There are literally no comparisons to current rates. That is, [the Department of Health and Human Services] has chosen to dodge the question of whose rates are going up, and how much. Instead they try to distract with a comparison to a hypothetical number that has nothing to do with the actual experience of real people.

—Douglas Holtz-Eakin

President, American Action Forum[1]

Enrollment in Obamacare’s health insurance exchanges has proven to be a somewhat difficult process amidst technical glitches and delays. Aside from the issues associated with actually purchasing health care, once an individual gets a quote for health insurance on an exchange, is the premium higher or lower than before?

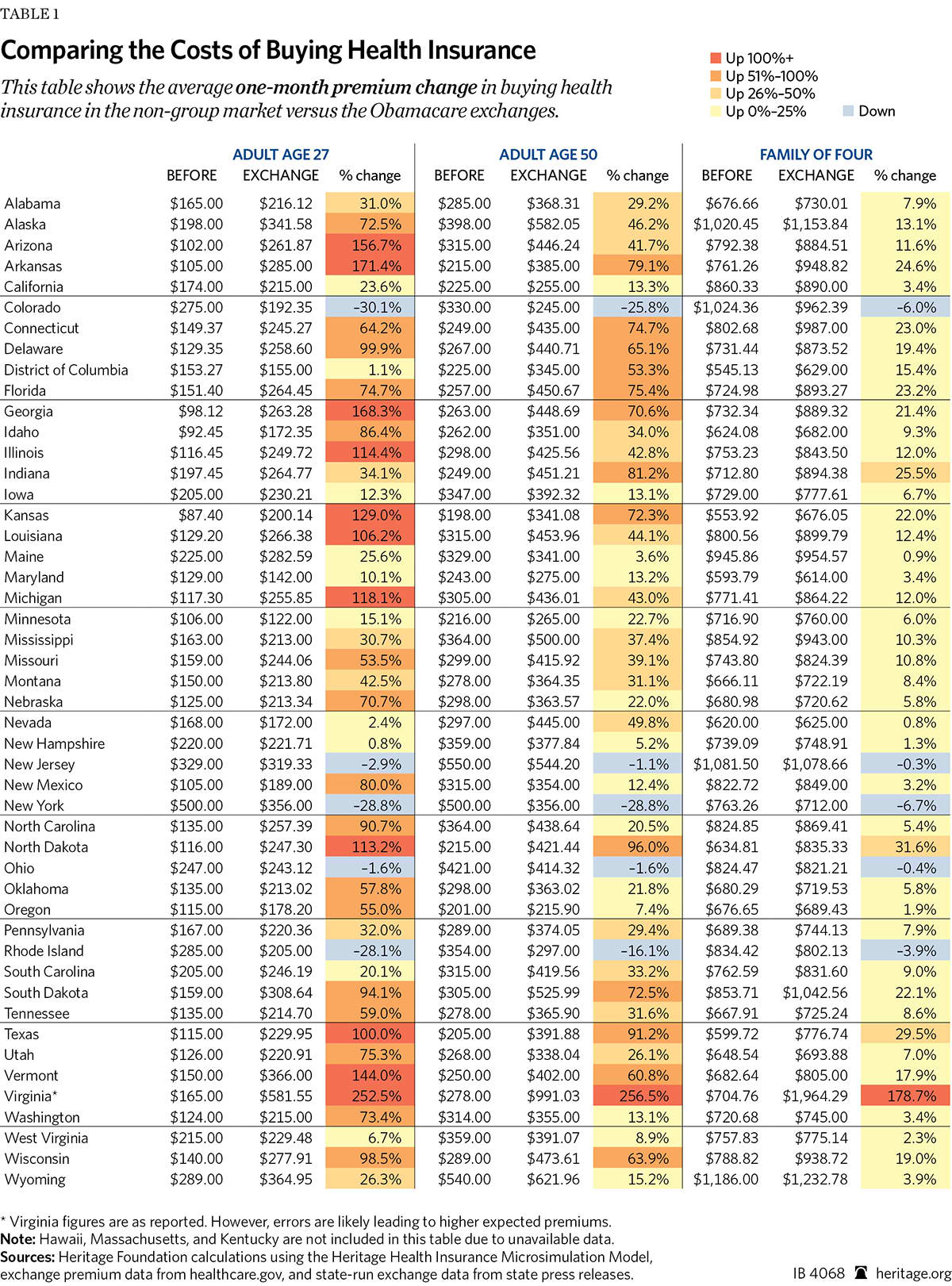

Our research finds that for many states, the insurance on health exchanges will cost more than existing insurance. This study illustrates that the general experience for individuals shopping on the exchange is that of increasing premiums from what was available to them prior to implementation of the exchanges. Many families and individuals will face this reality as they apply for coverage, and the implications of experiencing sticker shock are important to consider if enough people choose not to sign up for coverage for various reasons.

Methodology

The Heritage Health Insurance Microsimulation Model (HHIMM), in concordance with insurer data compiled by Mark Farrah Associates, is used to create a snapshot of what it looks like to shop for insurance prior to exchange implementation. This data is used to build weighted average premiums within the rating areas, similar to the process described in the most recent release from the Department of Health and Human Services (HHS).[2]

First, we use expected age distribution in the individual market from the HHIMM. Next, we use census data for the county populations in order to scale up to the state level, creating something that is roughly comparable to the weighted averages presented by HHS.[3] This comparison is different from others in that, rather than comparing specific plans, it is designed to capture the difference in premium levels between the exchange and what could be acquired in the market.

This paper is meant to provide a necessary segue to HHS’s data summary, creating an apples-to-apples comparison of exchange data to what the costs are for individuals. Effectively, we have used the same methods that were employed to provide summary data on the exchange markets to prior insurance data in order to get the closest comparison.

Some state-based exchanges have data releases that are more limited than the 36 federal exchanges. For state exchanges, some premiums must be estimated. As is the case with all studies built to address the changes in exchange premiums, it is important to note that when more data becomes available, results could vary slightly.

This study considers the data as released by HHS. States with little data released are omitted from this study.[4]

This analysis represents the change in unsubsidized rate levels. The purpose of this research is to provide further details on the changing premium levels across the country. With this in mind, it is true that many people will have the opportunity to lower their personal monthly costs within the exchanges if they qualify for subsidies.

Results

Individuals in most states will end up spending more on the exchanges. It is true that in some states, the experience could be the opposite. This is because those states had already over-regulated insurance markets that led to sharply higher premiums through adverse selection, as is the case of New York. Many states, however, double or nearly triple premiums for young adults. Arizona, Arkansas, Georgia, Kansas, and Vermont see some of the largest increases in premiums.[5]

The Obama Administration is desperate for younger people to enroll to prevent an adverse selection death spiral. As pointed out by Sam Cappellanti at the American Action Forum, “The enrollment of these low cost young adults…is essential as they are required to subsidize the costs of insuring the elderly and chronically ill.”[6] However, young adults face a penalty for not enrolling that is projected to be far less than the insurance coverage they could receive.

Our findings confirm that younger populations see larger percentage increases in premiums. A state that exhibits this clearly is Vermont, where the increase for 27-year-olds is 144 percent and the increase for 50-year-olds is still 60 percent, but far less. All states exhibit this relationship.

Many individuals will experience sticker shock when shopping on the exchanges. It is clear that many policies and cross-subsidization within Obamacare will lead to upward shifts in premiums. These policies include the health insurance tax, essential health benefit and actuarial value regulations, less allowed age variability in premiums, community rating, and guaranteed issue.[7] However, real uncertainty, amidst a rocky start, surrounds what enrollment will look like in the exchanges.

Fantasy Savings

Obamacare will leave many people paying more for their health insurance. The healthcare.gov website is learning to crawl, with additional data trickling in. However, based on information already released by HHS, states, and insurance plans, the claims of savings on premiums for the average participant is a fantasy.

—Drew Gonshorowski is a Policy Analyst in the Center for Data Analysis at The Heritage Foundation.

-------------------------

[1]Quoted in Avik Roy, “Double Down: Obamacare Will Increase Avg Individual Market Insurance Premiums by 99 Percent for Men, 62 Percent for Women,” Forbes, September 25, 2013, http://www.forbes.com/sites/theapothecary/2013/09/25/double-down-obamacare-will-increase-avg-individual-market-insurance-premiums-by-99-for-men-62-for-women/ (accessed October 11, 2013).

[2]U.S. Department of Health and Human Services, “Health Insurance Marketplace Premiums for 2014,” September 2013, http://aspe.hhs.gov/health/reports/2013/MarketplacePremiums/ib_marketplace_premiums.cfm (accessed October 10, 2013).

[3]HHS’s main exchange dataset can be found here: https://www.healthcare.gov/health-plan-information/ (accessed October 10, 2013).

[4]Massachusetts and Hawaii are omitted. Minnesota, Kentucky, and Maryland have issued small releases.

[5]Virginia’s data likely has data entry errors. Omitting the entries that are likely incorrect suggests that Virginia’s likely premium increases are 115 percent for 27-year-olds, 65 percent for 50-year-olds, and 30 percent for a family of four.

[6]Sam Cappellanti, “Premium Increases for ‘Young Invincibles’ Under the ACA and the Impending Premium Spiral,” American Action Forum, October 2, 2013, http://americanactionforum.org/research/premium-increases-for-young-invincibles-under-the-aca-and-the-impending (accessed October 10, 2013).

[7]Ibid.