Robust mortgage financing exists in virtually every developed nation in the world without the degree of government involvement found in the U.S. While the U.S. homeownership rate is about average among developed nations, U.S. citizens typically pay among the highest interest rates in the industrialized world. Still, many groups argue that eliminating the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac would imperil mortgage financing in the U.S.

Some groups take the necessity of the GSE model even further, arguing that some form of government guarantee is needed to preserve specific mortgage products. In particular, groups such as the National Association of Realtors claim that a government guarantee is needed in the secondary market to ensure the widespread availability of the 30-year fixed-rate mortgage (FRM). Yet, is a GSE system really necessary to preserve the 30-year FRM? If so, should government policy promote any one mortgage product over others?

In this paper, we argue that it is misguided to justify broad government intervention and taxpayer guarantees in the U.S. housing finance system to preserve any type of mortgage product. Policymakers should reform the mortgage finance market by first recognizing that no single type of loan will be best for all borrowers at all times. At present, no single government policy guarantees the existence of the 30-year FRM, and Congress should not enact any such guarantee. On the other hand, policymakers can ensure that the private sector will create more mortgage products by eliminating the onerous regulations imposed by the 2010 Dodd–Frank Wall Street Reform and Consumer Protection Act.

The American Dream: To Own a Home, Not a Mortgage

Owning one’s own home is commonly viewed as part of the American Dream, and the benefits of homeownership likely extend beyond the individual to the community. When people own homes, they become more engaged in civic institutions that increase the value of the community and society. Evidence also indicates that these “spillover effects” exist in the U.S.[1] However, it does not follow that the federal government should undertake a policy of actively encouraging people to purchase homes, and encouraging people—especially those with low wealth—to finance home purchases with low-equity long-term debt makes little sense.

Nonetheless, government programs to boost homeownership in this manner have expanded nearly continuously since the 1930s.[2] Currently, the federal government controls a dominant share of the U.S. housing finance system, and it encourages borrowing by guaranteeing the operations of Fannie Mae, Freddie Mac, and Ginnie Mae.[3] The federal government also extends loan insurance through the Federal Housing Administration (FHA), the Veterans Affairs (VA) home-lending program, and the U.S. Department of Agriculture Rural Development Program.

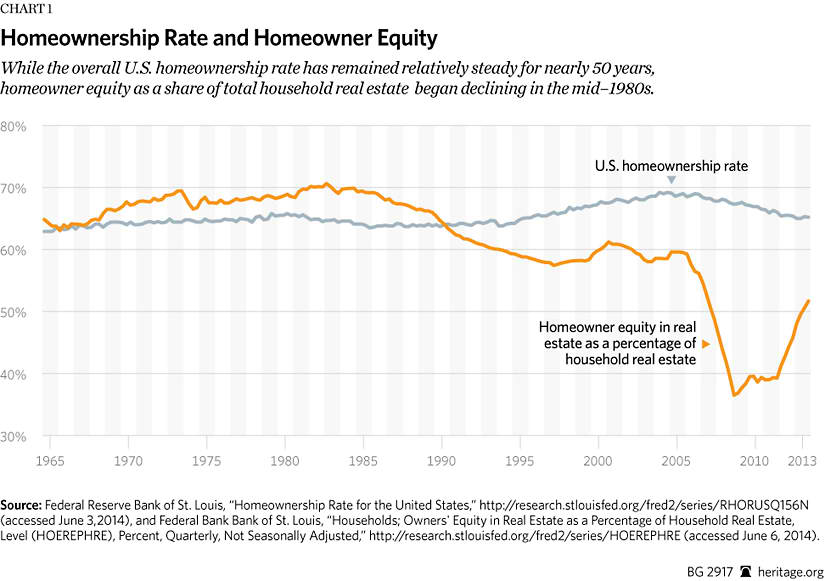

Outside the financial markets, the federal tax code promotes housing investment and consumption largely by allowing taxpayers to deduct mortgage interest from their federal income tax liability.[4] Yet, as government intervention has increased, the rate of U.S. homeownership has remained nearly constant over the past 50 years. On the other hand, the level of residential mortgage debt has increased nearly sixfold. Federal Reserve data show that inflation-adjusted mortgage debt increased from about $1.8 trillion in 1968 (the year Fannie became a GSE) to roughly $10 trillion in 2013.

Moreover, the level of equity that households have accumulated in their homes has trended downward since the 1980s and is approximately 20 percentage points lower than it was in the 1970s. (See Chart 1.) While countless government programs are touted as boosting homeownership, most government policies actually increase mortgage ownership. A large portion of this debt is in long-term FRMs, particularly 30-year FRMs. In most other countries, 30-year FRMs are not as prevalent.

U.S. Government Unique in Support of Mortgage Market

The U.S. is the only major country in the world with a federal government mortgage insurer, government guarantees of mortgage securities, and government-sponsored enterprises (GSEs) in housing finance. Comparing the U.S. with 11 other industrialized countries, only two have a government mortgage insurer (the Netherlands and Canada), two have government security guarantees (Canada and Japan), and two have GSEs (Japan and Korea).[5] The U.S. is the only major country with a housing finance system heavily geared toward the 30-year FRM for reasons that go well beyond the existence of the GSEs.

For instance, Canada and several Western European countries provide lenders with strong recourse protection that makes it very difficult for borrowers to walk away from mortgages.[6] This protection starkly contrasts with the U.S. system, where borrowers have very friendly bankruptcy laws, and lenders must satisfy liberal consumer protection laws. These rules vary by state, but overall, U.S. foreclosure laws favor the borrower more than in many other countries. Even in strict states such as Nevada, the foreclosure process can take years to complete, giving homeowners the option of staying in the home without making mortgage payments.[7]

Moreover, laws in many other countries force borrowers to accept some of the interest-rate risk on long-term FRMs by allowing monthly payments to vary with interest rates for the initial portion of the loan term. Long-term fixed-rate loans without government backing exist in some Western countries, such as Denmark and Germany, but in these countries it is more common to have fixed interest rates over shorter periods of time (five to 10 years) with options to reset for the overall longer-maturity loans.[8] Given the stronger recourse laws and more even distribution of financial risks, it is not surprising that mortgage default rates in Western Europe and Canada were much lower than in the U.S., even amid rapidly falling home prices during the recent crisis.[9]

More broadly, volatility of home prices and home construction from 1998 to 2009 in the U.S. was among the highest in the industrialized world.[10] The fact that the U.S. market was dominated by 30-year FRMs does not appear to have helped the U.S. to weather the 2008 crisis. Further explaining the crisis in the U.S., many of these long-term FRMs pose greater risks to taxpayers than to the financial institutions that originated and/or invested in them. Policies that shift mortgage risk away from financial firms and onto taxpayers have shaped U.S. mortgage markets for decades.

Brief History of Long-Term FRM and Government Policy

Long-term fixed-rate mortgages (15-year and 30-year FRMs) accounted for nearly 62 percent of all mortgages in the U.S. from 1990 to 2012.[11] In December 2012, the 30-year FRM accounted for more than 61 percent of the market. Yet, no single government policy is responsible for this high market share, but rather various policies instituted over many decades account for the prevalence of the 30-year FRMs. The Great Depression is typically cited as the period when these policies began, but federal involvement in housing actually started before the 1930s.

In fact, a major housing boom in the 1920s was fueled by a combination of expansionary monetary policy, federal promotional campaigns, and private market innovations.[12] Leading up to the 1920s, people typically financed homes with multiple mortgages, including at least one short-term loan that required refinancing approximately every five years.[13] Most private-market innovations centered around lengthening loan terms and enabling people to finance a larger portion of a home’s purchase price, but the refinancing feature lasted throughout the 1920s.

Many of the more activist polices of the 1930s addressed this aspect of home financing because it became a problem during the Depression. In particular, the refinancing feature along with massive job losses and a collapse in home prices contributed to the failure of many banks and private mortgage insurance companies during the 1930s. Many banks became insolvent when they had to refinance home mortgages that exceeded the value of the underlying home, loans that are now commonly referred to as being “underwater.”

Federal Policy Takes Hold in the Primary Market. Two federal agencies created to deal with this issue were the Home Owner’s Loan Corporation (HOLC) in 1933 and the Federal Housing Administration (FHA) in 1934. The HOLC bought short-term mortgages that had defaulted and then restructured them into 20-year FRMs. The FHA, on the other hand, provided lenders with mortgage insurance on “approved” loans, the very first of which was a 20-year FRM with a 20 percent down payment (for no more than $16,000).[14] These two agencies expanded the use of long-term FRMs to lessen banks’ exposure to mortgage defaults and refinancing risk.[15]

FHA loan terms have been altered many times since the agency was created, and the 30-year FRM appeared in 1954.[16] For approximately two decades after the Depression, fear of that era’s refinancing problem led to a pervasive bias against adjustable rate mortgages (ARMs). For example, the Federal Home Loan Bank Board prohibited its member banks from providing ARMs.[17] Additionally, many states passed laws and issued regulations that either prohibited ARMs or restricted their use.

Thus, government policies promoted FRMs and simultaneously discouraged the use of ARMs to deal with Depression-era financial problems long after the Great Depression. These policies had the complementary goals of removing risk from the banking sector and providing more funds to boost housing construction jobs. While the FHA and HOLC had an immediate impact on housing finance, government polices took much longer to have a major impact on the secondary mortgage market.

The Secondary Market Takes Shape, Slowly. A nascent version of a private secondary mortgage market, in which banks sell home mortgages to a third party, surfaced in the 1920s, but was destroyed by the housing price collapse of the 1930s. Federal efforts to restart this market in the early 1930s were unsuccessful, but the goal of those policies was to induce private companies (called associations) to buy mortgages from banks, thus lowering banks’ financial risk while providing funds to build homes.[18] When private associations failed to materialize, the federal government created the Federal National Mortgage Association (Fannie Mae) in 1938.[19]

Congress initially authorized Fannie Mae to purchase only FHA-insured loans to bring into the secondary market. At first, Fannie was effectively a lender that competed with savings and loan associations (S&Ls), a main source of mortgage funding after the Depression. Fannie’s operations only made life easier for the S&Ls’ competitors—private firms known as mortgage companies. These companies did not have access to customer deposits like the S&Ls, so they relied on Fannie Mae to provide them with funds for originating mortgages. At least as far back as 1959, mortgage companies actively lobbied for federal support of their operations.[20] In 1970, mortgage companies effectively got their wish.

Fannie Mae completed its transition to a quasi-private government-sponsored enterprise (GSE) in 1970, when for the first time, it was authorized to buy mortgages that are not insured by the government (referred to as conventional loans). Congress also passed the Emergency Home Finance Act of 1970, which created the Federal Home Loan Mortgage Corporation (Freddie Mac). Freddie was started specifically to alleviate S&Ls’ financial difficulties by expanding the secondary mortgage market for these institutions.[21]

Initially, only Freddie Mac issued mortgage-backed securities (MBS), while Fannie Mae continued to function more like a lending institution. Throughout the 1970s, Fannie and Freddie worked to standardize conventional loan documents to further boost the secondary market, and Fannie finally issued its own MBS in 1981. This timing was somewhat fortuitous because the GSEs’ conventional secondary mortgage market filled a huge funding void after the S&Ls crashed in the late 1980s.[22] Interestingly, the fact that the market consisted mostly of FRMs contributed to the S&L crash and also to Fannie Mae’s insolvency.[23]

Policymakers gradually removed ARM lending restrictions as they recognized that a mortgage market dominated by FRMs was not a good match for the volatile inflationary environment of the late 1960s and 1970s. By 1988, ARMs had approximately 60 percent of the U.S. market, nearly the same share currently held by FRMs in the U.S.[24] This difference underscores the fact that no single mortgage product is ideally suited for all economic conditions.

Trade-offs and Risk in Mortgage Products

Diversification across mortgage products not only benefits the overall market, but also individual customers, who benefit from having more choices. Having many different options in available mortgage products is critical to a well-functioning market because borrowers’ needs vary and frequently change. For example, many potential borrowers may want a short-term, interest-only loan because they expect to move and/or sell their home within a year or so. Similarly, lenders may find that they can best provide home financing by creating new mortgage products that do not yet exist in the U.S.

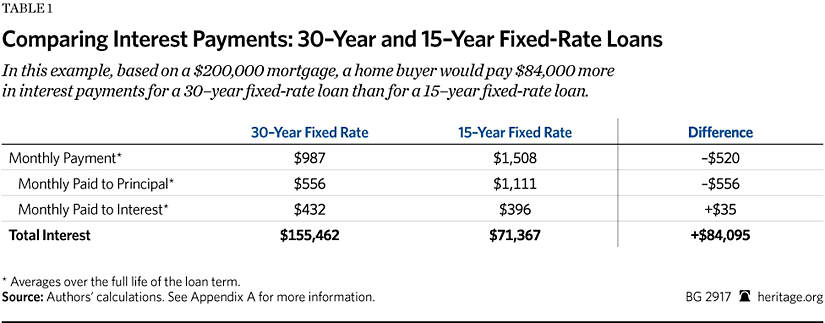

Different mortgage products have different risks with different trade-offs for borrowers and lenders. Table 1 presents a comparison of 30-year and 15-year FRMs to highlight these trade-offs. Even though the 15-year FRM is usually available at a lower interest rate, these calculations use the same rate for both the 15-year and 30-year loans. In practice, the differences are even more pronounced than shown in Table 1. (For more details on these calculations, see Appendix A.) The example shows that borrowing $200,000 for 30 years results in a monthly payment that is $520 less than borrowing the same amount for only 15 years. Lengthening the loan term dramatically lowers the monthly payment, but drastically increases the total interest owed on the loan.

Table 1 shows that $200,000 borrowed at 30 years results in a total interest cost of $84,095 more than if it were borrowed for only 15 years. In other words, even at the same interest rate, the total interest cost for the 30-year loan is more than double the cost of the 15-year loan. This trade-off, lower monthly payments for higher interest costs, cannot be judged objectively. Some borrowers may find this trade-off completely acceptable while others might not. The fact that this higher interest is not spread evenly over the life of the loan can also influence borrowers’ decision to borrow at the longer term.

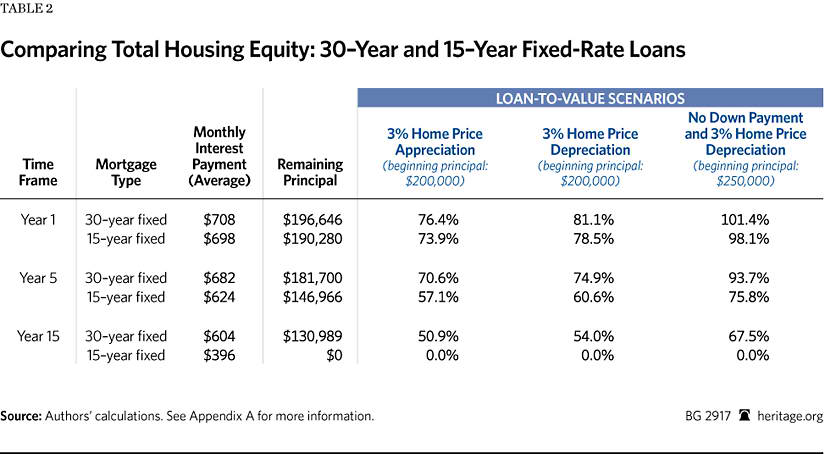

For all amortized loans (i.e., loans that allow for reduction in principal as opposed to interest-only loans), the monthly payment includes both principal and interest components. With everything else remaining constant, monthly payments on longer-term loans contain a larger proportion of interest at the beginning than payments on shorter-term mortgages do. In other words, the longer the term, the more time borrowers spend paying interest instead of paying off their loan balance. (See Table 2.) This additional time to pay off the balance constitutes an added risk for borrowers and lenders, which becomes apparent when the home must be sold.

Naturally, upon the sale of a home, any mortgage balance must be paid off before the homeowner receives any of the proceeds. For any given rate of home price appreciation, a borrower with a 30-year FRM will have less equity than one with a shorter-term mortgage.[25] In other words, the long-term borrower will owe the bank more than if they had borrowed at the shorter term. If home prices fall too much, long-term borrowers may be unable to pay off their loan balances with the proceeds from selling the home.

Still, a borrower’s decision to accept this risk in return for a lower monthly payment is purely subjective. Having the federal government tell borrowers that they can or cannot take out a 30-year mortgage is akin to telling workers whether they can invest in equities. In either case, by limiting choices in this manner, government regulators are assuming that they know which risks and benefits are best for all borrowers. Aside from the fact that policymakers cannot acquire this knowledge, the additional risks associated with mortgage lending suggest that polices should not favor any particular mortgage product.

Risks to Banks

When mortgages go underwater, both borrowers and lenders lose. Homes cannot be sold at a high enough price to pay off a mortgage, so borrowers remain in debt while lenders have nobody to pay them what is owed. In theory, this risk is shared by both borrower and lender, but in practice lenders in the U.S. bear most of the burden because many states have laws that favor the borrower when a mortgage goes underwater. In fact, many of these laws provide incentives for borrowers to walk away from underwater mortgages.

For example, in most states, borrowers who file bankruptcy cannot be forced to pay off their home mortgage with their other assets.[26] Even outside of bankruptcy, many U.S. states provide incentives for borrowers to stop making their mortgage payments, and foreclosures can take several years to complete, while the borrower is allowed to remain in the home. Lenders also bear a great deal of basic credit risk in a mortgage contract.

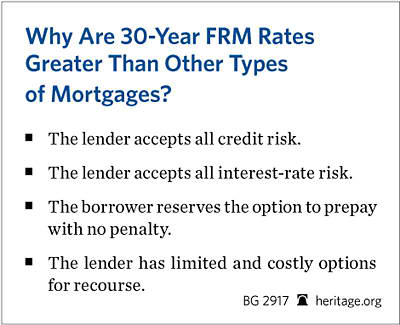

That is, lenders take on the risk that borrowers will make all of the scheduled payments for the life of a loan. The longer the term of the loan, the more risk that the loan will not be paid back. Another type of mortgage risk, referred to as interest-rate risk, is that the value of a mortgage falls when interest rates rise. For example, if a bank lends money at 4 percent interest on a 30-year FRM, it loses money when interest rates rise because it cannot earn the higher rate. On the other hand, FRM lenders are in a better position when rates fall because their existing loans pay a higher rate than any new loans would earn.

While these scenarios may appear to balance out—a rise in rates favors the fixed-term borrower while a fall in rates benefits the fixed-term lender—a key feature of the U.S. market pushes virtually all FRM interest-rate risk onto the lender. When interest rates fall, borrowers are virtually unrestricted from refinancing their loan by securing a new loan at a lower rate and paying off the old loan. Many state laws prohibit banks from charging borrowers fees (prepayment penalties) when they pay off a loan ahead of schedule. Furthermore, after 1979, Fannie Mae would only purchase FRMs without prepayment penalties.[27]

In many ways, these features make long-term FRMs in the U.S. a one-way bet for borrowers at the expense of lenders. As a result, lenders typically charge higher interest rates on long-term FRMs versus ARMs and shorter-term FRMs. The premium on 30-year FRMs effectively means that all U.S. borrowers who take on a 30-year FRM pay at least a portion of the costs to remain shielded from these risks. For instance, all 30-year FRM holders in the U.S. pay for the option to refinance when rates fall even though they may never refinance. On the other hand, ARMs typically have lower rates because borrowers share some of these risks—a difference that has been incorrectly identified as a key cause of the recent financial crisis.

The Recent Housing Crisis and False Narratives

There are numerous misconceptions about the recent crisis in the U.S. housing and financial markets that continue to shape the housing finance reform debate. One particularly common argument is that ARMs contributed to the crisis because of their “reset” feature, which changes a borrower’s monthly payment based on periodic changes in market interest rates. One problem with this story is that ARMs make up a relatively small share of the overall U.S. market.[28] More importantly, many ARM borrowers were not exposed to unique risks relative to those with FRMs.

While ARMs did lead to higher monthly payments for some borrowers, Federal Reserve data show that the majority of households holding ARMs were in delinquency before the reset occurred. Most ARM borrowers during this period were having problems making their mortgage payments before higher interest rates affected them.[29] In fact, only 12 percent of foreclosures between 2007 and 2010 were due to the payment reset on ARMs. The majority of foreclosures were on fixed-rate mortgages.[30]

Additionally, more than 80 percent of households that faced foreclosure during these years were making the same payment on their mortgage as when their loan was originated.[31] Thus, pervasive use of ARMs did not cause the recent housing crisis. What really mattered when home prices started to fall was not the type of mortgage product the household was holding, but the level of equity in the home.

Indeed, ample evidence suggests that negative equity, especially in a decreasing home price environment, is more of a factor in mortgage defaults than whether a borrower has an ARM or an FRM.[32] Both prime (ARM) and nonprime (FRM) borrowers with negative equity in their homes face a higher chance of defaulting on their mortgages.[33] While subprime mortgages generally pose a higher risk of default than prime mortgages, low-equity subprime mortgages face an even greater probability of default.[34]

For instance, Federal Reserve data show that subprime mortgages are about six times more likely than prime mortgages to result in foreclosure. Yet, the same data show that the combination of subprime homeownership with substantial negative equity increases the likelihood of mortgage default to 60 times that of a prime borrower with positive equity.[35] Overall, having some equity in a home is clearly a good way to protect against borrower default.

As discussed above, borrowers with 30-year FRMs take longer to build home equity compared with those with shorter-term FRMs and ARMs.[36] Starting in 2006, when home prices declined 15 percent nationally—nearly 60 percent in some regions of the U.S.—all mortgages backed with little-to-no equity were exposed to substantial default risk. Given the trends of higher debt and lower equity in the U.S., the spike in the rate of defaults and delinquencies in 2006 as home prices began to fall was not surprising.

Policy Recommendations

Policymakers should reform the mortgage finance market by first recognizing that no single type of loan will be best for all borrowers at all times. Congress should seek to remove obstructions so that private capital can flow to its most productive uses, not to preserve a product that some people may prefer. The first step should be to begin dismantling the regulations that Dodd–Frank imposed on the financial sector. Going forward, Congress’s best courses of action include:

- Shutting down Fannie Mae and Freddie Mac. Congress should get the federal government out of the U.S. housing finance market. A good first step would be to adopt some of the policies outlined in either Chairman Jeb Hensarling’s (R–TX) Protect American Taxpayers and Homeowners (PATH) Act or Representative Justin Amash’s (R–MI) New Fair Deal Banking and Housing Stability Act.

- Eliminating any semblance of affordable housing goals for lenders. Lenders should assess borrowers’ credit risk, not implement politicians’ favored social policies. Short of a full repeal of the Dodd–Frank Act, Congress should eliminate the Consumer Financial Protection Bureau (CFPB), the federal agency that enforces Dodd–Frank’s new mortgage regulations. Short of eliminating the CFPB, Congress can remove barriers to capital formation by eliminating the ability-to-repay rule, the qualified mortgage, disparate impact, and all of the mortgage servicing rules imposed by Dodd–Frank.

Conclusion

The 30-year FRM is now the dominant mortgage product in the U.S., but it did not become so pervasive simply because of the GSEs. Furthermore, 30-year FRMs exist in the U.S. without any government backing in the jumbo market, which is so named because its loans are larger than those eligible for GSE purchase. Supporters of the status quo point out that the 30-year FRM provides borrowers with long-term security, but they ignore certain costs and risks associated with a 30-year FRM. These risks exist, and government policies have typically attempted to shift these risks from financial markets to taxpayers.

The truth is no government policy can eliminate these financial risks, and the dangers associated with different types of debt vary as economic conditions change. History shows that policymakers tend to fight this reality with disastrous consequences. For instance, numerous government regulations contributed to the domination of U.S. markets by short-term adjustable rate mortgages (ARMs) in the 1920s, a factor that contributed to financial turmoil during the 1930s. Largely in response to those problems, policymakers implemented various policies so that mortgage markets would become dominated by long-term FRMs—a feature that caused financial hardship in the 1980s.

The secondary market operations of Fannie Mae and Freddie Mac certainly played a large role in shaping the U.S. mortgage market. FRMs’ domination of this market is the consequence of many economic events and government policies spread over decades. Even though no single federal government policy created or proliferated the conventional 30-year FRM, many interest groups claim that shutting down the GSEs would imperil the existence of the 30-year FRM. It is misguided to justify broad government intervention and taxpayer guarantees to preserve any one type of mortgage product, and there is no inherent reason that the 30-year FRM will not exist without the GSEs.

—John L. Ligon is Senior Policy Analyst and Research Manager in the Center for Data Analysis, of the Institute for Economic Freedom and Opportunity, at The Heritage Foundation. Norbert J. Michel, PhD, is Research Fellow in Financial Regulations in the Thomas A. Roe Institute for Economic Policy Studies of the Institute for Economic Freedom and Opportunity.

Appendix A

The data in the simplified examples in Table 1 and Table 2 are drawn from amortization schedules for a 15-year mortgage and a 30-year mortgage, each with loan principal of $200,000. The amortization schedules for both the 15-year and 30-year mortgage scenarios use a monthly periodic interest rate based on a fixed annual interest rate of 4.28 percent. Thus, for sake of comparison, there is no interest rate spread between the two mortgages. The calculations assume a fixed interest rate over the life of the loan with no recalibration to a lower fixed interest rate. Hence, the borrower does not exercise a prepayment option and does not borrow against accumulated positive equity.[37] Typically, interest rates on FRMs are higher than those on ARMs. For instance, over the past five years, the U.S. rate on the 15-year FRM averaged 75 basis points (0.75) below the 30-year FRM rate.[38] Moreover, most Americans do not stay in the same mortgage contract. The average length of tenure has historically been around six years, but this duration period has increased to around nine years during the recent turmoil in the housing market.[39]

In practice, the decision to take on a long-term fixed-rate mortgage is more complex than these examples suggest. For instance, the figures presented here say nothing about whether a household could otherwise make higher payments on a 15-year FRM and/or invest (in any mix of assets) the “difference” between the total payments for a 15-year FRM and 30-year FRM. In reality, these considerations can influence choices between various mortgage products and time horizons, especially for households in higher-income quintiles.[40]

The calculations in Table 2 assume that the change in the value of the home (home price depreciation or appreciation) is the total change from origination to the fixed point specified in the scenario (e.g., Mortgage Year 5). Thus, a 3 percent decrease in the home price in “Scenario Mortgage Year 5” corresponds to a home valued at $242,500 compared with the $250,000 at origination of the mortgage. The monthly interest payment is the average from the point of origination of the loan to the end of the specified fixed point (i.e., the end of 12-month period in the “Scenario Mortgage Year” specified).