls served local mortgage markets and small-scale builders, while FHA loans and Fannie Mae primarily funded commercial banks and mortgage companies that financed large-tract builders and multifamily projects. In the aftermath of World War II, Congress authorized the Veterans Administration (VA)[7] to insure low-interest, zero-down-payment home loans to returning U.S. servicemen.[8] Since this period, the FHA and the VA have been the principal federal agencies that provide home mortgage insurance.[9]

FHA’s Influence on Homeownership Rates

A major boom in housing corresponded roughly with the end of World War II and, therefore, with the operations of the newly created FHA and VA.[10] Thus, federal housing finance policy is often credited with causing an increase in homeownership. However, research suggests that all of the federal housing finance programs combined explain at most 13 percent of the growth in homeownership between 1940 and 1960. One study estimates that the VA programs alone accounted for approximately 7 percent of the overall increase from 1940 to 1960.[11]

In 1938, only four years after the FHA was created, FHA-backed loans accounted for just under 20 percent of new mortgage originations in the U.S.[12] Yet these FHA loans remained a small fraction of the overall market. For example, from 1949 to 1968,[13] government-backed mortgages accounted for no more than 6 percent of all mortgages in the market in any given year.[14] In other words, at least 94 percent of the mortgage market for this period received no federal backing of any kind. These federal programs almost certainly drove private lenders to offer loans with longer terms and lower down payments, but the evidence shows that these programs were not the main driver of increased homeownership before the 1970s.

Most importantly, the FHA has had a negligible impact on homeownership rates over the past several decades. Specifically, substantial research shows that the FHA’s single-family mortgage insurance portfolio has had little effect on increasing total homeownership. At best, the FHA has accelerated the purchase of a home by a few years.[15] In other words, if FHA mortgage holders had waited to borrow, they would have most likely done so in the conventional mortgage market instead of relying on government-insured loans.

Types of FHA Loan Insurance

From its inception, the FHA has managed two primary lines of loan insurance: single-family mortgage insurance and multifamily apartment mortgage insurance. In the 1950s, the FHA’s mission began expanding to promote “community development” through insurance on various types of health care facilities in addition to its other multifamily apartment programs.[16] Currently, the flagship FHA program guarantees single-family mortgages via the Mutual Mortgage Insurance Fund (MMIF).[17]

The MMIF principally insures two types of loans: single-family home mortgages (not exceeding four units) and home equity conversion mortgages (HECMs).[18] Both types of loans are available regardless of the borrower’s income.[19] The FHA also has a secondary focus on multifamily mortgage projects, which it manages through two separate insurance funds: the General Insurance Fund and the Special Risk Insurance Fund.[20] This paper focuses mainly on the FHA’s single-family mortgage insurance and its corresponding MMIF.

Over the 80-year history of the FHA’s single-family mortgage insurance practice, the agency has implemented many changes that have altered the underlying credit quality of the loans that it insures (loans-in-force). When the FHA weakens its underwriting standards and therefore the underlying quality of the loans that it insures, it reduces the agency’s ability to manage a self-supporting insurance operation. Thus, there is a fundamental trade-off involved in managing an insurance operation that seeks both to maintain the actuarial “safety and soundness” of the reserve fund and to serve an ever-expanding class of potential home buyers. In the face of this trade-off, the FHA has increasingly strived to expand access to mortgage credit to borrowers with weaker credit and income histories and lower levels of initial loan collateral, while trying to manage a self-supporting, actuarially sound insurance practice.

FHA’s Attempts to Influence Market Share

There is often confusion about the early mission of the FHA single-family mortgage program in the mistaken belief that the FHA was created to offer access to mortgages to underserved groups of individuals. In fact, the FHA started with relatively strict underwriting standards compared with those required of most loans today. Indeed, the FHA’s history exhibits a long-term drift in underwriting standards and the quality of loans insured in the program.

Deterioration in FHA Underwriting Standards. Starting in the mid-1950s, the FHA began to dramatically reduce the level of upfront collateral—the down payment—required to take on a home loan through its single-family mortgage program. By 1961, the maximum loan-to-value ratio allowed on new and existing homes was 97 percent (in other words, a 3 percent down payment).[21] More broadly, annual loan data from 1990 to 2014 shows that fewer than 10 percent of FHA-insured loans during those years would have qualified for eligibility during the first two decades the FHA’s existence.[22] The high percentage of low-collateral, highly leveraged FHA-insured loans puts borrowers at a higher risk of default and loan failure, increasing risk to both taxpayers and homeowners.[23]

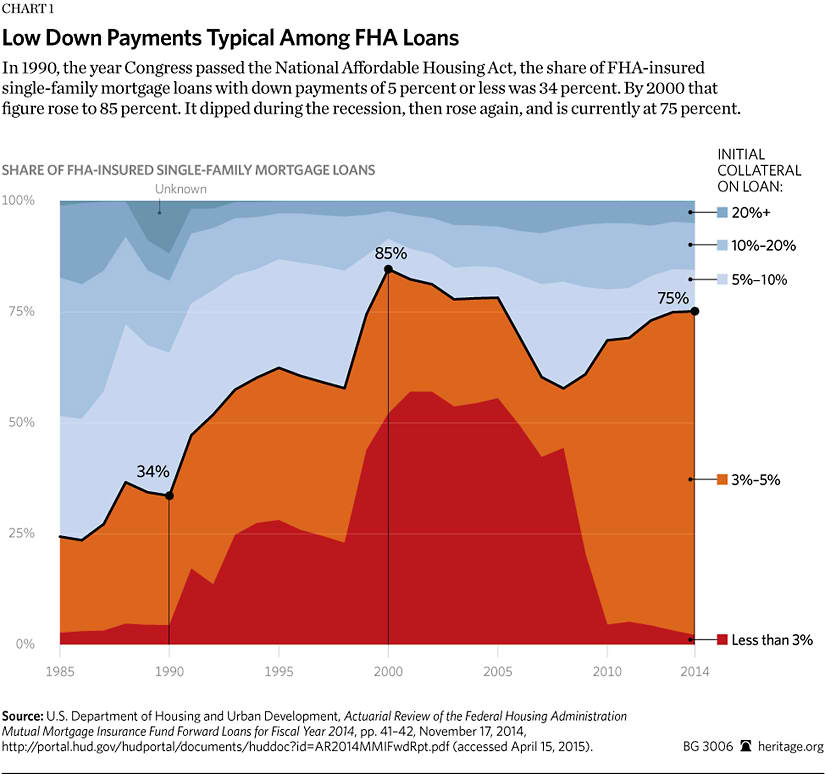

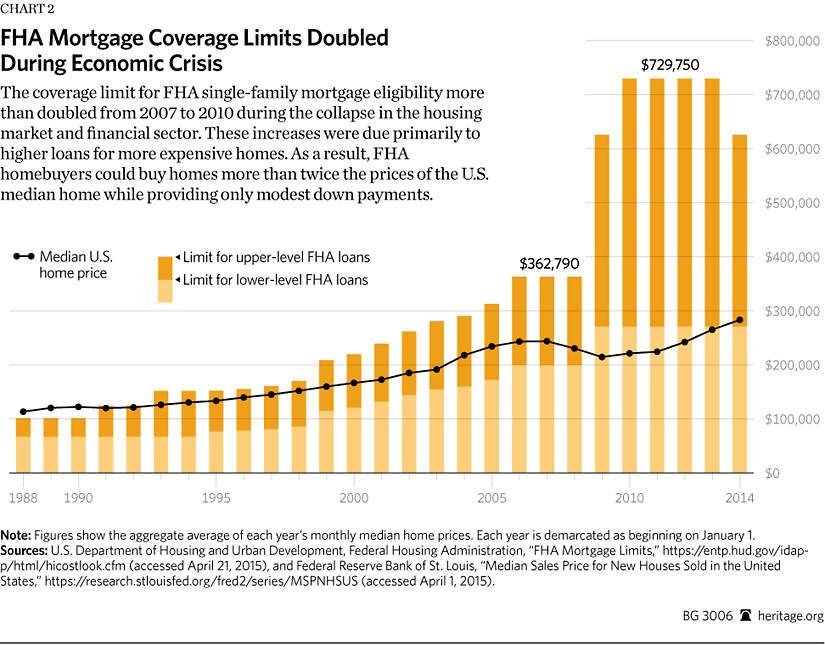

Dramatic Expansion in Loan Limit Coverage. From 2008 through 2013, the FHA dramatically increased its presence in the mortgage finance system, averaging about 23.3 percent of the purchase (non-refinance) market and 14.2 percent of the overall mortgage market (purchase and refinance). A crucial reason for this change in market share was a 100 percent increase in the coverage limit—that is, the maximum loan amount—for loans in the FHA program. In certain high-cost markets, the coverage change lifted the limit for mortgages over $700,000 on one-unit properties and $1.3 million on four-unit properties.

This increased presence marked a major reversal in the FHA’s role in the U.S. housing finance system. Prior to the change the FHA had held a much smaller position within the overall housing finance system for the past few decades. In 1971, three years after the passage of the Housing and Urban Development Act of 1968, the FHA accounted for approximately 15 percent of the purchase market.

Federal Taxpayer Subsidy Costs. Perhaps most importantly, over the years the FHA has garnered numerous credit funding advantages over its private-sector competitors. One of the most important advantages is the guarantee of the federal government during episodes of insolvency in the funds operation. Since the Federal Credit Reform Act (FCRA) of 1990, Congress has treated the FHA single-family mortgage insurance program as an on-budget taxpayer subsidy. U.S. taxpayers are obligated to cover any shortfalls in the MMIF with reserves in a capital reserve account.[24] This advantage surely lessens private firms’ incentive to enter the mortgage insurance market and, most likely, has prevented (crowded out) some private firms from entering the market.

Reserve Funds Amount to Budget Gimmicks

The Federal Credit Reform Act requires the FHA to maintain a 2 percent capital reserve ratio at all times. Private mortgage insurers, on the other hand, are generally required to hold around 4 percent in capital reserves to cover net losses on loans that they insure.[25] Aside from this lower requirement, the FHA’s capital reserve account is not really a reserve account at all. The FHA’s reserve merely represents credited budgetary surpluses (estimated annually).

Put differently, the FHA’s capital reserve account has no money, only an accounting of how much money would be in the account. In years that the Mutual Mortgage Insurance Fund program generates positive net income, the surplus (or subsidy “savings”) flows to the capital reserve account. In years that the MMIF program generates a net loss, this deficit (or subsidy “cost”) is “covered” by funds that were apportioned to the capital reserve account. Furthermore, in years that the FHA program generates a net loss of income and shows a capital reserve account of less than 2 percent, the FHA requires an additional appropriation to cover the deficit for that fiscal year.

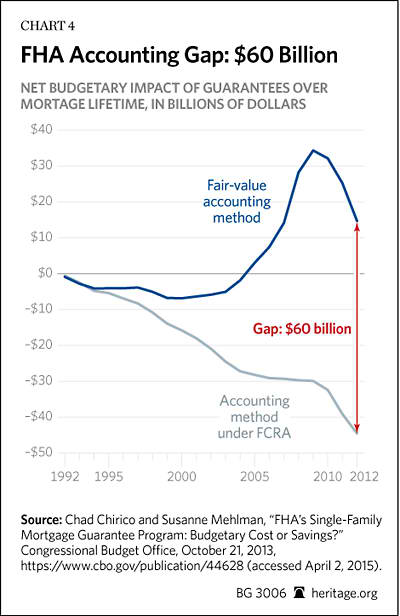

Historically, the FHA program has not needed to draw appropriations to cover annual deficits, but in recent years, the capital reserve account has been too low to cover the deficit in the MMIF program.[26] The MMIF subsidy cost estimate is sensitive to the choice of accounting methodology. Crucially, the FCRA accrual method significantly understates the costs of these insurance guarantee subsidies in the FHA single-family mortgage insurance practice.[27] In fact, between 1992 and 2012, there was a $60 billion difference between the accounting method required under the FCRA and a method that would more appropriately reflect market risk. The accrual accounting method shows the single-family mortgage insurance practice “saving” the taxpayer $45 billion compared with a “cost” of $15 billion using the fair-value accounting method.[28] In recent years, the FHA has treated the 2 percent capital reserve requirement casually. In 2012 and 2013, the FHA required several billion in appropriated funds to cover deficits in the MMIF program and the lack of loss reserves in the capital reserve account.

In summary, the on-budget subsidy treatment, federal taxpayer credit guarantee, and the relaxed capital reserve requirement are crucial market advantages for the FHA program. These funding advantages crowd out a portion of borrowers that would take up mortgages in the conventional market with credit enhancement through private mortgage insurers, as well as potential private mortgage insurance providers.

What Congress Should Do

The FHA has outlived its usefulness to taxpayers and homeowners. Federal policymakers should eliminate the federal government support and guidance in its single-family and multifamily mortgage insurance programs. This change would leave the mortgage insurance industry, outside of the guarantees in VA mortgage programs, principally in the domain of private market insurers.

Ideally, Congress would eliminate the FHA’s role in providing taxpayer-backed credit guarantees and mandating underwriting guidance affecting mortgages. Short of immediately ending the FHA mortgage insurance programs, Congress should phase down its presence in the mortgage market by:

- Increasing lender loan-loss liability. At a minimum, Congress should ensure that capital reserve requirement standards and recourse actions against lenders achieve parity with the private mortgage insurance industry. One reasonable step to take in the immediate future is to reduce the loan-loss coverage in the single-family mortgage insurance program from the current approximately 100 percent to 50 percent.[29] The ultimate goal should be to reduce the level of loan coverage to the private industry standard of 20 percent to 30 percent.

- Maintaining the statutorily required 2 percent capital reserves. The FHA must maintain at least a minimum of 2 percent reserves in its capital account. These reserve funds are necessary to maintain solvency and avoid appropriations from Congress to cover any shortfalls in the capital account. The FHA should immediately and aggressively take steps to ensure the capital reserve fund achieves the 2 percent capital ratio as required by law. One possibility is that the FHA could move from its tiered flat-rate premium structure toward a risk-based premium structure.

- Limiting the scope of eligible single-family mortgages. Congress should limit the FHA’s single-family insurance portfolio to first-time homebuyers, without any refinance eligibility over the tenure of the loans in force. Additionally, the value of loan limits eligible for FHA single-family mortgage insurance should decrease to the median home price in a given locality. These two reform measures would substantially reduce the FHA’s scope and move the FHA away from support of high-cost mortgages.

- Ending the multifamily mortgage insurance and the mortgage programs for health care facility and hospital construction. The federal taxpayer does not need to finance these commercial-based development initiatives. The FHA claims that it has a unique market advantage in providing “long-term loan amortization [up to 40 years in some cases] not found with conventional lending sources.”[30] All of these projects together comprise a small share of the overall FHA mortgage portfolio, and they have a longer history of needing appropriated capital transfers to cover financial shortfalls. These programs have also had the most problems with corruption and waste.[31] Despite recent efforts to increase efficiency in managing these mortgage programs, they are not necessary to maintain robust financing within the housing finance system.[32] Numerous other direct and indirect federal subsidies already support affordable rental assistance projects and other community development construction projects.

Conclusion

Over its more than 80 years of existence, the Federal Housing Administration has contributed to the long-run expansion in federally guaranteed mortgage debt in the U.S. financial system, increasing financial risk to both homeowners and taxpayers. In return for the substantial costs to taxpayers, the FHA’s mortgage insurance programs have had minimal impact on homeownership rates. Moreover, history suggests that additional reforms to the various FHA insurance programs will, at best, merely provide temporary financial improvements to the agency, without appreciable benefits to the housing market. Congress should therefore eliminate the FHA and get the federal government out of the home financing business.

—John L. Ligon is Senior Policy Analyst and Research Manager in the Center for Data Analysis, of the Institute for Economic Freedom and Opportunity, at The Heritage Foundation. Norbert J. Michel, PhD, is a Research Fellow in Financial Regulations in the Thomas A. Roe Institute for Economic Policy Studies, of the Institute for Economic Freedom and Opportunity, at The Heritage Foundation.