For four decades, Japan’s economic growth was the envy of the world. From 1950 to 1991, Japan averaged annual real gross domestic product (GDP) growth of 6.8 percent, and recorded only a single year of economic contraction, in 1974. By the late 1980s, Japan had turned from postwar ruin into an affluent country with the second-largest economy in the world.

Starting in 1992, however, the Japanese economy entered a two-decade protracted malaise that has persisted until today. While the economy briefly recovered during the administration of Prime Minister Junichiro Koizumi in the middle of the last decade, it resumed its downward spiral during and after the 2008–2009 global recession.

Toward the end of 2012, Shinzo Abe was returned to power on the promise to finally resuscitate the economy. Two years later, his economic policies, nicknamed “Abenomics,” have yet to bear fruit. In fact, in mid-2014, the economy again slipped into recession.

Prime Minister Abe’s economic reforms— much more ambitious in scope than his predecessors’—rest on a three “arrows.” The first arrow is a series of fiscal expansions, the first one launched just weeks into Abe’s administration. The second arrow is a monetary expansion, to lift Japan out of its deflationary spiral, which was making the country’s debt burden even more onerous. The third arrow consists of a series of structural or long-term reforms meant to improve productivity, economic competitiveness, and long-term growth. These reforms, however, have been much slower and difficult to implement.

As Japan is a critical political and military ally in the Pacific, it is very much in the interests of the United States that these reforms bear fruit. A resurgent Japanese economy would help make Japan a fuller partner in the alliance, and, thereby, contribute to peace, stability, and liberty in the region. A more vibrant, freer Japanese economy is also good in its own right, given its importance to the global economy and close integration with the U.S.

The Three Arrows

What is the critical lesson from Japan’s experience over the past two decades, particularly the recent period since the Great Recession? It is that easy money and fiscal stimulus—the first two arrows in Prime Minister Abe’s current marquee economic recovery package—have not resuscitated the Japanese economy.

Here are the facts: The degree of quantitative easing (QE) in Japan, although started later than the Federal Reserve’s three rounds of QE, has been far more aggressive than in the U.S. From 2008 to the middle of 2014, assets on the Fed’s balance sheet grew from 8 percent of GDP to 25 percent of GDP. The similar figure for the Bank of Japan (BoJ) over the same period is from 20 percent to 56 percent of GDP. (An extraordinary figure, dwarfing those of the European Central Bank and Bank of England.) In late October 2014, the BoJ announced plans to purchase government bonds at an annual rate of ¥80 trillion ($705 billion), 16 percent of GDP. This implies that the balance sheet of the BoJ would approach 80 percent of GDP within two years.

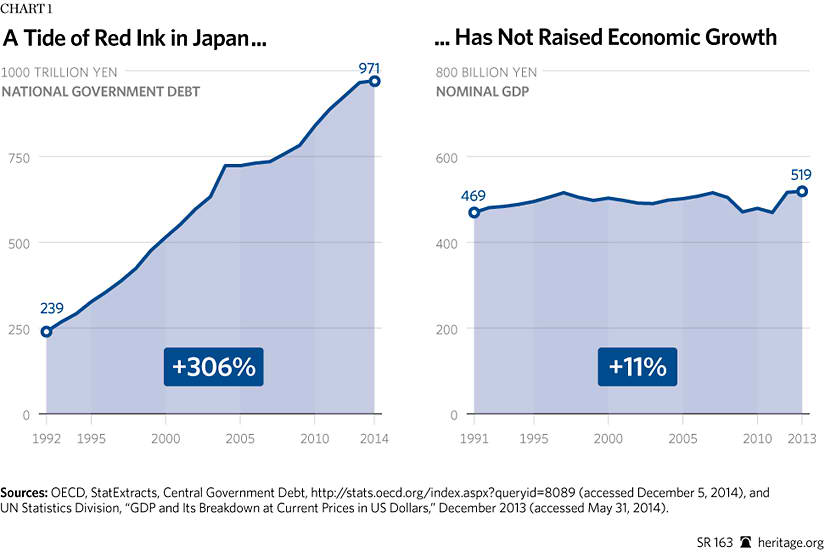

The same can be said of the fiscal stimulus. For the past five years, Japan’s budget deficit has been hovering around 10 percent of GDP (one of the highest in the world) while its national debt is more than 240 percent of GDP. As the national debt increased fivefold over the past two decades, the economy, measured in local currency, grew at an annualized pace of less than 0.5 percent. Since 1997, it has not grown at all. (See Chart 1.)

The third arrow of Prime Minister’s Abe’s reforms is tackling Japan’s “structural” long-term economic problems. Because of trends toward a shrinking population and labor force that will be next to impossible to reverse, given cultural norms in Japan and the fiscal headwinds that are highly likely over the long run, it is critical that Japan generate its growth through domestic investment and productivity gains. This is why focusing reform in the corporate sector is so vital to reviving long-term economic growth.

Necessary Policies to Revive Japan’s Economy

The priorities for the Abe administration should include the following:

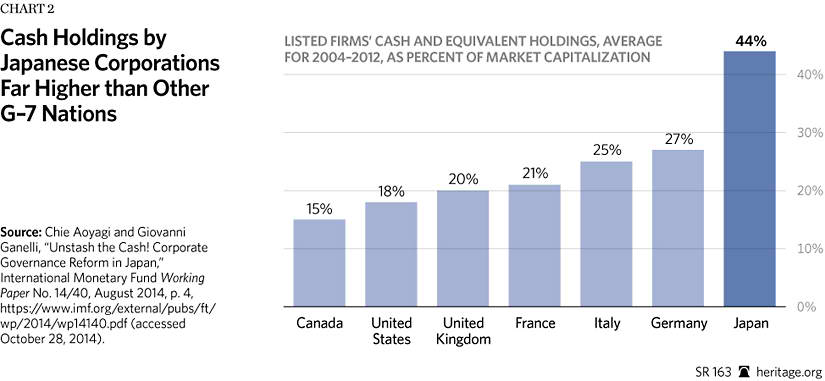

Policies that Shrink Corporate Cash Holdings. The chronic financial surplus of the corporate sector (the excess of earnings over investment) is arguably Japan’s most serious structural problem. According to the Ministry of Finance, cash holdings by Japanese corporations are at stratospheric levels compared to other Organization for Economic Co-operation and Development (OECD) countries. The average ratio of cash and cash equivalents as a share of total stock market capitalization of Japanese listed companies over the past decade exceeded 40 percent, compared to values in the 15 percent to 27 percent range in other G-7 countries.[1]

The trend to retain earnings is only becoming more prevalent. In 2001, Japanese-listed companies retained earnings of 33.5 percent of nominal GDP. Since then, this ratio has risen continuously, and hit 64.2 percent of nominal GDP in 2012.

It is widely believed that under Japan’s persistent deflationary environment, hoarding cash makes sense because it produced positive real rates of return. This belief is a fallacy. Returning cash to shareholders would have resulted in the same rates of return in addition to giving them alternative investment opportunities. According to Citibank, last year the buyback and dividend yield of companies listed on the Tokyo Stock Exchange was only 0.5 percent and 1.7 percent, respectively.

The extraordinarily high retention ratio is holding back corporate investments, which used to account for approximately one-third of GDP during the 1980s but have fallen to 20 percent since then. The high retention ratios are also partially responsible for the slow wage growth, which is still in negative territory after accounting for the recent rise in inflation. In Japan, wages fell by 3.5 percent between 1990 and 2012, while prices rose by 5.5 percent.

Japan’s bankruptcy laws are probably another reason why management has a preference for large cash holdings. Japanese managers are averse to filing for bankruptcy for a number of reasons. First is a lack of a structured legal reorganization procedure, such as exists in almost all developed countries. Second are the penalties associated with bankruptcies. Japanese executives potentially face severe civil and criminal penalties for filing bankruptcies, not to mention social ostracism.

To reduce the size of precautionary cash holdings, Japan should introduce prepackaged reorganizational plans similar to Chapter 11 in the United States. It should also reduce or eliminate the criminal penalties for bankruptcy filings.

Another serious issue with hoarding too much cash relates to the principal-agent problem, a common phenomenon in economics and political science. It occurs when a person (the “agent”) is able to make decisions against another person or entity (the “principal”) that is not in the latter’s interest. Retaining excessive earnings may increase the prestige and power of a company’s managers (the agents) at the financial expense of the shareholders (the principals). This is one of several reasons why stock prices often rise when companies announce a dividend increase.

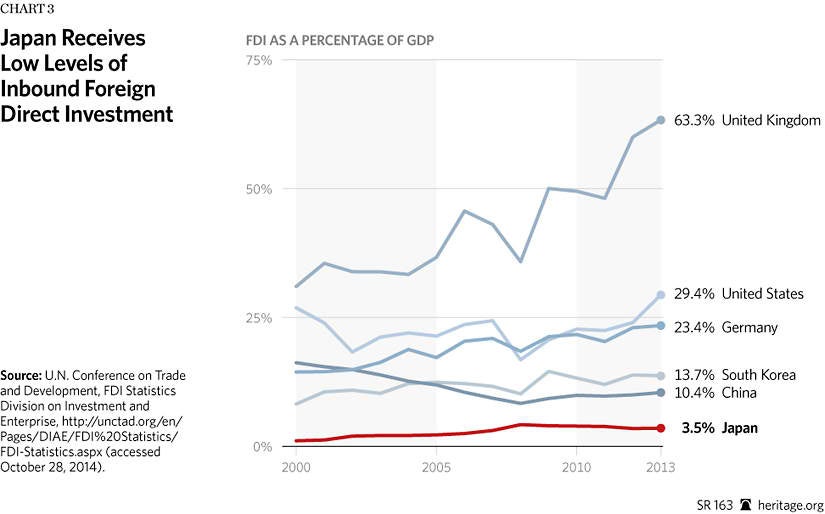

Reduced Barriers to Investment. The dearth of investment in Japan is best illustrated by the lack of inbound foreign direct investment (FDI). As shown in Chart 3, FDI into Japan is extraordinarily low compared to other countries. Japanese manufacturers are increasingly choosing to invest abroad. Within two years, Japanese automakers are projected to be producing more vehicles abroad than at home. This is a primary reason for Japan’s sluggish exports. While the yen has depreciated approximately 22 percent since the end of 2012, export volumes actually fell 1.5 percent in 2013 and have fallen 0.4 percent through August 2014.

While the average import tariff is low in Japan, non-tariff barriers have kept inbound investment at low levels. According to the Economist Intelligence Unit, foreign companies that want to enter the Japanese market are often forced to meet with domestic competitors in an attempt to prove that they will have no adverse effect on them. The non-tariff barrier goes by the euphemism of “demand-supply adjustment” in market-entry regulation. This regulation needs to be dismantled as part of Abe’s third arrow.

The lack of capital expenditures has significantly increased the age of Japan’s capital stock. Since 1990, the average age of service of its manufacturing equipment has risen by almost six years, while it has risen by just three to three and a half years in both the U.S. and Germany.

In the World Economic Forum’s 2014–2015 “Global Competitiveness Report,”[2] Japan, overall, ranks in a very respectable sixth place. But it is rated poorly on rules impacting investment. For example, it ranks 71st on “effects of taxation on incentives to invest,” and 58th on “business impact of rules on FDI.” In The Heritage Foundation’s 2014 Index of Economic Freedom, co-authored with The Wall Street Journal, Japan ranks 46th in investment freedom, one of the lowest among the OECD countries.

Improved Corporate Governance. Until mid-2014, Japan was one of the few countries in the world that did not have a corporate governance code. It is still the only developed country that does not have any rules about director training. Training is considered essential because many incoming directors have no boardroom experience. In many critical measures of corporate governance, Japan scores lower than other G-7 countries on the firm-level governance attributes of board composition, audit quality, shareholder rights, and ownership structure and compensation.[3] Improving corporate governance would go a long way toward unlocking Japan’s hoard of corporate savings.

Japan’s corporate board rooms are notorious for their insularity and lack of independent directors. Nearly all directors and CEOs are hired internally with longtime managers often accounting for 90 percent of board directors. In Japan, the proportion of independent outside directors of all directors in listed companies is only 9 percent—compared to 70 percent in the U.S., 50 percent in the U.K., and 30 percent in South Korea.[4] Research has shown that firms with a large number of independent directors typically possess smaller cash reserves, so raising the number of independent directors would be a healthy development. An amendment was passed in June 2014 which provides that any company without an outside director must explain to its shareholders why it is inappropriate to have one. According to the Ministry of Finance, as of June 2014, 74 percent of listed companies have at least one outside director, up from 62 percent in August 2013. While this has been a positive development, change has been slow to diversify the boardroom. Keidanren, a powerful business lobby, opposes making it mandatory to install independent directors.

Related to boardroom structure, the keiretsu system in Japan has long been associated with its once exceptional economic performance. Literally meaning “headless combine,” keiretsu is a form of corporate structure where a number of businesses are linked in various ways, mostly through small ownership shares in each other (crossholdings). It was once widely thought that this system enabled Japanese firms to take a longer view, to spend more money on research and development, and provide more job security.

Twenty years later, it seems that keiretsu’s economic value was overstated. Jeffrey Garten, Undersecretary of Commerce for International Trade in the Clinton Administration, believed that keiretsu restrained trade “because there is a very strong preference to do business only with someone in the family.”[5] Moreover, the keiretsu system made corporate takeovers very difficult in Japan, restraining competition and corporate consolidation. Japan’s proportion of mergers and acquisitions relative to GDP is about one-fourth to one-fifth of comparable levels in the United States and Britain. That is low in an economy that needs to be restructured.[6]

Not all looks bleak, however, for corporate governance in Japan. In 2014, the Tokyo Stock Exchange introduced a new index called JPX-Nikkei 400 that is composed of companies that offer better governance and higher returns. According to Nicholas Benes, head of the Tokyo-based Board of Director Training Institute of Japan, 2014 could be a “tipping point.”[7] The Japanese are now promising to adhere within a year to OECD corporate governance principles that spell out the rights and responsibilities of executives, boards of directors, and other stakeholders. Accountability for creating a new code was not given to the powerful Ministry of Economy, Trade and Industry (METI) but to the Financial Services Agency, which is responsible for protecting investors. Another important reform was the introduction of the Stewardship Code in February 2014 aimed at increasing fiduciary responsibilities of institutional investors. It has already been adopted by Japan’s largest asset managers and is expected to encourage investors to pressure managers to maximize shareholder value.

Reform of the Corporate Tax Structure. Although Japan has reformed its corporate income tax in recent years, it remains one of the highest in the OECD and throughout Asia. The marginal effective corporate tax rate measures the tax burden imposed on the marginal investment. High marginal taxes discourage investment because they often do not cover the cost of capital. Moreover, depreciation schedules (to write off the investment as an expense) are also less generous than in most countries. In the current “Global Competitiveness Report,” Japan is ranked a dismal 114th on “total tax rate as a percentage of profits.”

Compounding this problem, Japan allows deductibility of interest payments but not equity payments (dividends and share buyouts), which further distorts corporate financial decisions because it causes corporations to favor debt over equity financing. This distortion is illustrated by the difference in the cost of capital for equity versus debt. For Japan, this difference is the highest among the G-7 countries.

Given the high corporate taxes and cash levels, it is no surprise that the return on equity in Japan has consistently lagged behind those of Europe and the United States. According to the well-known Japanese brokerage firm Nomura Securities, Japanese companies earn just $9.50 a year for every $100 of shareholder equity, compared with $17.70 at U.S. companies and $11.80 at Asian companies outside Japan. The dismal performance of “Japan, Inc.” over the past 20 years, however, is beginning to change corporate Japan in some positive ways. For example, according to The Economist, foreigners now own 30 percent of the stock market, up from 4 percent in 1989. Shareholder capitalism as opposed to stakeholder capitalism is taking root, which means there should be a much greater focus on maximizing shareholder value as opposed to placating stakeholder groups, such as labor unions, environmentalists, and even suppliers. Foreign shareholders are more likely to want to change the lifetime employment guarantee that favors seniority over merit. In the “Global Competitiveness Report,” Japan places 133rd in “hiring and firing practices.”

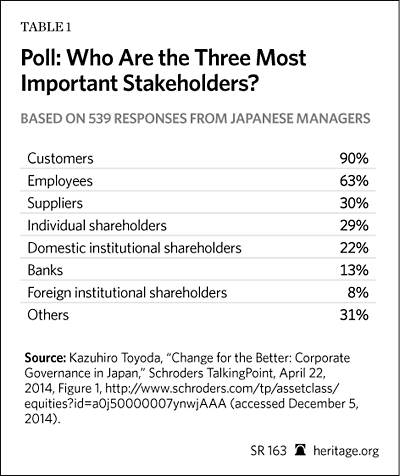

The movement toward making the shareholder the priority in Japan has a long way to go. According to a survey of over 500 Japanese senior managers, shareholders remain low on the totem pole, with customers and employees ranked as more important stakeholders.

Bold Special Economic Zones. The centerpiece of Abe’s structural reforms are the six special economic zones announced in 2014. The zones are to be granted special powers to deregulate everything from health care to agriculture, and allow companies to lay off workers, something which is now very difficult. Because the proposals are considered too radical to be approved now, the idea is to show their efficacy in boosting growth within the zones before adopting the reforms for the entire country.

If this experiment is to be successful, Abe and policymakers will have to be bold. Interestingly, Japan is already littered with roughly 1,000 special economic zones, many of them started by the government of Prime Minister Koizumi during the 1990s. Unfortunately most of the zones were considered a failure because central government bureaucrats crushed many of the deregulation proposals for fear of offending business interests.[8]

Abe’s proposed economic zones are much larger in scale, covering an area encompassing nearly two-fifths of Japan’s GDP. This scale, of course, could make the reforms within the zones even harder to pass. This is, in fact, already occurring. According to The Economist, bureaucrats have been already watering down some of the proposals. For example, foreign doctors will only be allowed to treat foreign patients, not Japanese, as first planned. There are no measures on critical issues such as immigration or immediately lowering the corporate income tax. Even bureaucrats in Tokyo are balking, trying to make the new labor practices apply only to foreign firms.[9] It may be too early to tell the fate awaiting the special economic zones, but it appears that special interests still have the upper hand.

Conclusion

There are obviously other important structural reforms not mentioned in this Special Report, such as fiscal consolidation. With the national debt running at 250 percent of GDP, medium-term and long-term fiscal consolidation is a necessity. But without a significant lift in economic growth, cutting the debt ratio will be impossible.

That said, for the first time in 20 years, there seems to be a collective consensus that Japan is long overdue for a structural overhaul. Japan still has many advantages. Under the “Global Competitiveness Report” pillar of competitiveness “Business Sophistication,” Japan ranks first in the world. Within the sub-categories, it ranks first in the world in “local supplier quality,” “nature of competitive advantage,” “value chain breadth,” and “control of international distribution,” and second in “production process sophistication.”

The rise of China—a critical challenge for the U.S.–Japan alliance—is also creating greater urgency for domestic reform. China surpassed Japan as the world’s second-largest economy in 2010, and it is quickly building a deepwater fleet to challenge Japan and its allies in the Pacific.

There are precedents for quick and effective reforms in Japan. During the Meiji dynasty toward the end of the 19th century, a group of young reform-minded officials opened up the economy and eliminated feudalism, leading to a period of rapid industrialization. The country was transformed in just a decade.[10] As daunting a task as economic restructuring is today, it pales in comparison to that epic achievement. With the right priorities, Japan can meet the challenge. The U.S. needs it to do so.

—William T. Wilson is a senior research fellow in the Asian Studies Center, of the Kathryn and Shelby Cullom Davis Institute for National Security and Foreign Policy, at The Heritage Foundation.