President Bill Clinton has sent health care legislation to Capitol Hill that is breathtaking in its scope. He strikes a responsive chord with most Americans when he condemns the current system as bureaucratic and wasteful, and when he urges a comprehensive reform of the $1 trillion health system-accounting for about one-seventh of the entire U.S. economy-based on the principles of security, simplicity, savings, choice, quality, and personal responsibility.

But although Clinton has stressed the need for simplicity and freedom from bureaucracy, his legislation offers anything but that. The Administration followed a 239-page draft, leaked by Members of Congress in September 1993, with a 1,342-page bill, the "Health Security Act." Emerging from the complex language of this huge bill is a massive top-down, bureaucratic command-and-control system that would meticulously govern virtually every aspect of the delivery and the financing of health care services for the American people. As The Economist of London observes, "Not since Franklin Roosevelt's War Production Board has it been suggested that so large a part of the American economy should suddenly be brought under government control . 1

Every aspect of the health care system would be affected by the legislation. Hundreds of pages of tightly written paragraphs detail sweeping government control of the health insurance industry: precise benefits that must be assured; insurance requirements for firms; a "national quality management program" to oversee the quality of health care services; medical education, and the training of physicians; the creation of model information systems; new public health initiatives; the establishment of new federal loans and guaranty and solvency funds; new assessments and taxes; rural health programs; a new long-term care program; malpractice reform; antitrust reform; new penalties to combat fraud and abuse; major changes in the Medicare program, including a prescription drug benefit and coverage of state and local government workers; billions of dollars in tax subsidies; new panels, advisory boards, and commissions; coordination of worker's compensation and auto insurance with the new standard benefits package; and dozens of other fundamental changes. The American people can be forgiven for feeling overwhelmed by the enormity and complexity of this reform-a reform which officials claim will certainly work and save money because every aspect has been thought through by experts.

Americans are concerned about how the Clinton Plan will affect not only their health care, but also their pocketbooks. When Donna Shalala, the Secretary of the Department of Health and Human Services, said on October 28 that under the Clinton Plan 40 percent of all Americans with insurance would be paying more for their health care premiums, Members of Congress and many other Americans expressed alarm.2 And many ordinary Americans no doubt will be shocked to learn that Members of Congress, Administration officials, and other federal workers will not join the system, if at all, until after the rest of the country is under the program. As congressional hearings continue, more details will be revealed and fully explored, enabling Americans to get a better picture of the dramatically different health care system that awaits them under the Clinton Plan.

As Americans attempt to determine how this package would affect them, they need to examine the details. But they also need to be keenly aware that lodged deep in the body of the draft are five key mechanisms that would greatly broaden and deepen government control over the financing and delivery of medical services in the American health care system:

A National Health Board

The Clinton Plan creates a new, presidentially appointed agency that will have general oversight over the American health care system, ranging from the pricing of health insurance premiums, to the approval of new benefits to be included in any "government standardized health care" plan, and to the enforcement of public and private spending limitations at the national and state level. Unless there is congressional action to intervene, no change in benefits, medical treatments, or price can occur without the prior approval of this federal agency.

Regional Health alliances

The Plan creates a new state-based system of health insurance cooperatives that will control the availability of health plans, enforce health budgets, enroll employers and employees in the new system, collect premiums, and generally enforce the national insurance rules and regulations. Every American will be required to obtain health insurance through these health alliances, or through similar corporate-sponsored plans if they work for a large firm.

A Standard Benefits Package

The Plan outlines in meticulous detail what medical services are to be included in a standardized government health benefits package. These benefits must be offered by all approved health insurance plans. The mandatory benefits package includes not only major medical services but also routine ear and eye examinations and even elective abortion and expensive treatments for alcohol and drug abuse. This standardized benefit package will be free of tax to Americans. But if a family requires or wants any other benefits, these must be paid for with the family's own after-tax dollars.

Employer Mandates

The Clinton Plan requires all employers to provide at least the standard package and to pay at least 80 percent of the cost of the government's standard health benefits package. But the Plan also will subsidize companies in regional alliances (but not self-insured companies) so that their premium costs are limited to 3.5 percent of payroll for small firms and up to 7.9 percent of payroll for large companies. Firms with over 5,000 employees still have to provide at least the standard package, but may opt out of the regular health alliance system and form their own regulated cooperatives.

Government Budgets and Spending Caps

While the President says he does not favor price controls, his plan bristles with them. In fact, the central cost control in the Clinton Plan is not competition, nor even "managed competition," but a rigid system of spending caps on public and private health insurance spending, plus fee controls for doctors in feefor-service plans. Powerful standby price controls also are contained in the Plan. States are permitted, even encouraged, to run every element of health care through state monopolies known as "single payer" systems. Under the Plan, the growth in health care spending is to be forcibly racheted down, year by year, until it is in line with the growth of inflation, as measured by the Consumer Price Index (CPI), by 1999.

With these central features in place, there can be little doubt that Americans will experience profound changes in the way they receive medical care, and what care they will receive. Among these changes:

1) Government controls will be expensive and will expand.

Despite all the talk of removing red tape and bureaucracy, personal choice and responsibility are tightly restricted in the Plan by boards and alliances, commissions and panels. Government regulation rather than market competition is the chief instrument to contain costs and deliver medical services. A standardized health benefit package replaces choice of benefits and the government will aggressively promote managed care, thereby practically limiting personal choice of doctors, and making it even more difficult for Americans to take advantage of new or specialized medical services. Moreover, the regional health alliances seem destined in the first instance to pave the way for giant, geographically based health insurance cartels. Most likely, public criticism of this will be so great that the unpopular insurance middle-men will in the future be swept away. The result? Health care eventually will be managed directly by state-run boards or alliances.

2) There will be less freedom for doctors and patients.

The President says that America's doctors will have more freedom to practice medicine and patients will have freedom to choose their doctors. But the ability of every doctor to treat patients according to his or her independent professional opinion will be sharply limited. For example, the National Health Board will set national guidelines for determining what treatments can be provided or upgraded in a standard government health insurance package, which treatments are or are not "medically necessary," and even how often approved treatments or tests can be conducted. Regional alliances and their approved networks and plans will instruct doctors on what costs they can incur and will enforce official practice guidelines. And if doctors are in a fee-for-service plan, it will be fee-for service in name only: state governments and the alliances can tell them what fees to charge.

Theoretically, patients will have choice of doctor. And the Clinton Administration has included a "point of service" option in the proposed system, enabling Americans to pick doctors outside of their health plans. But, as managed care drives out all but one fee-for-service alternative, something the Administration encourages, more and more Americans will be forced into plans that deny them an easy choice of doctor and control access to any specialist. Private practice will decline, and is likely to become the last resort of the wealthy. To be sure, anyone will have the right to consult any doctor outside the system if they pay for the visit and treatment out of their own pocket. But just as any American is free to send their child to Harvard University or Sidwell Friends School, in reality this choice will be the privilege only of the rich and powerful.

Moreover. if the Clinton Administration is serious about giving all Americans coverage at least as good as that offered by Fortune 500 companies, and yet also serious about driving down the rate of growth of medical spending, then at some point the federal government, either directly or indirectly, must ration medical services. This means that the government must either explicitly limit medical services or subtly reduce the availability of such services. Unlike the Oregon health reform initiative, which lists and ranks 709 different medical procedures, and will deny access to one that falls "below-the-line" determined by a budget limit,3 the Clinton Plan is silent on this unpleasant prospect. But with federal government spending caps, explicit denial of services must occur.

3) taxes will grow sharply or care will be cut.

Nobody really knows what the Clinton reforms will cost-not even the Administration. After the Clinton Administration's September 7 draft plan reached Capitol Hill, Representative Henry Waxman, the California Democrat who is chairman of the House Subcommittee on Health and the Environment, was openly skeptical of the proposed caps on Medicare and Medicaid. Focusing on the same topic, Senator Daniel Patrick Moynihan, the New York Democrat who is Chairman of the powerful Senate Finance Committee, labelled the White House financing proposals "a fantasy."

Congressman Waxman and Senator Moynihan were not alone. Describing the initial financing projections of the Clinton Plan as "outrageously dishonest," the London Economist observed, "Mr. Clinton would have Congress believe that his proposals will provide universal coverage, subsidies for small employers, generous new commitments to cover prescription drugs, longterm nursing and mental health care plus a big chunk of deficit reduction with virtually no new taxes (bar a small rise in cigarette duties)--and all by 1997."4 Likewise, Representative Jim Cooper, the Tennessee Democrat who is the leading congressional champion of the "managed competition" health care reform model, said, "I don't know anybody who thinks it's fully funded."5

Since its first set of numbers was greeted with widespread skepticism, the Clinton team has gone back to the drawing board to "scrub and rescrub" the numbers. Given the Administration's initial presentation, it is not surprising that few experts, and just as few ordinary Americans, actually believe the Administration's numbers.

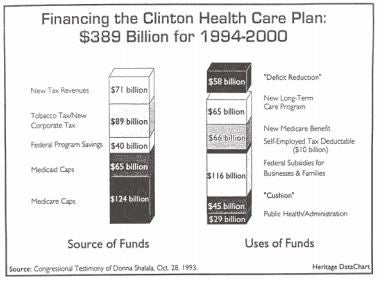

The Administration currently projects its plan to cost $331 billion from 1994 through 2000, including new spending for tax subsidies to businesses and low-income families, a new Medicare drug benefit, new long-term care services, and new public health initiatives.6 The White House also claims that it will achieve "savings" through new cost controls and greater efficiency. Increased "sin" taxes, in the form of a new levy of 75 cents on a pack of cigarettes, also are to be imposed. And the Administration still assumes it can cut both the rate of growth of Medicare spending by S124 billion and the growth of Medicaid spending by S65 billion over the next few years (including Medicare cuts already legislated in this year's budget package) without reducing the quality or availability of medical services to the poor and the elderly.

Among others, David Shulman, an economist with Solomon Brothers, Inc. of New York, does not expect the Clinton reform proposal to achieve its fiscal constraints: "Make no mistake about it. President Clinton is proposing an entitlement program, and if its substance survives, it will inevitably expand in budget and regulatory control.',7 Of course, if the Administration miscalculates on the cost of its huge reform program, or fails to cut "waste," or its latest financing efforts fail to achieve the promised savings in the system, its only resort is to cut care.8 The alternative is a huge tax increase.

Instead of relying on central planning, price controls, and top-down bureaucratic management to reform the health care system, Congress should adopt a comprehensive reform based on a consumer choice approach, such as The Heritage Foundation's Consumer Choice Health Plan or legislation in Congress based on similar principles.9

Under the Heritage proposal, the health coverage available to Americans, and the tax breaks for coverage, no longer would depend on their place of work. This would make insurance fully portable. Consumer choice, not bureaucracy, would serve as a mechanism for cost control the same way it does in the rest of the economy, where consumers seek the best value for their money. This would be done by ending the multi-billion dollar federal tax relief now available only for employer-based health benefits and using that money to give all American families refundable federal tax credits.

The tax credits would be provided directly to families through the withholding system or through a federal voucher for the poor. While every American family would get basic tax relief for health care, the generosity of tax relief for a family would depend upon its health care costs compared with family income. Thus, every American family would get a federal tax credit to purchase a basic health insurance package, including catastrophic coverage, to offset the costs of out-of-pocket expenses or to deposit funds into a tax-free "medical savings account"--a "medical IRA"--from which families could pay routine medical expenses. Families could allow the account to grow year after year for later use for retirement health care needs, for the purchase of long-term care insurance, or to roll over into an IRA or other pension plan.

By giving every American the same tax advantages, irrespective of place of employment. and empowering them with tax credits to purchase insurance, a consumer choice approach would enable all Americans to seek the best value for their money when buying insurance and medical care. If companies wanted to continue to provide health insurance, or contribute to a medical savings account they could still deduct the cost of doing so. But with equal tax treatment for all consumers for the purchase of all kinds of health insurance options, company plans would compete with other types of health plans, from union plans to church and trade association sponsored plans to various kinds of physician group, health promotion, and managed care programs. This would give all Americans the same kind of broad personal choice-now enjoyed by the President, White House staff, Members of Congress, federal workers and retirees, and their spouses and dependents. In the Senate, Republicans Don Nickles of Oklahoma and Orrin Hatch of Utah, among others, are drafting legislation to include these positive tax and insurance reforms. In the House, the chief proponent of such health care reforms is Representative Cliff Steams, the Florida Republican. These approaches would, in effect, open up to the American people an improved version of the consumer choice program now enjoyed by Members of Congress, Clinton Administration officials, and other federal workers, the program known as the Federal Employee Health Benefits Program (FEHBP). Under the Clinton bill, the FEHBP would remain for federal workers, at least until all other Americans were under the new Clinton program. The Nickles-Steams approach, by contrast, would correct the weaknesses of the American health care system by using consumer choice to attack the soaring costs, gaps in coverage, and absence of portability in health insurance, while preserving the high quality of care available to all Americans.

How the Clinton Plan Would Affect Americans

The broad outlines and likely consequences of the Clinton Plan might alarm a particular family or they might seem attractive. But the real story is in the details-those are what will determine how the Plan, if enacted, will change the way each family receives and pays for care.

Today approximately 86 percent of Americans are covered by health insurance, usually through their place of work. Polls show they are overwhelmingly satisfied with the quality of medical services they receive. 10

But many Americans are anxious that because of rising costs or a job change, they may not be able to keep their health benefits in the future. This worry is a structural result of the way in which the tax code penalizes every method of obtaining benefits other than through a company-sponsored plan. This tax treatment also fosters the rapid escalation in health care costs. 11 While the Clinton Plan would enable Americans to count on a plan of some sort if they changed jobs, costs and benefits would still depend on their place of work, as well as their residence. And little is done to reform the inflation-inducing tax treatment of health care. This huge. encrusted edifice of longstanding federal tax policy, with all of its inequities, is left practically untouched by the Clinton Plan.

When considering how the Plan will affect them, Americans also need to note that the health care system today is heavily dominated by government. Approximately 44 cents out of every dollar spent on health care is spent by government, and the health care industry itself-especially the health insurance market-is already one of the most highly regulated sectors of the American economy. Yet while the authors of the Plan acknowledge that bureaucracy "overwhelms consumers and providers," they prescribe even more of it. 12

The Clinton Plan creates several more layers of government bureaucracy. These include a powerful National Health Board, new federal advisory bodies, new rules governing reporting and data collections, new mandates on the several states to comply with federal rules, and the creation of state-based regional health alliances.

Q. What is the National Health Board?

A. Under the Clinton Plan, the National Health Board is established as a new federal agency, part of the executive branch of government. It is created for the purpose of setting national standards for the new system, including health insurance coverage, cost containment, information gathering and evaluation, risk adjustment for health insurance, the encouragement of "reasonable pricing" of prescription drugs, quality of health care services, grievance procedures for enrollees in the state-based regional health alliances, the development of premium classifications, financial requirements for health plans and guaranty funds. It is also responsible for approval of state plans to implement the new system, and oversight over the administration of the new health care system when it is up and running in the states. 13

There will be seven members of the Board, serving four-year terms. Each will be appointed by the President and must be confirmed by the Senate. The Chairman of the Board will be able to serve a maximum of three terms, or twelve years.

Q. HHS Secretary Donna Shalala, during her October 5,1993, congressional testimony described the National Health Board as "a relatively minor oversight group." What are the functions of the National Health Board?

A. Secretary Shalala is incorrect, The Board would have wide rule-making standard-setting, and oversight authority, making it, in effect, the "Supreme Court of Health." All Board decisions on health benefits, performance standards, and procedures for accountability apply to state-based regional alliances and to the corporate alliances (see below) that large companies are permitted to create. According to the Health Security Act, the Board's powers include:14

Oversight of the health care system established in each state

The Board will establish standards and requirements for health insurance plans in the states, approve state implementation of health care reform, and monitor compliance.

Control over changes in the comprehensive health care benefit package

The Board's authority includes expanding the statutory standard benefits package all Americans receive, and issuing corresponding regulations. Under Title I, Section 1153, dealing with "high risk" populations, the Board is required to specify and define "specific items and services as clinical preventive services." For the general population, at any time before January 1, 2001, the Board "may by regulation" make appropriate adjustments or expand the comprehensive benefits package, "unless the Board estimates that the additional increase in per capita health care expenditures resulting from the addition or alteration for each regional alliance for the year, will not cause any regional alliance to exceed its per capita target (as determined under Section 6003(a))."15 In other words, what will or will not be in the standard health benefits packages available to Americans will be entirely in the hands of the members of the National Health Board, except if it thinks a particular medical service might be too expensive. Its decisions are final, unless Congress intervenes.

Establishing and enforcing compliance with a global budget for national health care spending

According to the "Health Security Act," the Board issues regulations for implementing a national health care budget in the form of caps on health insurance premiums. It also determines per capita premium targets, or baseline budgets, for every regional alliance in the country, as well as making sure that the allocation of national spending among the various health alliances around the country reflects "regional variations."

In adjusting the targets for the regional alliances, the Board also is to adjust the infla tion factor for each alliance to reflect "variations in premiums across states and across alliance areas with a state," information on "variation in per capita spending by state, as measured by the Health Care Financing Administration Medicare and welfare spending, and "area factors commonly used by actuaries."16 As noted, the Board also "certifies" compliance of the regional alliances with the national health budget.

Establishing and "managing" a "quality management and improvement system" for health care delivery

Under Section 1503(d) of Title 1, the Board is to "establish and have ultimate responsibility" for a performance-based system of quality management and improvement.

This new federal program is to be called "The National Quality Management Program." The day-to-day operations of the program are to be run by yet another new federal agency called the National Quality Management Council, composed of fifteen members appointed by the President who are "broadly representative of the population of the United States." Staff for the Council will be provided by the National Health Board.

The National Quality Management Council is to develop "measures" of "quality" in order to standardize the measurement of the performance of health plans. In other words, the Council will attempt to quantify "quality." To develop these "measures," under Section 5003(c), the Council is to consult with "appropriate interested parties," including doctors, insurers, consumers, and state officials, as well as "experts" in law, medicine, economics, and public health and health research, and certain federal officers and their agencies, including the Director of the National Institutes of Health, the Administrator for Health Care Policy and Research, an agency of the Department of Health and Human Services, and the Administrator of the Health Care Financing Administration (HCFA), the federal agency which runs the huge Medicare program. 17

Monitoring breakthrough drug prices

The National Board is not authorized to set drug prices. Under Section 1503(i) of Title I, however, the Board is to establish a special committee of its own membership called the "Breakthrough Drug Committee." While the legislative draft language is unclear on a specific set of responsibilities, it appears that this special Board committee is to coordinate its efforts with a new "Advisory Council on Breakthrough drugs," to be appointed by the Secretary of the Department of Health and Human Services.

The Council, in turn, is to monitor the prices of new "breakthrough" drugs and determine whether the initial prices are "reasonable." In the language of Section 1572 of Title I, a "breakthrough drug" is a drug considered to be a "significant advance over existing therapies." The Council is to investigate drug prices at the request of the Secretary of HHS if the Secretary thinks that the price may be "unreasonable." If the Council thinks that a price is unreasonable, after examining such data as other countries' drug prices, cost information supplied by the company, the projected volume of the prescriptions, "economies of scale," "product stability," "special manufacturing requirements and research costs," the Council tells the Secretary of HHS, and the Secretary can issue an official report to that effect.18 The bill language does not give either the Council or the National Health Board explicit powers to roll back a price, however.

Q. The Office of Management and Budget (OMB) normally can review regulations proposed by a federal agency, and can block them if they would be too onerous. Does OMB retain this function with the National Health Board?

A. Apparently not. Under Section 1505(e) of Title 1: "The National Health Board is authorized to establish such rules as may be necessary to carry out this Act." Given the massive scope of the Clinton Plan, this is an enormous concentration of regulatory authority. While OMB does have authority to review the budget of the Board, as established in Section 1506(b) of Title 1, the language does not include review of the Board's regulations. In any case, this interpretation of the bill language is clearly consistent with the spirit of the earlier September 7 Clinton Draft, which reads: "The Office of Management and Budget does not review regulations issued by the Board or its annual report to Congress prior to publication."19

Q. Can Board decisions be appealed?

A. No more than the decisions of any other federal regulatory agency, and less than most. Under Section 5232 of Title V of the proposed legislation, all of the decisions of the National Health Board relating to its imposition of premium caps on health insurance are exempt from either judicial or administrative review.

While the General Accounting Office can conduct routine periodic audits, and while there is no language in the Clinton draft that forbids congressional intervention, it is clearly the intention of the Clinton Administration to insulate the National Health Board from normal political processes. In response to an inquiry from Congressman Philip Sharp, the Indiana Democrat, during Hillary Rodham Clinton's September 28, 1993, appearance before the House Energy and Commerce Committee, Mrs. Clinton commented, "The National Board is a feature that is found in both the Senate Republicans' approach as well as the President's because we believe there needs to be some place where a lot of the decisions about benefits-how they're actually defined in individual cases, when a treatment moves from being experimental to clinically provable-those kinds of decisions need to be taken out of this body. They need to be taken out of politics." 20

While the National Health Board will regulate at the national level, the Clinton Plan makes it the legal obligation of each state to make sure that every American is enrolled in a health plan and that all health plans operating within the state meet the federal comprehensive benefit requirements. In effect, the states become the enforcers of federal health policy.

Each state is required to submit a detailed plan to the National Health Board--"in a form and manner specified by the Board"--showing precisely how it plans to comply with federal rules guaranteeing access to health insurance, how they will set up and staff regional alliances, how they will certify plans, administer subsidies for low-income individuals and small employers, collect data on health alliance and health plan performance, and meet federal quality, management and fiscal solvency requirements.21 And by January 1, 1998, each state must be a participant in the national health care reform plan, including the establishment of "one or more regional alliances" for the enrollment of employers and employees in approved health care plans.22

Q. What if a state fails to comply with these rules or meet the deadlines?

A. The Board must first determine that the state's failure to participate "substantially" jeopardizes the access of state residents to the federally established comprehensive benefits package. If so, the National Health Board informs the Secretary of HHS, who is authorized to withhold federal health appropriations, such as payments to academic health centers, federal research funds, or federal payments to hospitals in the state.23 If a state still resists, the federal government will directly assume responsibilities of the "non-participating" state. The Board can order the appropriate regional alliance to enroll state residents. And under Section 1522(b) of Title 1, the Secretary of HHS can intervene directly and establish one or more health alliances in the state, and is empowered to take such steps "as are necessary" to ensure that the "comprehensive benefits package is provided to eligible individuals in the state during the year."

Q. How can the federal government finance a regional alliance if a state resists or cannot meet a deadline?

A. Effectively by taxing businesses and workers in the state. If a state does not meet the deadline, the Secretary of HHS, under Section 1523 of Title I, is empowered to pay for the establishment of regional alliances and the availability of the comprehensive benefit package through a special surcharge. The Secretary can impose a 15 percent surcharge on all health insurance premiums to offset any "administrative or other expenses" incurred by the Secretary of HHS in "establishing and operating the system."24

Q. Can states avoid the danger of a regional alliance monopoly by setting up more than one alliance in an area to foster competition?

A. No. Under the Clinton Plan, "No geographic area may be assigned to more than one regional alliance."25

Q. Let's say a state legislature thinks it has a better plan to deliver less expensive universal health care than that devised by Washington. Maybe it wants to introduce a more marketbased system, or perhaps a Canadian-style single-payer system. Can it do so?

A. The only alternative state-based reform option allowed is a single-payer, government-run health care system with at least the same level of benefits mandated in the federal comprehensive benefits package. Under a single-payer system, of course, consumers are denied the freedom of choice of alternative health insurance plans, because there is no alternative. Under the proposed bill language, veterans, active-duty military personnel, and persons enrolled in the Indian Health Care system would be exempted from the mandatory enrollment in a single-payer system. Persons enrolled in either a corporate alliance, a special arrangement for big business with over 5,000 employees or the Medicare program would be forced into a single-payer system at the option of the state government.

Significantly, states are actually encouraged to set up government-run health care systems, because the proposed bill language makes it easier to establish them, exempting them, for example, from the federal rules related to the establishment of regional alliances and state guaranty funds.26 After consultations with congressional supporters of a Canadian-style system, the White House eliminated several major administrative hurdles for states, making it easier for them to adopt such a system. Moreover, under Section 1221 of Title I, the National Health Board has limited legal discretion in approving single-payer applications; the proposed bill language says the Board "shall approve" such applications if the specific legal conditions are met by the state. Beyond these changes for the states, at least one unnamed Clinton Administration official acknowledges that the White House is promoting within its own plan the framework for a government-run health care system: "'What they did was to take the form of managed competition and filled it up with content that looks a whole lot like a Canadian-style government system,' a Clinton adviser said this week, deviating from the official White House line."27

Q. What federal rules apply to the geographic boundaries of state regional alliances?

A. States will be legally obligated to make sure that they do not establish boundaries or rules for an alliance that could lead to discrimination based on race, gender, income, or even health risk. According to the proposed bill language, "The entire portion of a metropolitan statistical area located in a state shall be included in the same alliance area."28

Q. If the states draw the boundaries for the regional health alliances, isn't there a danger of "gerrymandering"-like the creative drawing of congressional district boundary lines-in order to assure cheaper premiums for favored constituencies?

A. Yes. Elizabeth McCaughey, who is a fellow at the Manhattan Institute of New York, notes that, "The system promises to pit black against white, poor against rich, city against suburb."29 There will be strong political pressure on state officials by groups wanting to be included or excluded from certain alliances. Voters will want areas with a higher-than-average incidence of older citizens or retirees, teen pregnancy, violent crime, or HIV infection excluded from their alliance, and areas with low potential health costs included. As McCaughey observes, "Everyone will figure out that you get more health care for your dollar or pay lower premiums in an alliance without inner city problems. The plan will be an incentive for employers to abandon cities and relocate."30 Real estate prices also are likely to be affected, p, just as they are today by the geographic boundary of the public school catchment area.31

Q. But won't the Clinton Plan's anti-discrimination provisions stop gerrymandering?

A. Probably not. Because state boundary-setting, decisions will mean huge costs or savings for families and businesses, there is likely to be intense political in-fighting and an avalanche of law suits. As Richard Grenier of the Washington Times remarks, "...the plan has enough districting rules and gerrymandering possibilities to keep the courts busy for generations ."32

Q. The Plan requires "community rating" for insurance plans. What does that mean?

A. Under community rating, an insurance company must offer insurance at the same premium for any individual or group, regardless of health risk.

Q. What are the consequences of community rating?33

A. If insurance companies are legally forbidden to take health risk into account, it means that younger and healthier individuals are overcharged for their health insurance premiums-since these are not permitted to reflect their better health condition-while older and less healthy individuals are undercharged for their insurance premiums.

Community rating also tends to lead to higher average costs. For example, New York state passed a health insurance reform law in 1992 which requires all insurance companies to set insurance rates without regard to age, sex, or medical condition. The result, according to the New York State Insurance Department,. is that the average price for commercial insurance for individuals was driven up by 18 percent, for small groups by 19 percent, and for some New Yorkers by as much as 100 percent.34 Not surprisingly, state legislators have been deluged with complaints about the new law from angry consumers, but New York officials defend themselves by saying that is only a one-time jump or that the rates of the higher risk people are going down. "Pointing out that rates for many older people have actually decreased," reports The New York Times, "the officials say that New York's experience is likely to be mirrored nationally, when consumers find that health care reform might well mean higher costs for many people."35 Of course, the solution to higher insurance premiums under the Clinton Plan is simply to make them illegal above a nationally ordained level.

Q. Doesn't this mean that if a plan happens to attract higher-risk individuals and groups, its premiums can't be raised, but it may face huge payouts and be in danger of financial collapse?

A. Exactly. In order to compensate for this "adverse selection"--a problem inherent in community rating-the states must use a federal model for risk adjustment that factors in differences in patient populations related to demographic variables such as age and gender, the number of people on public assistance, geography, socio-economic status, and health status.36 The National Health Board is to develop such a model for a national risk adjustment system, with extra help from yet another yet federal agency. The Board is to create a special fifteen-member Advisor\ Committee to provide technical assistance for the development and modification of the methodology to establish a national risk adjustment mechanism.

Q. What if a state thinks it has a better way of adjusting for risks than that set down by the federal government?

A. It must apply to the National Health Board for the privilege of introducing it.37

Q. If premiums must not reflect risk or health condition under community rating, what incentive would employers or employees have to try to keep their health costs down?

A. Little or none, since keeping their own costs down would not lower their premiums. In particular, companies and individuals would no longer have a financial incentive to reduce insurance costs through "wellness programs" or change personal behavior by cutting down on smoking or other habits that tend to increase health costs.

Q. Under the Clinton Plan, what is the role of the states in approving health plans?

A. The states are legally required to approve all health plans, subject to all applicable new federal rules and regulations. In approving health insurance plans, states are specifically required by federal law to assess the "quality" of health plans, their solvency or financial condition and their "capacity'' to deliver the federally determined comprehensive benefits package. Only health plans that are "qualified" by the state, according to these criteria, can offer a health insurance package through the regional alliances.38

Q.Will the National Health Board preempt all state regulation of health insurance rates?

A. No. The states may regulate premium rates in order to meet federal spending targets or ensure a plan's solvency.39

Q. What solvency requirements does the Clinton Plan place on states?

A. States must establish "capital standards" that meet federal standards for health plans. The minimum capital requirement for a health plan is $500,000. States are required also to establish a "guaranty fund," or trust fund to pay doctors and other health care providers if a health plan becomes insolvent or fails. If a health plan fails, states are authorized to assess up to two percent of premiums of all other health plans in an alliance to cover the costs of the failed plan.40

Q. The Clinton Plan specifies a comprehensive federal health benefits package for health insurance companies. Does this mean an end to state mandates on insurance companies widely blamed for a large increase in costs in some states?

A. No. States can still mandate additional benefits above and beyond those contained in the comprehensive benefit package. The only limitation spelled out in the Clinton draft is that states cannot pay for such extra benefits by using the funds to finance the Clinton Plan.41

The Role of the Regional Health alliances

If the National Health Board is the brain center of the Clinton Plan, the regional health alliances, the state-sponsored health insurance cooperatives, constitute the bone and muscle of the new system. These extremely powerful state-based cooperatives are to accept bids from approved health plans; collect all of the health insurance premiums; provide consumer information; represent the interests of the employers and employees who purchase insurance within a given geographical area; oversee "the market" to assure the delivery of "high quality" and "cost effective" care; and assure that every citizen, armed with "the health security card" provided to them by the regional alliance, is enrolled in a government-approved health insurance plan.42

States must establish the regional health alliances by January 1, 1998.

While Clinton Administration officials downplay the role of the regional alliances as regulatory agencies, they have impressive powers. Not only do they have the authority to impose "prospective budgeting" and fee schedules on doctors, but also, under Section 1352 of Title I, regional alliances enjoy the power to assess businesses and workers up to 2.5 percent of their premiums to provide for their own "administrative allowance," plus levy another 1.5 percent to give to HHS for federal funding of academic health centers and graduate medical education programs.43

Q. Is the regional health alliance a public or a private entity?

A. According to the proposed bill language, it could be a non-profit private corporation. But it also could be an independent state agency, or an agency of the executive branch of state government. The choice is up to state officials.

Whatever choice the state makes, however, there are federal rules on how the Board is to be set up. It is to be composed of equal numbers of employers and consumer representatives, but may not include doctors, representatives of health care industry, or any individuals who "derive substantial income" from pharmaceutical companies and suppliers of medical equipment, devices, and services.44 States may also establish a "Provider Advisory Board," composed of doctors and other health care professionals who live and work in the region controlled by the health alliance.

Q. So the alliances may be nothing more than a new state agency?

Q. How many more bureaucrats will staff these new regional alliances?

A. According to Laura Tyson, Chairman of the President's Council of Economic Advisers, approximately 50,000 new positions will be created in staffing the regional alliances, a substantial portion of the 400,000 jobs the Clinton Administration expects its legislation to produce.45

Q. How is the regional alliance supposed to "manage" the geographically defined "market"?

A. Each regional alliance negotiates and contracts with the health insurance plans it approves. The alliance decides which plans are permitted to operate in its geographic area and it exercises firm control over the marketing policies of health plans: "Each regional alliance shall review and approve or disapprove the distribution of any materials used to market health plans through the alliance."46

Q. Can a regional alliance prevent a plan being offered to consumers?

A. Yes. The regional health alliance must normally offer contracts to health plans meeting the federal conditions, but it still has reserve powers to exclude a plan. For example, a regional alliance may exclude a plan if its proposed premium exceeds the average premium within the alliance by more than 20 percent; if the plan fails to offer coverage for "all services" as outlined in the federal government's comprehensive benefits package; if the alliance finds that the plan discriminates against any group of the basis of race, ethnicity, gender, income, or health status. 47 The 20 percent standard may in practice prevent many fee-for-service plans with full choice of doctors from being offered in most states. With the "approval of the applicable regulatory authority," the alliances can also allow a plan to limit its enrollment because of the plan's limited "capacity to deliver services or to maintain financial stability."48

Q. If regional alliances run short of funds, can they borrow money?

A. Yes. Under Title IX, Subtitle C, Section 9201, the Secretary of the Department of Health and Human Services can make loans available to "cover any period of temporary cash-flow shortfall" because of an administrative error, an erroneous estimate of insurance risks (such as a miscalculation of the proportion of welfare recipients in the region or average family premium payments), or cash-flow shortfalls relating to the "timing of the year'' between payments and disbursements to the alliances. In making these loans the Secretary of HHS is to consult with the Secretary of the Treasury on the rules governing the terms and conditions of these loans and is also to make an annual report to Congress.49 Naturally, the creation of a new federal loan program is another invitation for future federal bailouts at the expense of the taxpayer.

Q. Are there any major exceptions to enrollment in a regional health alliance?

A. Yes. Companies with over 5,000 employees nationwide may act as their own alliance if they do not want to join a state-established regional health alliance. These large employer-based systems are called "corporate alliances."50 In general, they must follow the same federal and state rules that will apply to the state-sponsored regional alliances. But oversight over corporate alliances rests with the U.S. Department of Labor, and corporate alliances are temporarily permitted to use a different kind of insurance rating system.51 They are not initially required to use community rating.

Q. Inasmuch as federal workers and retirees are exempted from the legal requirement to enroll in the new regional alliances until after the new system is up and running in the states, won't this affect the premiums paid by many private sector workers?

A. Yes. Federal workers, retirees, and dependents account for almost ten million people, one out of 25 Americans who have health insurance. In states or metropolitan areas with a large number of federal workers and retirees, plus a high proportion of lower paid workers or a relatively large number of people being folded into the system who are now on Medicaid, the big government health program serving the poor and the indigent, overall premium costs will go up. Without federal workers participating, and thus helping to spread risk and the cost of coverage in these areas, premiums for everybody else will be higher.

Q. What happens to a worker who moves from a corporate alliance to a firm in a regional alliance?

A. If the corporate alliance plan has an even more generous plan than that required by the government--and those more generous benefits are tax-free at least until January 1, 2003--chances are that any move to a smaller firm enrolled in a regional alliance is likely to result in the worker paying more for a lower level of benefits.52

Limitations on Comsumer Choice

Q. The President emphasizes "choice" as one of the six principles of his reform plan. Do families have the freedom to choose a health care benefits package outside of the regional health alliance?

A. No. The choice available to families is limited by the government, with very few exceptions. As the Manhattan Institute's Elizabeth McCaughey remarks, "Unless you now receive health care through Medicare, military or veterans benefits, or unless your spouse works for a large company, the law will require you to buy basic health coverage from the limited choices offered by your alliance. It will be illegal to buy it elsewhere."53

Q. What if an individual doesn't enroll in a plan within the regional alliance?

A. Then, under Section 1323(h)(i) of Title I, the officials of the regional alliance can enroll him in a plan of their choice, and the individual will be required to pay twice the premium he would have otherwise paid.

Q. Since the Clinton Administrations description of the employee's "contributions" is not designated a "tax," what if a person chooses not to "contribute"?

A. He or she will be forced to "contribute." Under Section 1345(b)(1)(A) of Title I, the person's employer will deduct from his paycheck what he owes. Section 1344(b) makes it clear that if the amount a person owes is not paid by the applicable deadline, then he will be subject to interest and penalty charges; Section 1345(d)(2) says that for "repeated failure" to pay a person can be assessed civil and monetary penalties up to $5,000 or three times what that person owes, "whichever is greater." Regional alliances, under Section 1345(a) of Title I, are authorized to use credit and collection procedures to collect the money with assistance from state governments. And the states are authorized, under Section 1202(d) of Title 1, to help the regional alliances collect monies owed, and "shall assure that the amounts owed are paid." And for good measure, Section 1345(d)(2) says that the Secretary of Labor can also help the regional alliances with collections.

Q. Can families buy a plan with more generous delivery of the standard benefits?

Q. What if individuals want to purchase medical services directly, paying cash for those medical services outside of the regional alliance system?

A. They can. According to Section 1003 of Title 1, "Nothing this Act shall be construed as prohibiting...an individual from purchasing any health care services." So, it is not illegal to pay for medical services directly in cash, without any tax relief.Q. Will a family be able to choose its own doctor?

A. Theoretically, a family's choice of doctor would not be compromised. The language of the proposed bill in this respect retreats from the more restrictive provisions of the September 7 Clinton Draft. First, the Clinton Plan requires every regional alliance to have a "point of service option," whereby families can see a doctor of their choice outside of their health plan, though it is likely that families will have to pay more in doing so. Second, under Section 1322(b) of Title 1, each regional alliance is to include among its health plans "at least one" fee-for-service plan, a health insurance plan where families can choose any doctor they want and the health insurance company reimburses the doctor for his services. But given the regulatory pressures imposed on fee-for-service-medicine in the Clinton Plan-including state and regional alliance fee schedules, restrictions on balanced billing and prospective budgeting-the legal prescription of one such plan is likely to be the fact of life for many, if not most, Americans. As Newsweek reporters Tom Morganthau and Mary Hager observe, "The Clintonites say fee-for-service medicine would continue to exist, but this is somewhat disingenuous: under the president' s plan, fee-for-service doctors would operate under price schedules established by the alliances."55

Q. Then what kind of relationship are Americans likely to have with physicians in the Clinton Plan?

A. The dominant health insurance model envisioned under the Clinton Plan is a health maintenance organization (HMO), in which patients are in practice denied a choice of doctor and the services of specialists are more limited. The Plan clearly encourages this type of health care delivery, and discourages fee-for-service medicine.56

Q. But won't families be able to maintain a long-established relationship with their personal physician, even if the choice of specialist is limited?

A. Probably not. While the regional alliances will be required to provide Americans with a "point of service option," so that they can see their physician even if he's not participating in the plan in which they are enrolled, the bigger question is whether that doctor will be available in such a heavily regulated environment. Moreover, the legal requirement of at least one fee-for-service option is offset by the regulatory hassles that will accompany physicians enrolled in such a plan. The constant pressures of remaining within the federal and the regional alliance budgets with the threat of fines, plus the likely imposition of fee schedules, and limitations on balanced billing, makes fee-for-service less attractive to physicians. In any case, the ideal of the traditional, independent, private medical practice is unlikely to survive in such an environment. As Newsweek recently reported, "Despite the president's attempts to be reassuring about the changes that will ensue, there is a very good chance that our relationship with our current doctor will be disrupted--the physician may leave medicine altogether or join a health plan we do not choose to join."57

Q. What if a family still wants the services of a particular physician who is not a member of an approved health plan?

A. If the doctor is in private practice outside the system, they will have to go outside their plan and they pay for all that physician's services themselves, in after-tax dollars. There is no tax relief for such out-of-pocket expenses. This may be no problem for the rich, but it will be for everyone else.58Q. The President says that his plan does not include price controls on doctors. Is that true?

A. No. The Clinton Plan establishes a framework for tough price controls on doctors' services in fee-for-service plans. Each regional alliance, following negotiations with doctors, can establish a set "fee schedule" for physicians' services. Furthermore, states can establish their own fee schedules on all doctors in fee-for-service plans statewide.59 Moreover, a doctor may not charge or collect from a patient a fee in excess of the fee schedule adopted by a state government or an alliance.60 This is clearly a price control. Finally, according to the Clinton draft, states are authorized to adopt a statewide fee schedule and are empowered to impose "prospective budgeting" on fee-for-service plans offered through the regional health alliances.61

Beyond the specific powers of state officials and regional health alliances to control the geographic markets, the Clinton Plan establishes a system of "assessments," or fines, to be levied on those doctors and health insurance plans who stray from the regionally allotted and adjusted budget targets set by the National Health Board in Washington.

A Government-Standardized Health Benefit Package

The Clinton Plan requires every health plan to offer a standardized package of health care benefits. This should not be confused with a basic benefits package or a "minimum" or catastrophic benefits package. It is a comprehensive benefits package, covering a broad range of medical services, and it is the package-no more and no less-that most Americans must have.

The benefit package is very detailed. It will provide major medical coverage, including an impressive array of hospital and physician services, diagnostic services, preventive care. mental health and substance abuse benefits, family planning and "pregnancy related" services. inpatient and outpatient prescription drugs and biologics, hospice, home health and rehabilitative services, durable medical equipment, prosthetic and orthotic services, vision and hearing care. and preventive dental care for children. Health plans are also "permitted" to include "health education classes" in their packages.62

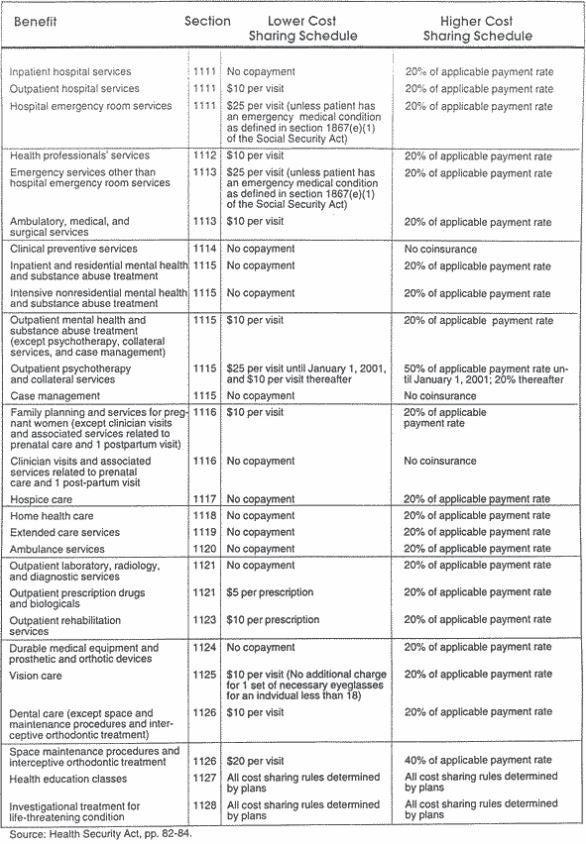

In outlining the comprehensive array of benefits and treatments, the proposed bill language covers 56 pages, with many unspecified details simply left up to the National Health Board. In other cases, the coverage is very specific (See table, next page). For example, under Section 1114 of Title 1, dealing with clinical preventive services, Congress is to enact which regular shots and tests Americans get and when. Among the items specifically excluded from the benefit package: in vitro fertilization, sex change operations, and dental implants.

According to the Clinton Plan, market forces can have no role in setting copayments, coinsurance, and deductibles. Rather, the draft details the cost-sharing and coinsurance requirements for the comprehensive health plans. Health plans are limited to three cost-sharing options. Low costsharing plans would have to require a $10 copayment for outpatient services and no copayments for inpatient services. They may offer a "point of service option," with higher coinsurance. High cost-sharing plans can require a $200 deductible for individuals and $400 deductible for family coverage, 20 percent coinsurance, and a maximum out-of-pocket spending limit of between $1,500 and $3,000. A third option allows plans to offer a "combination" if subscribers use preferred providers (PPO physicians) and higher-cost sharing, or a 20 percent coinsurance if subscribers use doctors outside of a PPO network.63

Q. Does the comprehensive health package contain abortion coverage?

A. Yes. Thus, all American employers and employees will be required to finance elective abortion. Abortion coverage is subsumed under the euphemistic phrase "pregnancy related services."64

Q. How can new medical treatments, procedures, or benefits be added to the comprehensive benefits package?

A. Slowly, and with great difficulty. New benefits, including new treatments, medical procedures, or devices for the treatment, prevention, or cure of disease must be approved by Congress or the National Health Board before they can be covered in an alliance plan. Moreover, under Section 1141 of Title I of the proposed legislation, the Board, by regulation, can exclude any item or service that it may determine not -medically necessary.Q. Do we have any experience with federal agency approval of new benefits or medical services or devices in this way?

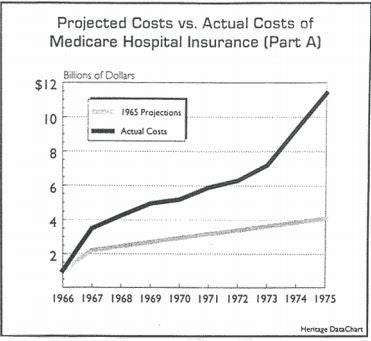

Americans should be alarmed at the prospect of a system like this for the general health care system. Consider the crucial area of medical technology. According to a study of Medicare by Senator David Durenberger, the Minnesota Republican, and Susan Bartlett Foote, a congressional health policy analyst, Medicare technology evaluation has been underfunded because of competing budgetary priorities, such as payment for a growing volume of medical services. Moreover, say Durenberger and Foote, the evaluation has been hobbled by ineffective assessments of the cost-effectiveness of technology, distorted by the politicization of HCFA's decision-making process, and burdened by an inability to respond in a timely fashion.65 As Durenberger and Foote note, "A bureaucratic approach to technology policy that would affect all Americans, not just the Medicare population, raises serious concerns. OHTA performed only about 10 assessments in 1991 and eight in 1992. Some assessments have been buried in the bowels of OHTA for over three years."66

What is true of medical technology assessment is true of Medicare's benefit changes. However, organized political action is used to win approval of certain benefits. Wrote Jeremy Rosner, then a scholar at the Washington-based Progressive Policy Institute, and now a Clinton Administration official, "The history of Medicare is replete with cases of organized groups acting through Congress to add coverage for specific illnesses or procedures, or to affect changes in specific prices."67 When considering the procedure for adding new benetits; to the package, Americans might also be alarmed when they consider the long delays in drug approval by the Food and Drug Administration (FDA).68 Because of the bureaucratic delays in approval of lifesaving drugs, for example, the Bush Administration found it necessary to launch an overhaul of the FDA regulatory process and expedite approval of new drugs to treat deadly diseases such as AIDS, cancer, and cystic fibrosis.

Q. Do we have any experience with government agencies setting benefits?

A. Yes. The Medicare program provides a vivid example of how benefits are determined in the political process. Virtually any benefit change in the Medicare program becomes a major political event, involving Congress and the Health Care Financing Administration. Witness the debate. passage, and then the repeal of the Medicare Catastrophic Coverage Act of 1988. Moreover, at the state level, there are approximately 1,000 state laws that mandate insurance coverage of all kinds of benefits, ranging from mandatory chiropractic care to the provision of in vitro fertilization. For medical specialty groups, or groups afflicted with particular medical conditions, the National Health Board, and inevitably Congress, will become the central focus of intense lobbying over the addition or substraction of medical benefits. This will compound the politicization of the health care system, already established through state government management of the regional alliances.

The Cost to Employers and Employment

Every employer is mandated to participate in the financing of health care reform. For full-time employees, the employer must pay at least 80 percent of the average premium for the individual or family coverage of the employee. But employers may pay up to 100 percent. The employee pays no more than 20 percent of the average cost plus any extra premium for selecting a higher cost plan.

Employers have two options. First, they may place all their employees in a regional alliance. For any employer

choosing to join a regional alliance, there is a cap on the total contribution made by the employer. The federal

government makes up the difference between this cap and 80 percent of the average premium. With this subsidy, the employer contribution for firms with 75 or fewer workers, as a percentage of payroll, ranges from 3.5 percent for low-wage employers to 7.9 percent of payroll for high-wage employers. No employer in a regional alliance will be legally obligated to pay more than 7.9 percent of payroll for health insurance.69 Low-wage workers in regional alliances will also receive government subsidies to help them pay their share of premiums.70 Under the Clinton Plan, no family with an adjusted income of less than $40,000 per year will pay more than 3.9 percent of income.

The other option for a company, if it has 5,000 or more employees, is to set up a corporate alliance. This means that the company's managers can organize their employees into their own corporate purchasing cooperative where their workers may purchase health insurance, choosing from at least three plans: a fee-for service option and two plans that are not fee-for-service plans, The same rules that apply to regional alliances also generally apply to corporate alliances, except that big employers get no federal subsidies and the oversight over the corporate alliances is the responsibility of the Secretary of Labor. The Secretary of Labor has the power to dissolve any corporate alliances if they do not meet their federal budget targets in a timely fashion. And if a corporate alliance should become insolvent, the Secretary of Labor can take it over and manage it directly as a trustee. In this instance, the Secretary is authorized to make payments for the government's guaranteed health benefits package from another, newly created federal institution: the Corporate Alliance Health Plan Insolvency Fund.71

Q. Do corporate alliances receive the same subsidies?

A. No. Firms choosing to get up a corporate alliance face a double whammy, making such alliances very unattractive. First, it is the employer, not the government, who subsidizes the employee's share of the premium for low-wage workers. And second, subsidies are not available to corporate alliance employers. In other words, the payroll caps on premium costs do not apply to them.72

Q. If a company in a regional alliance must pay at least a fixed amount of money to the alliance (80 percent of the average premium), no matter what benefits the employee receives, isn't this really a tax?

A. Yes, and some officials at the Congressional Budget Office want it to be called a tax.Q. Are part-time employees covered under the employer mandate?

A. Yes. While part-time workers are covered by the regional alliances, employers will still be compelled to contribute to a pro-rated share of 80 percent of their health insurance premiums according to the number of hours worked per week.

Q. What is the likely economic impact of an employer mandate?

A. Any mandate on employers to provide health insurance necessarily adds to the Labor costs of firms that do not now offer health insurance, or that offer a package less generous than the mandatory plan. Increased Labor costs necessarily translate into higher prices for consumers for goods and services in the general economy or reduced compensation for employees in the form of wages or other benefits. Depending on the size and the resources of the firm, the increased Labor costs will translate directly into lower wages or job loss.

Q. How many jobs will be lost?

A. It is difficult to tell and the response varies. Ira Magaziner, the President's chief advisor on health care reform, has argued that the Clinton Plan will create jobs. But most liberal and conservative economists and journalists disagree and expect higher unemployment to accompany a universal employer mandate. Time magazine recently reported an estimate of the loss of 1 million jobs.73 An even more recent study conducted by Professors June and David ONeill of Baruch College for the Washing ton- based Employment Policies Institute estimates the job loss of an employer mandate at 3.1 million, with 75 percent of that loss concentrated in such low-wage service industries as restaurants and agriculture.74 Likewise, the Washington-based Employee Benefit Research Institute, reports that between 200,000 and 1.2 million workers could lose their jobs as a result of an employer mandate, depending on the extent to which companies will decrease wages to compensate for the increased costs of health benefits.75 Even the Clinton Administration's own economic advisers concede there may be substantial job losses. Council of Economic Advisers Chairman Laura Tyson said that the job loss from an employer mandate would be about one half of one percent of the workforce in the general economy--roughly 600,000 jobs--but Ms. Tyson considers this impact to be "very small."76Q. Will mandates affect each business differently?

A. Yes. In general, small businesses will have trouble coping with mandates. The Clinton Plan hopes to alleviate that problem, in the short term at least, with its employer and employee subsidies. For large corporations with generous health compensation packages, an employer mandate can have a much different effect. Large employer-based health insurance plans currently are taxfree without limit, and are often well in excess of the 7.9 percent payroll limit that the Clinton Plan would impose for small firms in the state regional alliances. Given the Clinton Plan's provision that such a firm is legally obligated to spend only 7.9 percent of payroll on insurance, it is a direct incentive for self-insured big companies with large and generous benefits packages to join a regional alliance, scale back their coverage to the standard benefits package mandated by the federal government, and pick up the subsidies after a few years. Unless employees are successful in securing the difference in wage increases, a difficult proposition if they are not covered by collective bargaining agreements, they could lose generous tax-free compensation.

Q. In other words, the Clinton Plan provides subsidies that would make it difficult for employers and employees enrolled in corporate alliances to remain outside of the regular state-based regional alliances?

A. Yes. Under the Clinton Plan, the only employers eligible for government subsidies and the 7.9 percent limit on the payroll contribution to employee health insurance are firms enrolled in the regional alliances. Large employers, with more than 5,000 employees, especially if those employers have a benefits package less generous than that of the comprehensive government package or who have a low-wage workforce, could have much higher health care costs as a percentage of payroll.Q. What kind of subsidies does the Clinton Plan provide for large companies that give up their corporate alliances and enroll in the regional alliances?

A. In the transition from a corporate alliance to a regional alliance, the large companies would get no subsidies for the first four years. In the fifth year, they would get 25 percent of the subsidies given to other firms on a progressive scale until the eighth year, when they would get the full subsidy (100 percent), the same level of subsidy that is provided to every other company in the state-based regional alliance.77

Q. What other special government benefits do large companies receive in the plan?

A. One very large one is that the Administration intends to force the taxpayers to pick up 80 percent of the cost of corporate health benefits for early retirees, those who retire between the age of 55 and 65. )While the number of companies providing health insurance coverage for their retired workers is steadily shrinking, the practice is still prevalent among very large industrial corporations, such as the firms of the auto industry. In 1994, providing coverage for early retirees would cost taxpayers about $13.6 billion.78 The Clinton Administration is proposing to offset these new federal obligations with a special "one-time" tax on the affected companies based on a calculation of their financial gains from the government assumption of the bulk of their retiree health costs. A natural side effect of the Clinton prescription for federal coverage of 80 percent of early retiree costs is, of course, a new incentive on the part of firms that have such retiree health insurance programs to "downsize," cut the size of the older workforce, knowing that the taxpayers will also pick up this new health insurance bill.

How Other Government Programs are Affected

Under the Clinton Plan, Medicare will be retained, but states can open up the health alliances to Medicare beneficiaries if they have the same or better coverage and if the federal financial liability is not increased. After the alliances are established, Medicare beneficiaries will have the right to elect to join them or remain in Medicare. At the same time, the Medicare program will have, by July 1 1996, a new prescription drug benefit. Medicare will cover outpatient prescription drugs, with a $250 deductible, a 20 percent copayment, and a cap on out-of-pocket expenses at $1,000.

While the Clinton Plan establishes a new prescription drug benefit, all Medicare beneficiaries earning more than $100,000 a year will pay 75 percent of the cost of their benefits, not 25 percent, as they do today. Moreover, the Medicare program is expanded by extending both the coverage and the Medicare hospitalization tax on all state and local government employees.79

On the other hand, Medicaid beneficiaries receiving acute care services, the poor and the indigent, will be fully integrated into the state-based regional health alliances. Medicaid beneficiaries will be subsidized.

The Department of Defense will establish its own health system in accordance with the national standards set forth for national health reform, including the establishment of the national standard benefits package. The same general rule applies to the Veterans Administration Health system. It can organize its hospitals and clinics into health plans, as long as these plans provide the standard benefit package. The Indian Health Service, however, will remain outside of the regional alliance system, and the rules governing the standard benefits package, at least for the next five years.

The Federal Employee Health Benefits Program (FEHBP) is to be abolished, effective December 31, 1997--only after all ordinary working families already are under the Clinton program. Based largely on the market principles of consumer choice and competition, the 33-year-old federal health program is unusual in the sense that it is a consumer-driven system.80 The timing of the abolition of the FEHBP represents another change in White House policy on the sensitive topic. In the original September 7 Clinton Draft, the program covering the President, the White House Staff, Members of Congress, congressional staff, and over nine million federal workers, retirees and deendents was to be phased out and all federal

Q. Next year, according to OPM, average premium increases in the FEHBP will be only 3 percent, and 40 percent of employees and retirees will actually see a decrease in their premiums. If the FEHBP has been working well for over three decades, why does the Clinton Administration intend, eventually, to abolish it?

A. Good question!82

Q. If the FEHBP is eventually abolished, what would this mean for federal workers and their families?

A. It means that they will lose their broad range of choice of benefits and plans they have now, including health plans they have personally chosen and may have subscribed to for many years. While the Administration spokesmen have been trying to sell federal workers on the proposition that reduced range of choice and a standard benefits package is really better for them, throughout the summer of 1993 federal union leaders have been saying that being included in the Clinton health care reform programs means that they will be paying more and getting less in benefits.83 In a remarkable September 13, 1993 letter to Ira Magaziner, the senior health advisor to President Clinton, John Sturdivant, the President of the American Federation of Government Employees (AFL-CIO) writes, "It would be disingenuous for AFGE to try to convince the majority of our members that this plan offers anything other than a decrease in their level of coverage.. ..We have said all along that AFGE would be fully supportive of the plan and its goals of universal coverage and security as long as our members did not end up paying more for less. But this plan does just that."

Q. Are all federal workers and enrollees in the FEHBP being treated the same?

A. No. Postal workers, who are represented by the powerful federal postal unions, would be allowed to enroll in their own corporate alliance through the United States Postal Service.

Q. Why are Members of Congress and federal workers and retirees being folded into the new health care system after everybody else, and thus being treated differently than everybody else?

A. Because in Washington they are more politically influential than ordinary Americans. James King, the Director of the Office of Personnel Management (OPM), the federal agency, that runs the FEHBP, and Congressman William Clay, the Missouri Democrat who chairs the House Post Office and Civil Service Committee, persuaded Administration officials that including federal workers and retirees into the new system from the beginning would be unduly "disruptive," an official Washington concern that apparently does not apply with equal force to private sector workers. In another remarkable letter to Hillary Rodham Clinton, dated September 17, 1993, which highlights the various benefits of a delay, OPM's Director King writes, "I think that it is important that the FEHBP population be given the opportunity to see that national health reform is working before they are transitioned to it."Q. In other words, Members of Congress and federal workers and retirees are the last group scheduled to be in the Clinton health plan?

A. Right. They are not to come into the new system until January 1998, after the regional alliances are up and running in the states. And, if the national test results on private sector businesses and workers are not satisfactory, they might not even come in at all.84The President says he can finance his health care reform proposal without broad-based new taxes. Few agree.

When the President first presented his financing projections, Senator Daniel Patrick Moynihan, the New York Democrat who is chairman of the Senate Finance Committee, dismissed them as "fantasy." Barry Bosworth, a former economic advisor to President Jimmy Carter and a scholar at the Brookings Institution, said, "This is a proposal that is not funded."85 Likewise, Rudolph Penner, former director of the Congressional Budget Office, remarked, "It is financed by assumption-that you can cut Medicare and Medicaid by very, very large amounts, much larger than we've ever cut them before. That does not sound very plausible."86