Abstract: Congress will soon vote on massive health care legislation--and on the amount of power the federal government will have over the entire U.S. health care sector. Many economists, politicians, and American citizens want to know: How many people could lose their current health insurance and end up on the so-called public option, a new government-run health plan? The numbers being tossed around are as dizzying as the array of health care bills. How to make sense of it? Heritage Foundation health policy expert Greg D'Angelo details five estimates--and what they mean for millions of Americans.

Congressional leaders are finalizing the details of the massive House and Senate health care bills. Congress will soon vote on health care legislation--and will decide whether to greatly expand the power of the federal government.

The House and Senate leaders have been busily cutting and pasting the complex provisions of the various bills into two pieces of legislation. While all five congressional committees with jurisdiction over health care have drafted their plans and passed bills out of committee, many unresolved policy issues still need to be addressed in the merger of these giant pieces of legislation. Chief among those unresolved issues is whether reform legislation will include the so-called public option--a new government-run health plan to "compete" with private health plans. Conservatives and moderates are unwilling to vote for a reform bill that includes the public option, yet many congressional liberals declare that they will not support legislation without a "robust" version of it.

House and Senate Versions. One of the two Senate bills includes a public plan and, strictly speaking, the other does not: The Senate Health, Education, Labor and Pensions Committee legislationincludes a public plan, while the Senate Finance Committee would instead create a health care cooperative. But Senate Majority Leader Harry Reid wants to include a public option and is reportedly considering a variety of alternative designs, including a state opt-out provision.

All three versions of the House bill included some form of public option. Speaker Nancy Pelosi has just unveiled the merged bill in the House, the Affordable Health Care for America Act (H.R. 3962), which includes a provision for a new public plan.[1] The original version of the House health care bill drafted by the House tri-committee--the American Affordable Health Choices Act of 2009 (H.R. 3200)[2]--would have created a new public plan modeled on Medicare to "compete" with private health plans in a health insurance exchange. Consistent with the original tri-committee proposal, the Ways and Means Committee and Education and Labor Committee versions of the House legislation included a "robust" public plan that would pay providers Medicare-based rates. The version amended by the Energy and Commerce Committee instead contained a public plan that would have to negotiate provider payment levels.[3] While the final House product, H.R. 3962, includes a somewhat less "robust" public option than the original tri-committee bill (because the public plan would begin by paying private or negotiated rates), it is still useful to look at all the estimates. If the history of Medicare--a program initially designed to pay private rates to providers but now governed by a complex formula for administered pricing--is any guide, then even a less "robust" public option is likely to become more "robust" in the future.

The "Public Option": A Major Sticking Point

The proposal to create a new public plan has become a major sticking point in the health reform debate, so it should be no surprise that controversy has surrounded estimates of public-option-enrollment and the resulting impact on private coverage, including the employer-sponsored health insurance that millions of Americans currently have today.[4]

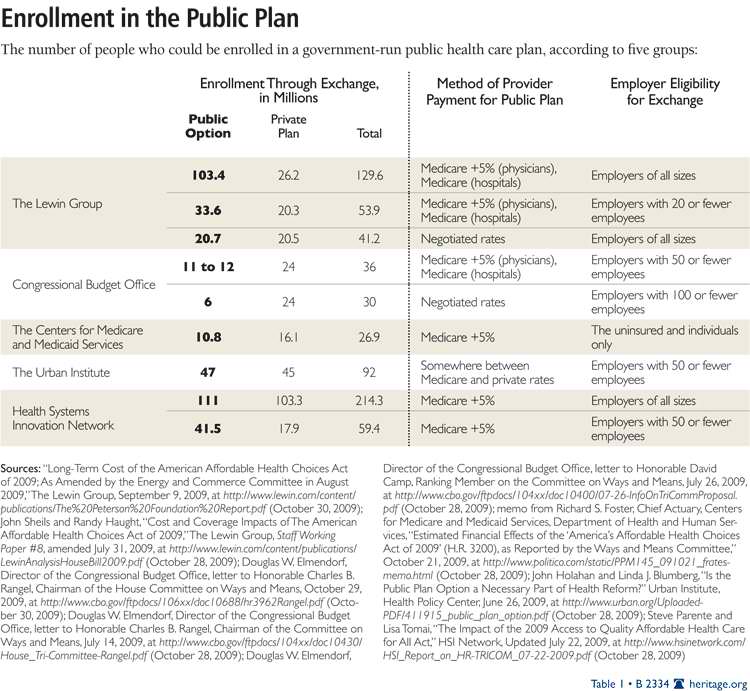

Five different organizations and offices have made predictions of how many Americans could end up enrolled in the public option. The Lewin Group, the Congressional Budget Office, the Centers for Medicare and Medicaid Services, the Urban Institute, and Health Systems Innovations Network all examined the impact of the original House tri-committee bill, or a similar proposal, using a public plan modeled on Medicare. All five entities attempted to predict the impact of a new public plan, at the time operating under slightly different assumptions and methodologies.

Given these differences, it is important for lawmakers and their constituents to take a closer look at the estimates. This is not necessarily because the various predictions are right or wrong, but to grasp the context of the different numbers cited in the debate. While there are different estimates, by every prediction, millions of Americans could lose their current insurance and end up enrolled in the new public option.

Predicting Public-Plan Enrollment. When estimating the impact of health reform proposals there is always some degree of uncertainty about how different individuals will respond to changes in policy. Scholars from the Urban Institute suggest, "any enrollment prediction will require significant assumptions about individual behavior, and the resulting estimates will be subject to more than typical levels of uncertainty."[5] Therefore, in the presence of great uncertainty--and the absence of a consensus--the best approach is to review existing studies and compare the different estimates.

Key Factors in Estimates. The two most significant factors that would determine the enrollment in, and thus the impact of, a new public plan are the size of companies that are eligible to join the health exchange and buy into the public plan, and the cost of premiums in the public plan compared to premiums for private insurance.

- Size of employers eligible to join the exchange and buy into the public plan. Under section 202 of the proposed House tri-committee legislation, in year one (2013), individuals and employers with 10 employees or fewer are eligible for the exchange. In year two (2014), individuals and employers with 20 employees or fewer become eligible. In year three (2015), the "Health Choices Commissioner"--a presidential appointee tasked with heading a new executive-branch agency called the Health Choices Administration--is granted the authority to expand employer eligibility with the "goal of allowing all employers access to the Exchange."[6] The commissioner can phase in eligibility "based on the number of full-time employees" and "such other considerations as the Commissioner deems appropriate." But clearly, different assumptions about how, or when, the commissioner might act could significantly alter estimates of enrollment in the public plan. When discretion is left to public officials, it is often difficult to know exactly how they might exercise their power. In this case, it is even more difficult to predict what the commissioner--an unknown official overseeing an entirely new agency--would do.

- Premiums in the public plan compared to private insurance premiums. The relationship between premiums for the public plan and premiums for private health plans will also influence enrollment in the new public option. A number of considerations would affect premiums for the public plan, but the most important determinant would be the provider-payment levels under the plan.[7] According to section 223 of the tri-committee legislation, the public plan would pay providers using Medicare-based rates--which today are much lower than private payment rates-- with a 5 percent increase in reimbursement for physicians that accept both Medicare beneficiaries and patients covered by the public plan. However, even with payment rates at Medicare plus 5 percent, reimbursement under the public plan would still be considerably lower than private payment levels--with physician reimbursement at only 86 percent of private rates. The public plan would only pay hospitals Medicare rates, which are 68 percent of private rates. Mainly as a consequence of these low provider-payment levels, it is likely that premiums in the public plan would, to some extent, be lower than private insurance premiums. The ability of the public plan to offer lower premiums by imposing below-market reimbursement rates on providers would enable it to undercut private health plans, increasing enrollment in the public option.

Five Entities, Five Estimates

The Lewin Group.[8] The Lewin Group--an independent health care analysis firm--was the first to estimate the impact of creating a new public plan, modeled on Medicare, in its analysis of the Health Care for America proposal[9] developed for the Economic Policy Institute, a liberal Washington-based think tank, by Jacob S. Hacker, professor of political science at the University of California at Berkeley and chief architect of the public option.[10] Lewin also produced a series of analyses examining variations of the proposed public option under President Obama's health care plan during the campaign.[11] More recently, in the context of the current debate, Lewin analysts examined the actual text of the House tri-committee bill in order to predict the impact of the public plan included in the draft legislation.

In its analysis of the House tri-committee legislation (similar to the versions amended by the Ways and Means and Education and Labor Committees), Lewin used the provider-payment rates for the public plan specified in the bill. Under the Ways and Means and the Education and Labor Committee versions, the public plan would use Medicare plus 5 percent reimbursement rates for most physicians, and Medicare rates for hospitals. Using these payment rates, Lewin estimates that premiums in the public plan would be about 20 to 25 percent lower than premiums for private insurance.[12] Although less important than provider-payment levels under the public plan, Lewin's premium estimates also take into account other important factors, such as administrative costs, utilization review, risk selection, and increased cost-shifting onto private health plans.

With its estimated difference in premiums, Lewin analyzed the impact of the public plan under two different assumptions for exchange eligibility: (1) the commissioner allows all employers into the exchange and (2) the commissioner continues to restrict eligibility to employers with no more than 20 employees.

If fully implemented in year three (2015) and employers of all sizes were made eligible, Lewin estimates that 129.6 million people would obtain coverage through an exchange. Within the exchange, 103.4 million people, or 78 percent of exchange participants, would be covered by the public plan. Lewin estimates that 88.1 million Americans would lose their current employer-sponsored insurance and that there would be an 83.4 million net reduction in private coverage under this scenario.

If fully implemented in year three (2015), when only employers with a maximum of 20 workers are eligible, Lewin estimates that 53.8 million people would obtain coverage through an exchange. Within the exchange, 33.6 million people, or 62 percent of exchange participants, would be covered by the public plan. Lewin estimates that 21.9 million Americans would lose their current employer-sponsored insurance and that there would be a 34.9 million net reduction in private coverage under this alternative scenario.

When Lewin modeled the impact of the less "robust" public option included in the Energy and Commerce Committee version of the original House tri-committee bill--now similar to the merged House bill H.R.3962--it predicted that as many as 20.7 million people could still end up on the public option. Meanwhile 8.2 million people could lose their private employer-sponsored insurance.[13]

While the Lewin numbers have been the most cited figures by far, the Lewin analysts who conducted the studies have advised against relying on only a single source.[14]

The Congressional Budget Office. In its preliminary analysis of the draft House tri-committee legislation, the Congressional Budget Office (CBO), Congress's official scorekeeper,[15] predicted substantially lower enrollment in the public plan than did the Lewin Group, and thus a very different impact on existing private insurance. However, the CBO estimates did not represent a formal or complete score of the actualbill languagebut were based only on draft specifications and discussions with congressional staff.

In its two preliminary estimates, which relied on draft language, [16] the CBO predicts that approximately 36 million people would obtain coverage through the exchange. As opposed to deriving enrollment estimates for the new public option, the CBO simply assumed that one-third of exchange participants, 11 to 12 million people, would be enrolled in the public plan once it was fully implemented.[17] However, based on the CBO analyses, it is unclear what the exact impact on private coverage would be or precisely how many Americans would lose their current employer-sponsored insurance.[18]

Although the CBO used the same provider-payment rates for the public plan as Lewin, it expects the premium differential between the public plan and private insurance to be just 10 percent (compared to the 20 to 25 percent difference estimated by Lewin). This prediction was made using a comparison of costs between traditional fee-for-service Medicare and private health plans offered through the Medicare Advantage program. In response, the Lewin Group issued a report that questioned the conclusions drawn from such a comparison.[19] Lewin and CBO also appear to disagree over how private plans would respond to a new public plan entering the market.[20] Nevertheless, CBO suggests that even with an offer of lower premiums, some individuals would avoid enrolling in the public plan due to limited provider participation.[21]

Another difference between the CBO and Lewin estimates is whether the commissioner would open up the exchange and the public plan to employers with more than 20 workers in year three. In its early estimates, CBO and the congressional Joint Committee on Taxation (JCT) assumed that even though the commissioner is permitted to allow all firms to join the exchange, the commissioner would restrict access to employers with 50 or fewer employees.The CBO emphasized the difficulty in predicting how the commissioner might act in the face of conflicting pressures to fully open the exchange and potential resistance from providers and private health plans to expanding eligibility. The CBO also cited the potential for adverse selection if larger employers were allowed to enter the exchange.

In circumstances like these, where legislation does not provide sufficient guidance, the CBO usually relies on the intent of the legislation's drafters, which can be assessed in a number of ways, including speeches made by Members of Congress or documents prepared by committee staff. While this is probably how the CBO made its determination,[22] it is still not exactly clear why the CBO assumed only employers with 50 or fewer workers would be eligible for the exchange--and would exclude roughly 70 percent of those currently with private employer-sponsored insurance. This judgment call made by the CBO appears at odds with the drafters' intent to offer a "robust" public option with the "goal of allowing all employers access to the Exchange."

But, regardless of the underlying assumptions in the preliminary CBO scores, the legislation specifies that the commissioner would ultimately have the discretion to open up the exchange to employers of all sizes. Therefore, any forthcoming CBO estimates should at least consider the impact of the public option under a variety of alternative assumptions, including a scenario in which eligibility is extended to all employers. When the Lewin Group used the CBO assumption that the exchange would be opened only to individuals and employers with 50 or fewer workers, it estimated public-plan enrollment at 42.7 million people--four times the CBO number. When Lewin further assumed that premiums for the public plan would be just 10 percent less than comparable private coverage, it arrived at an estimate of public-plan enrollment of 22.1 million people--still a full 10 million more than the CBO prediction.

The CBO preliminarily estimated that under the merged House bill, H.R. 3962, about 30 million people would obtain coverage through the exchange with roughly one-fifth, or 6 million people, enrolled in the less "robust" public plan operating based on negotiated rates--15 million less than the Lewin Group predicts.[23] The lower CBO estimate of enrollment primarily reflects its assessment that the public plan as envisioned in the merged legislation would probably have higher, not lower, premiums than private plans.[24]

Notwithstanding the discrepancy over premium estimates, the CBO has not modeled a scenario in which all employers become eligible for the exchange, but it has previously indicated that while its estimates of employer-based enrollment in the public plan would indeed grow, the numbers would remain "substantially smaller than the Lewin Group's." The CBO contends that large employer group plans would likely have lower administrative costs than health plans in an exchange and thus would not elect to join the exchange and buy into the public plan. But, like Lewin, the CBO admits that with all the uncertain factors, "estimating enrollment in the public plan is especially difficult."

The Centers for Medicare and Medicaid Services. The Chief Actuary in the Centers for Medicare and Medicaid Services (CMS) in the Obama Administration's Department of Health and Human Services issued a memorandum on the potential impact of H.R. 3200 as reported by the Ways and Means Committee.[25] Unlike the CBO, the CMS based its estimates on the actual legislative text and considered the coverage impact of an exchange with a public option, which would "generally pay providers at Medicare payment rates plus 5 percent." The CMS estimated that the public plan would have costs about 18 percent below private plans, with premiums approximately 11 percent lower than private coverage--reflecting differences in provider-payment rates, utilization management, and selection effects. The actuaries modeled exchange and public plan enrollment as a function of expected health expenditures relative to the cost of available coverage. The CMS estimates that at full implementation, roughly 27 million people would obtain coverage through and exchange, with 10 to 11 million people (40 percent of participants) enrolled in the public option. The CMS assumed that 40 percent of exchange participants would be enrolled in the public option based on a review of "insurance selection studies and experience from other programs." The actuaries caution that "in practice, the percentage of public option enrollees is one of the most uncertain estimation factors" for the legislation.

The actuaries predict that approximately 12 million Americans would lose their current employer-sponsored insurance--contributing to a net reduction in private coverage of about the same size--as employers drop or change existing offers of coverage. However, in a clear departure from the legislation, the CMS appears to assume that only the uninsured and other individual purchasers of health insurance would have access to the exchange and the public option. Of the predicted 27 million people enrolled in the public plan, 13 million would have otherwise been uninsured and 14 million would have moved from individual private coverage to the public option. Consequently, if either small or large employers gained access to the exchange and could buy into the public option as the bill allows, it is likely that the actuaries' enrollment numbers would significantly increase. In fact, CMS actuaries warn that behavioral responses to changes are "impossible to predict with certainty" and that responses of individuals, employers, and others in the health sector "could differ significantly from the assumptions underlying the estimates presented" in part because the "legislation would result in numerous changes in the way that health care insurance is provided and paid for" with "few precedents" that exist. The estimates were thus "very uncertain" and "subject to a substantially greater degree of uncertainty than is usually the case."

The Urban Institute. Two Urban Institute scholars--John Holahan and Linda J. Blumberg-- also estimated the impact of a health reform proposal with a new public plan offered in a health insurance exchange. [26] Despite the "uncertainty about so many parameters," the Urban Institute assumed "a comprehensive reform framework consistent with those being discussed in Congress" to produce "ballpark" numbers.[27] The Urban Institute study was not based on proposed legislation, but it is similar to plans in Congress and happens to assume that only individuals and employers with no more than 50 workers would be eligible for a newly established exchange with a public plan. Holahan and Blumberg estimate that 92 million people would obtain coverage through the exchange, while 46.7 million people, or roughly 50 percent of those in an exchange, would be covered by the public plan. The Urban Institute enrollment estimate of 46.7 million people is close to the Lewin estimate of 42.7 million people under similar assumptions, when only employers with 50 or fewer workers are made eligible for the exchange. According to the Urban Institute study, under this scenario, 52 million Americans would lose their current employer-sponsored insurance and there would be a 16-million-person net reduction in private coverage.

These Urban Institute predictions by Holahan and Blumberg assume the public plan would set reimbursement rates somewhere between Medicare and private levels.[28]

In accounting for the difference in cost between public and private premiums, the Urban Institute, like the CBO, assumes a 10 percent difference between premiums for the public plan and comparable private coverage.[29] Because the CBO and Urban Institute make similar assumptions, it would be reasonable to expect their results to be similar. But the outcomes of the two studies vary significantly, with the Urban Institute--like the Lewin Group--estimating public-plan enrollment at least four times higher than the CBO and even CMS predictions.

Yet, unlike estimates made by Lewin, CBO, and CMS, in the Urban Institute study, the number of people who obtain coverage through the exchange does not depend on provider-payment rates and premiums. In the Urban Institute model, the availability of subsidies was a more important factor than payment rates and premiums in the public plan relative to the cost of private coverage. Therefore, the Urban Institute expects the likelihood of public plan enrollment to fall as income rises. While Holahan and Blumberg criticize earlier work by the Lewin Group--suggesting that Lewin overstates the importance of price, underestimates the likely response of private insurance to a public option, and thus exaggerates the impact on private coverage--under similar parameters, the Urban Institute study produced similar results.

Health Systems Innovations Network.[30] Steve Parente and Lisa Tomai of Health Systems Innovations Network (HSI), a health care economics consulting firm, also made predictions about enrollment in a new public plan under the original House tri-committee draft legislation. The Parente and Tomai study relied on a peer-reviewed simulation model that--like the Urban Institute model--was initially funded by the U.S. Department of Health and Human Services to estimate the impact of policy proposals.[31] Parente and Tomai used the Medicare-based reimbursement rates specified in the legislation as in the other studies, with the exception of the Urban Institute. Consistent with the CBO assumption for exchange eligibility, the authors of the HSI report assumed that at least initially the exchange, and thus the public plan, would be limited to individuals and employers with no more than 50 workers.

Parente and Tomai estimate that 59.4 million people would obtain coverage through an exchange, while about 41.4 million people, 68 percent of those in an exchange, would be covered by the public plan.While there would be a 33.2 million net reduction in private coverage, the most significant point of these findings is that the HSI enrollment estimate, when individuals and employers with fewer than 50 workers are made eligible for the exchange, are far more comparable to the estimates produced under similar assumptions by the Lewin Group and the Urban Institute than to the preliminary figures released by the CBO. The CBO numbers are actually more closely in line with the CMS estimates that appear to assume that employers are not able to buy into the public plan at all.

When Parente and Tomai adjust the underlying assumptions to allow large employers to purchase coverage for their workers through the exchange, participation in the exchange reaches 214.3 million with 91.6 million people, 42.7 percent, enrolled in the public plan, resulting in a 64.9 million net reduction in private coverage. Although neither the CBO nor the Urban Institute examined such a scenario for exchange eligibility, the HSI predictions seem in line with the oft-cited Lewin numbers for public plan enrollment, which are currently the only means of comparison.

Aside from exchange eligibility, similar to the model used by the other entities (excluding Urban), the HSI predictions for enrollment in a public plan are driven by the difference between its premiums and the premiums for private insurance. But, as the CBO, CMS, and Urban Institute contend, price is not the only factor in choosing a health plan. While the Lewin model addresses this common criticism in part by controlling for age and health status of individuals, the model used by Parente and Tomai--unlike the models used by CMS, CBO, and Urban Institute--is somewhat superior since it attempts to mitigate this concern by also taking into account the underlying preferences of individuals for certain types of health plans.

The Largest Unresolved Issue

Lawmakers are currently meeting behind closed doors to iron out the legislative specifics of a massive overhaul of the nation's health care system. But many critical issues must be resolved before Congress can vote on legislation. Perhaps the largest unresolved issue is whether reform will include a so-called public option and, if it does, what form it will take. Liberals are pushing harder than ever for the inclusion of a public option with the stated intent of making the new public plan available to all Americans.

Indeed, there has been controversy over the different predictions made about enrollment in the different forms of a public option and the resulting impact the plan could have on private coverage, including the employer-sponsored insurance that millions of Americans currently have today. While these competing estimates have been relied on throughout the course of the debate, few Members of Congress have done an objective review of existing studies.

But a closer look at all the available estimates shows less controversy than initially expected and, instead, an almost emerging consensus. If lawmakers were to create a public plan as envisioned by many congressional leaders, particularly liberal Democrats in the House, millions of Americans could lose their current employer-sponsored insurance, end up crowded out of private coverage, and find themselves enrolled in the new public "option."

Greg D'Angelo is a Policy Analyst in the Center for Health Policy Studies at The Heritage Foundation. Health policy interns Julius Chen and Kathryn Nix contributed to the research for this paper.

;){kind=link}