(Archived document, may contain errors)

953 August 4,1993

We view the federal employees program as a terrific system and we don't want to do anything that would hurt its effectiveness.

Robert Boorstin, Special Assistant to the President for Policy Coordination The President's Task Force on National Health Care Reform[REF]

I can say we're leaning toward [dissolving FEHBP absolutely

Robert Boorstin, Special Assistant to the President for Policy Coordination The President's Task Force on National Health Care Reform[REF]

INTRODUCTION

Question: At the end of the national debate over health care reform, will all new rules and regulations governing the access of Americans to health care services be exactly the same as those that apply to Congressmen and mailmen?

For both taxpayers and federal employees alike, this question takes on a special urgency. The reason: Inside the Washington Beltway, the clash of powerful political forces now taking place will influence significantly the outcome of the national health care reform debate.[REF] At stake in this struggle are the personal health care benefits of Members of Congress, congressional staff, members of federal employee unions, military families postal workers, and the very same federal officials who are writing and will administer the Clinton health care plan for all other Americans. The cast of characters in this Capitol Hill drama:

Members of Congress and congressional staff. Currently, Members of Congress and congressional staff are covered under the 33-year-old Federal Employee Health Benefits Program (FEHBP This is a unique, consumer-driven health care system covering nine million federal, postal, and congressional employees and their dependents.[REF] In the past, Members of Congress have proposed major health care reforms while specifically exempting themselves, congressional staff, and federal and postal workers from the system to be imposed on businesses and employees in the private sector-so that they can remain in the FEHBP.[REF] A key question for taxpayers today is whether Members of Congress will subject themselves to the same laws and regulations on health care that will govern all other Americans.

Federal workers and retirees. Powerful federal employee union leaders publicly back the Clinton Administration's comprehensive national health care reform-but strongly oppose including federal workers in such a system. The major reason: federal workers and their families fear they will pay more for health care services, but receive less for their dollars. These federal and postal workers, retirees, and their families also are enrolled in the Federal Employee Health Benefits Program. And in sharp contrast to the private sector employer-based system, many federal employee organizations, including unions, sponsor their own health insurance plans. Indeed, over one-third of all federal employees and their families are enrolled in union- or employee-sponsored health insurance plans.

Military families. At the very time the Clinton Administration is thinking of abolishing the FEHBP for federal workers and their families, the National Military Families Association (NMFA) wants military wives and children to have the right to enroll in the FEHBP under the same terms and conditions as the families and dependents of federal civilian employees. Right now, almost six million military dependents and retirees are enrolled in the costly Civilian Health and Medical Program of the Uni formed Services CHAMPUS In speaking of the FEHBP option, NMFA Executive Director Dorsey Chescavage says: Its operational and its successful. Why reinvent the wheel? We could go into the program during the next open season in November.[REF]

The reason the Clinton Administration is considering trying to abolish the FEHBP is that it is politically impossible for White House officials to advance a national health care reform while excluding from it themselves, Members of Congress, and other federal workers. But if the Clinton Administration is successful in abolishing the FEHBP, congressional and federal workers, plus millions of retirees and dependents, would be denied a system in which wide personal choice and intense competition have kept ave rage annual premium increases as much as one-half to one-third below increases in the private sector in recent years.[REF] And unlike those with private sector health plans, families with FEHBP plans enjoy benefits that are portable between jobs.

Rather than solving their ethical dilemma by abandoning the successful EHBP and forcing all Americans into an untested and questionable new national plan, lawmakers would be wiser to retain the FEHBP, improve it, and use its principles of consumer choice and competition as the basis for health care reform for all Americans. In other words, Members of Congress should guarantee to every American family the same kind of choices that they and other federal workers already enjoy Consumer Choice Plan. This could be done by instituting a reform based on the central elements of the Heritage Foundations Consumer Choice Health Plan and giving every American family direct control of their own money-including the money their employer now spends on their health insurance.[REF] Every American family would be em powered also by changes in the federal tax code and by a tax credit or a voucher (for low income families) to help offset the costs of purchasing health insurance, to pay routine out-of-pocket medical expenses, or to open up a tax-free medical savings account.[REF] Legislation based on the Heritage proposal S.3348) was introduced last year by Senator Orrin Hatch, the Utah Republican. A group of Senators and House members currently are developing a revised version for introduction this summer.

Such comprehensive changes would enable all American workers and their families to purchase the health insurance plans of their choice, including plans offered through unions or other employee organizations, just as Members of Congress and federal and postal workers do now. They could even obtain plan s sponsored by churches, the local farm bureau, or any other major organization. Moreover, federal tax relief for health insurance no longer would be tied exclusively to the place of work, as it is now, but would be available to. workers,regardless of where they worked or even their status of employment This would make health benefits both portable and secure. This change in the tax laws also would enable workers who retire to carry their health insurance plans directly into retirement, and thus enjoy the unique security and peace of mind now reserved to congressional and federal retirees.

BREAKING UP A GOOD THING IS HARD TO DO

If the FEHBP is abolished, federal workers will be forced to buy one of the standard ized health care plans offered by the Clinton Administration's proposed "regional health alliances new government-sponsored health care purchasing cooperatives to serve the self-employed, the unemployed, employees of small businesses, current Medicaid recipients, and the currently uninsured. These regional alliances are likely to be an even more highly regulated variant of the health insurance purchasing cooperatives (HIPCS) envisioned under the original "managed competition" reform model proposed by Professor Alain Enthoven, the Stanford University economist, Dr. Paul Ellwood of the so-called Jackson Hole Group, and Representative Jim Cooper, the Tennessee Democrat.[REF]

John Sturdivant, President of the American Federation of Government Employees AFGE), the largest federal union, worries that if the Clinton Administration exempts big private companies from participating in these pools as some officials hint, federal workers and their families then would be thrown into plans serving the most expensive patients, with consequently higher costs for federal families.[REF]

For federal workers and retirees and their families, the Clinton Administration's proposed abolition of the Federal Employee Health Benefits Program raises a number of specific concerns. Among them:

WORRY #l : A reduction in choice of benefits. Federal employees and retirees could not expect to have access to the same wide choice of health benefits packages, with vary ing premiums and deductibles, that they now enjoy. Almost 400 plans now compete to satisfy federal consumers, who normally choose between a dozen and two dozen plans in any given geographical area of the country. Instead their "choice" will be between 4 minor variations of a standard one-size-fits-all health benefits package. As Washington Post reporters Dana Priest and Stephen Barr note The standard package might include fewer or different benefits than some [federal] workers now receive, and the federal government might decide not to pay for supplementary coverage to close the gap."[REF]

This prospect of being forced to accept an unknown level of benefits and costs angers most federal union 'leaders. Says George Gould, Washington representative of the National Association of Letter Carriers "We all support the concept of national health care for people who don' t have health care coverage or can't afford it but we resent the presumption that we have to be drafted into a program when nobody knows how the hell it will work....Suppose someone went up to Congressman X and said, 'Lets put 300,000 of your 550,000 constituents in a system that we don't know what it will cost, don't know what benefits it will offer or what it is going to be'"[REF]

Rather than throwing all federal workers into the Clinton health plan, one prominent union official suggests an alternative--just throw Members of Congress and Clinton Administration political appointees into the Clinton plan, but leave the rest of federal workers and retirees alone. Says Ken Parmelee, Washington representative of the Rural Letter Carriers Association It makes sense for Members of Congress and political appointees, but not regular workers and retirees, to be part of a national plan."[REF] Notes Mike Causey, veteran reporter on civil service affairs for The Washington Post, there are approximately 37,000 elected and appointed officials in the federal government. This is just a small fraction of the nine-million-member enrollment of the Federal Employee Health Benefit Program.

But if any federal union leaders want to insulate themselves and federal workers from the health care system Congress imposes on private sector workers, then they should at least offer Membe rs of Congress, whom they are ready to consign to the new health care system, a compelling justification for the difference in treatment

WORRY #2: The elimination of employee-sponsored plans. Federal workers probably would lose the right to remain in plans offered by unions and various employee organizations. Such employee-sponsored plans are a characteristic feature of the FEHBP, and do not exist to a comparable degree anywhere else. Indeed, plans sponsored by unions and other employee organizations have been a feature of the FEHBP since its inception in 1959, and they now enroll over one-third of all federal workers, retirees, and dependents.

WORRY #3: Paying more and getting less. The most fundamental concern for federal families is financial: how the Clinton plan will affect the paychecks-the bottom line of federal workers and retirees. The key financial worries center on future costs and premiums of their health insurance. Other Americans also share these concerns.

According to Hillary Clinton, whose special task force has been hammering out the details of the Administrations plan, these concerns are misplaced. During a recent trip to Baltimore, Maryland, Mrs. Clinton said "I can guarantee you that an program the president proposes to you will cost you less than you are paying now."[REF]

Notwithstanding Mrs. Clintons promise to a small group of Baltimore businesspeople, federal union leaders wony that their members and retirees will end up paying more for health insurance, but getting less under the Clinton health plan: People with health insurance are going to end up paying more for less coverage, worries American Federation of Government Employees resident Sturdivant. "Thats what were concerned about with federal employees."[REF] Similarly, Robert Tobias, president of the National Treasury Employees Union, says, If the federal employee program is eliminated and they're rolled into the new federal healthcare plan, were concerned that they will receive less benefits and be paying more dollars in premiums."[REF]

Paying More for Less. Private sector unionized workers are beginning to echo those worries. Observes Representative Jim McDermott, the Washington State Democrat, If Im going out to my Boeing workers, who stood outside for 30 years to earn their benefit package, and tell them they're going to give up 20 percent of those benefits-and pay more in taxes, too-they're going to ask me to have my head examined.[REF] Indeed, recent surveys show that most Americans think that they will be paying more for less.[REF]

They are probably right. Under the emerging Clinton health plan, private sector employers likely will be required to pay a portion of their employees health care benefits; employees also would be required to pay some portion of the cost of their plans in the form of a payroll tax, as well as copayments and deductibles. In fact, a recent study by Lewin-VHI, a leading Virginia-based econometric firm specializing i n health care shows that about one-fourth of all households could end up paying at least $1,000 more each year for their health care than they do today.[REF] In the case of the FEHBP the federal government this year contributes up to $1,675 for individuals and $3,630 for federal families, approximately 72 percent of the premium cost for congressional and federal workers If the rules in a new system based on the Clinton proposal were to be the same for the federal government as they are expected to be for employers in the private sector-and if private employer contributions are lower than the current federal contribution-then the federal government likely would lower its contribution to premiums.[REF] The only other option for Members of Congress would be to set up one set of rules for..employers and employees..in the private sector and another, far more generous, set of rules for themselves and federal workers and retirees-an option which would generate intense public opposition

THE GREAT ESCAPE FOR FEDERAL UNIONS?

Federal union leaders use various arguments to justify their demands for a special dispensation from the Clinton Administration's evolving national health plan.

One such argument is that the federal government is like a big corporation, and the Clinton Administration has already indicated a willingness to consider exempting large self-insured companies from participating in its regional alliances.[REF] Approximately 97 percent of all companies with 5,000 or more employees are self-insured.[REF] Self-insurance means a company directly assumes all the risks and the financial liabilities of its employees' health plans. Under current laws, this gives a company an exemption from state laws mandating certain health benefits. If large, self-insured companies were exempt from key provisions of the Clinton plan, they might not have to pay a full payroll tax. They would become, in practice, their own health regional alliance, offering their own plans to their employees. If big businesses can be exempted from the Clinton health plan, union leaders argue, then so should the federal government. If the Clinton Administration exempts these corporations from participating in the regional alliances, a different set of benefit and tax rules is likely to apply to them.

This would create a two-tiered health care system-one for most large corporations and their employees, and another for small businesses and their workers.

One key difference between many large corporations and the federal government toda y is that the federal government is not self-insured. And if the federal government were to self-insure, it would not be for the same reason that large private sector companies self-insure-the state taxation and regulation of their health insurance plans , particularly the imposition of mandated benefits. But Congress already protects FEHBP plans from state-mandated benefits and their attendant costs. They have also protected competing FEHBP plans from state taxes on their premiums.[REF]

Members of Congress also know there is an enormous difference between self-insurance for private companies and for the federal government If private companies self-in sure and assume the financial risks of health insurance, and then have grave difficulties meeting their financial obligations in paying their employee s health care costs, the dam age is limited to the bottom line of the company, its stockholders, its managers, and its employees. But if the federal government were to self-insure, all of the financial obligations of health insurance of federal,.employees simply.would--be shifted to the taxpayer Thus, treating the federal government like a self-insured corporation under the Clinton plan would exonerate private insurance carriers in the FEHBP from all financial risks they now assume, and instead saddle Americas taxpayers with another increase in the unfunded liabilities that already burden other federal entitlement programs.[REF]

THREE DECADES OF SUCCESS

It is perfectly understandable why federal employees and their organizations oppose the abolition of their health care program. It works.

The FEHBP is the program of Presidents, Supreme Court Justices, the FBI and the CIA, biomedical research scientists at the National Institutes of Health and astrophysicists at the National Aeronautics and Space Administration. But it is also the program of. Capitol Hill cops and maintenance workers, mechanics and technicians postal workers and Capitol Hill couriers.

It also is open to all Members of Congress and thousands of congressional staff, including the congressional staff members who worked on Hillary Clintons Health Care Reform Task Force. Altogether 37,000 congressional and political employees are covered under the FEHBP, and about one-half of all residents of the Washington, D.C metropolitan area are enrolled in one of its 35 competing health care plans.[REF] Official Washington from the First Family to the animal cage cleaners at the National Zoo, is covered under this unique health care program.

After Congress enacted the Federal Employee Health Benefits Program in 1959, President John F. Kennedy enrolled in it and chose the Aetna health plan for himself and his young family; President Lyndon B. Johnson took his Blue Cross and Blue Shield plan into retirement.[REF] Those coming into government are often as delighted with the program as those going out of government. During the 1992 Clinton presidential transition and congressional orientation, many of the new political appointees of the Clinton Administration and Members of Congress were introduced to the FEHBP for the first time and The FEHBP covers millions of federal employees and retirees in the executive branch 8 were pleasantly surprised at the choice of benefits they now have. At least two Cabinet officers have requested and gotten briefings on health insurance benefit s because of special medical problems in their families, reports the Washington Posts' Mike Causey. "Most are delighted at the relatively low group-rate premiums 700 to $4,500 a year for family coverage, half that for singles and the fact that pre-existing medical conditions are fully and instantly covered."[REF] Causey adds that, Most presidents, past and current Members of Congress staff members and Cabinet officers sign-up as soon as they can. It is one of the least advertised, best perks of office, especially for retirees.[REF]

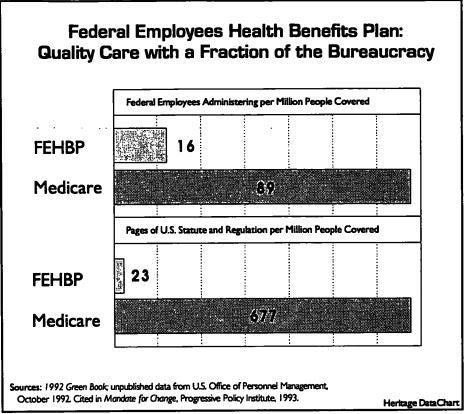

Cost Control. It is ironic that the Clinton Administration is targeting for oblivion the one government health care program that works well in controlling costs and simultaneously gives millions of American families a solid range of benefit choices. Since 1975 the average annual premium increase in the FEHBP has been about 10 percent.[REF] Leading independent studies, such as those conducted by the Congressional Research Service and Lewin-VHI, show that average annual premium increases over the past twelve years are two to three and one-half percentage points less than those in private, employer-based insurance.[REF] As Dana Priest and Stephen Barr of The Washington Post note FEHBP is one of only a handful of national health benefits programs in which costs apparently have grown less rapidly than in private sector plans.[REF]

This cost control is all the more remarkable, given that the federal program, unlike many private or corporate health plans, is open to all retirees. Retirees are much more costly on average to insure than active workers, and many federal retirees are not eligible for Medicare. Moreover, the FEHBPs comparative superior cost-control performance is even more noteworthy because private sector health plans in recent years have been moving away from first dollar coverage, shaving benefits, increasing employees share of premiums, or a combination of both, and cutting back on coverage for dependents and retiree.[REF] Retirees, especially, have been hit hard by private sector health insurance cutbacks.[REF] While private sector plans have been retreating from first dollar coverage and in creasing the size and number of deductibles and copayments, federal benefit packages in recent years actually have been getting progressively more generous.[REF] So, federal union leaders, employees and retirees are right to be nervous about the critical details of the Clinton healthcare.

The reason the FEHBP, unlike other government health programs, keeps cost increases in check is because market forces rather than regulation are the primary tool for cost control in the FEHBP. Says Walton Francis, a Washington based economist 'The Paradox of the program is that it is successful because it is relatively unmanaged.[REF] The FEHBP consequently is burdened by both fewer bureaucrats and less red tape.Federal employees enjoy a far wider degree of personal choice in health care than most other Americans. Unlike most private employer-based insurance, and all other governmental health care programs, individual consumers not employers or government officials, make key personal decisions about price and benefits in their plans. Insurance companies have to compete by satisfying these federal consumers directly in order to keep their business

A WORKING MODEL FOR REFORM

Uniquely based on the twin principles of consumer choice and competition, the FEHBP is broadly similar to the kind of health care system embodied in the Heritage Foundation Consumer Choice Health Plan. If all Americans had the same opportunities to make choices in health care that are practically denied them now, they and their families would enjoy many of the same benefits now reserved to Members of Congress, congressional staff, and federal workers as special privileges. Among them:

A wide choice of plans. All over America, Members of Congress and federal workers can choose between a dozen and two dozen plans, f r om traditional fee for-service options to Health Maintenance Organizations (HMOs) and other man 36 Ibid emphasis in the original. aged care programs. Uniquely, federal consumers can even choose union plans and plans sponsored by organizations that represent federal employees in other ways. And unlike workers in the private sector, they are not tied to an employer's narrow set of health care options-if the employer offers any options at all. If federal workers do not like the annual performance of their health plan, they can simply change it the following year.

Likewise, under the Heritage Consumer Choice Health Plan, every American family, armed with tax credits or vouchers, could pick from a wide variety of plans, including plans sponsored by unions, employee organizations, trade and professional associations and even churches, fraternal, and religious organizations. Right now for example, farm bureaus offer health insurance plans in rural areas, but tax relief for these plans is not available unless they are offered to farmworkers through the place of work. So, many lower-paid far m workers without company plans cannot afford these plans. But under the Heritage proposal, workers would receive tax credits or vouchers to enable them to afford at least the basic plan of their choice

Portability. Federal workers do not have to worry about losing coverage when they change federal jobs. They simply keep the same plan. It belongs directly to them. congressional and federal workers do not have to worry about carrying their health insurance into retirement because they 'own" the plan. Unlike private sector workers who often worry about losing their insurance when they retire, or facing arbitrary benefit cuts by their former employers, retiring federal workers can enjoy peace of mind.

Likewise, under the Heritage Foundation Consumer Choice Health Plan, there is not only portability in health insurance for active workers, who can change jobs without losing their health insurance plan, but also portability into retirement. Under the Heritage proposal, there would be no obstacle to a worker taking his or her health insurance plan into retirement, or choosing to keep it at age 65, paid in part with a voucher from the Medicare program, rather than being forced to enroll in Medicare.[REF]

A wide range of benefits. Members of Congress and federal workers can pick from a wide range of benefit packages, benefits and prices to fit a family's wants or needs. Responding to strong market demand, virtually all plans competing in the FEHBP now offer catastrophic coverage. Some plans offer excellent dental benefits for young children. Other emphasize prescription drug coverage. Some plans, the most expensive, offer generous mental health benefits.

Many organizations keep premium prices low by incorporating managed care options with traditional fee-for-service medicine. Significantly, managed care options voluntarily chosen by federal families as good value for money, are far more prevalent in the FEHBP than in government or private sector programs.[REF]

Example: The 1993 plan offered by the Beneficial Association of Capitol Employ ees (BACE) serves Members of Congress and legislative staff exclusively. It is, as one might expect, one of the best health care options available in the federal market. For individual Members of Congress or congressional staffers, the monthly premium cost of the BACE plan is $43.57, with the federal government picking up the remaining $130.70. For family coverage, the monthly premium cost is $109.93, with the government contributing $302.47. For the same premium rates, the BACE plan offers Members of Congress and congressional staff an option of participating in either a preferred provider organization (PPO) or a more traditional health insurance plan. Aside from catastrophic coverage, the traditional BACE option offers Congressmen and staffers 100 percent coverage for hospitalization and outpatient surgery, plus routine physical examinations, well child care, dental benefits, and even home health and hospice care. The BACE PPO option offers Members and staffers health care services without deductibles or coinsurance, including 100 percent coverage for hospitalization, surgery, and routine medical care. Out-of-pocket costs are limited to a $5 copayment to the primary care physician, a $10 copayment for the specialist, and a $25 for allergy testing and emergency care. Like the Postmasters Plan and the American Postal Workers Union plan, the BACE plan offers a mail order prescription drug service.

Example: The 1993 Postmasters Benefit Plan, run by the National League of Postmasters, offers self and family coverage, including standard option and high option benefit packages. The Postmasters plan features not only 100 percent coverage for accidental injury and catastrophic illness, along with its hospitalization and physician services, but also quick and efficient claims processing, coverage for routine annual physicals, and a mail order prescription drug program, as well as "wellness" benefits for both active and retired employees and their families.

Given the wide range of options, plus the wide variety of prices, deductibles, and copayments, congressional and federal employees now enjoy a range of choice in health care practically denied every other American. Likewise, under the Heritage Consumer Choice Health Plan, every American would be able to choose the health care plan best suited to meet his family needs-from any licensed source. Thus, consumer choice would directly promote a range of health care benefits even broader than that now found in the FEHBP.

Strong Competition. In the FEHBP, congressional and federal employees exercise a degree of economic control that is practically denied most other Americans. So insurance companies, including the largest insurers, must work for and satisfy federal employees and their families--not just the employer--to continue in business.

Likewise, under the Heritage Consumer Choice Health Plan, while basic groundrules for protecting consumers would be established and enforced, consumer choice and competitive innovation among insurance carriers in the delivery of care 12 would be rewarded in an open market. Doctors, hospitals, group practices, and clinics, as well as the underlying insurers, would be forced in the market to deliver quality care as efficiently as possible.

Consumer Information. Members of Congress and federal workers are not left alone in a bewildering and confusing health care market, but are given solid, her-friendly in format from agencies and private .organizations on the options available to them. Federal consumers generally are more knowledgeable about the details of their health insurance than their private sector counterparts. The reason: they are the key decision-makers and their demand for information has created a whole private information industry. Booklets and consumer guides complement seminars, congressionally sponsored "health fairs," newspaper columns, and television an d radio advertising to a degree that is unknown in private employer-based systems.

Likewise, under the Heritage Consumer Choice Health Care Plan, all Americans would be able to take advantage of the same kind of information made available to Members of Congress and federal workers, and so new sources of information and advice would flourish. Moreover, health care plans, doctors, and hospitals would want to advertise their success in treating and curing various kinds of illness, and solid empirical evidence indicating performance would be in strong demand. Already, U.S. News and World Report, in conjunction with the National Opinion Re search Center, a social science research group based in Chicago, Illinois, using new methods to quantify and assess hospital performance objectively, has completed a comprehensive assessment of hospital performance, "something no government agency or research group has done before on a nationwide basis."[REF] The problem for most Americans today is that they cannot take full advantage of such information be cause their choice of health plans-if ky-is so limited. In a highly competitive open market, in which consumers can pick the best value for their money, there would always be a premium on such solid and readable health-related information.

Payroll Deductions. Members of Congress and federal workers do not wrestle with administration in the payment of health care premiums. After they pick the plan of their choice, the clerk of the House or Senate or their employing agency simply makes a payroll deduction, which is processed by the Treasury Department and transmitted to the carrier.

Likewise, under the Heritage Consumer Choice Health Plan, private employers would be subject to a simple requirement: make a payroll deduction for the premium from the employees paycheck, adding in the federal tax credit available to the employee and his family, and transmit it to the plan of the employee's choice

Financial Help. Members of Congress and all federal workers also get some financial help from the federal government in the purchase of their insurance. The government makes a contribution up to a certain dollar amount, an average of a little more than 70 percent of the premium. In effect, congressional and federal workers are the unique beneficiaries of a voucher system for health care. But because they make the decision whether their plan is a rich plan or a lean plan, a traditional indemnity-plan or an HMO, these consumers pocket the savings and thus are very sensitive to price. Unlike so many private sector workers, they tend to be cost-conscious.

The Heritage proposal would change the law to give employees directly the finances they need to obtain a plan. First, at the direction of its employees, firms would have to cash out the value of the current plan and give the money to the employee. This also makes employees realize that the employer contribution is, in fact , the workers money. Second, the Heritage proposal would change the federal tax code so that all Americans would be given tax relief in the form of tax credits or vouchers, regardless of their place of employment. With this money, they could then select the best plan for themselves and their families. But changing the tax code would also make private sector workers more cost-conscious. They, too, would at tempt to get the best value for their money and pocket the savings directly.

Insurance Reforms. Member s of Congress and federal consumers enjoy the benefits of certain insurance practices that are designed to make the health care system work better. They are not blocked from enrollment in a health plan because of pre-existing medical conditions and they d o not have to endure a waiting period to enroll in the plan of their choice. Moreover, they can renew their insurance plan each year, with no questions asked. Nor can they be dropped from coverage by their insurance company simply because they or a member of their family gets sick.

Likewise, the Heritage.Foundation Consumer Choice Plan also provides for changes in health insurance underwriting practices to guarantee consumers greater peace of mind. These include new rules to stop insurance companies from forcing sick people to drop their coverage and guaranteeing individuals and families the right to renew coverage at the average premium increase for all those enrolled with an insurer.[REF]

CREATING A FAIR AND COMPREHENSIVE REFORM

In the sensitive area of national health care reform, Members of Congress are faced with some tough political and personal decisions. These decisions will affect every American in a very personal way. Families will not welcome a decision to create a large, impersonal bureaucratic system, replete with big tax increases, national health boards global budgets, price.controls, or.endless rules and regulations governing every facet of the delivery of medical services. In addition, Congress will retain public support for change only if lawmakers are fair to federal workers and retirees and military families, as well as to taxpayers and workers in the private sector. This leaves them some clear policy options

1) Members of Congress should retain the FEHBP and strengthen its market features.

Close examination of the FEHBP indicates that virtually all its imperfections stem precisely from government policies that inhibit the full functioning of free market forces. As economist Walton Francis argues, It is noteworthy that the FEHBPs greatest failures have tended to arise in areas where the program is constrained by law.[REF] This includes the Office of Personnel Managements (OPM) unnecessary meddling in the details of rates and benefits, and congressional insistence on retaining insurance underwriting practices that aggravate the programs problem of "adverse selection."[REF]

Instead OPM should simply enforce basic groundrules for insurance and consumer protection. If it did so, the variety of health care options would be even richer, the competition among private plans keener, and the cost savings to federal workers and taxpayers even greater. The strong basic framework of consumer choice and competition has made FEHBP a solid system, and it has been functioning well for over three decades.[REF] It should not be abandoned. It should be improved by increasing, not decreasing, the role of free market forces

2) Congress should create a consumer choice system for all Americans.

Instead of dissolving the FEHBP, as the Clinton Administration threatens to do, or choking it with the kind of regulations and paperwork that burden Medicare,[REF] Congress should rebuild the American health c a re system on the programs principles of consumer choice and competition. It can do so by making the federal tax and insurance market changes embodied in the Heritage Foundations Consumer Choice Health Plan.

3) Congress should let military families join the FEHBP.

While Members of Congress are debating comprehensive health care reform for the rest of the nation, they could, in the interim, allow military families int o their own health care system. Currently military families and the dependents of servicemen and -women are covered by CHAMPUS, a government health insurance system. If Congress would allow military families to join the FEHBP as these families want, they could do so on the same terms as congressional and federal employees. No special treatment is necessary. This not only means that military families would generally have the same range of choices as Members of Congress and federal workers and their families, but also that military associations, just like federal employee organizations, could sponsor health insurance plans for their members and others. For example, the American Postal Workers Union Plan and the Mail Handlers Plan could compete with plans sponsored by military or fraternal organizations.

As consumers, military families would get to know the value of their health benefits package and pocket any savings from paying directly for those services. They would also enjoy the security of knowing that they could not be dropped from coverage. Says the National Military Families Association executive director, Dorsey Chescavage, It would probably cost a little more, but in return for paying more you would have security and choice, no more space available, care and people over 65 would not be dumped"[REF]

Aside from the personal benefits of consumer choice and competition for military spouses and children and retirees, enrolling these families in the FEHBP would also be a boon for federal taxpayers. According to a preliminary study for the United States De partment of Defense, conducted by Birch and Davis Associates, a consulting firm based in Silver Spring, Maryland, the enrollment of military dependents in the FEHBP would save American taxpayers 435 in health care costs per military family each year.[REF]

If Members of Congress sincerely want to help military wives and children gain access to a better health care system, they can open up their own system to these families on the same basis as other congressional a n d federal employees

CONCLUSION If Members of Congress enact a comprehensive reform of the health care system, fairness dictates that the same rules and regulations they impose on workers in the private sector must apply with equal force to themselves and workers in the public sector. Members of Congress must not set up a system of special exclusions from the Clinton Administration health plan for big business, for federal workers or postal workers, or for them selves If Congress insists on restricting choices and imposing new regulations and taxes in the new system, all current beneficiaries should be subjected to exactly the same rules and regulations, without exception. If Americans cannot have the benefits of consumer choice in a free market, then neither should Members of Congress and federal workers

But instead of abolishing the FEHBP and joining other Americans in an untested new system, Congress should instead build upon the principles underlying the successful FEHBP, particularly consumer choice and competition, and extend the benefits of such a system to the entire American population This could be done by adopting the Heritage Consumer Choice Health Plan.

Time to Share. The best public policy was articulated by Kay Bailey Hutchison, the new Texas Republican Senator, in her second state-wide debate with then-Senator Robert Krueger, the Texas Democrat:

The difference between us is, you don't want to give everybody in America what you have as a Member of Congress. You h ave exactly the choice I am trying to give everyone You choose the one plan that is best for your family. You get the tax credit and you are able to spend the money the way you want to. I want everyone to have the choice that Bob Krueger now has.[REF]

In the upcoming debate on health care, Congress has the chance to share the best features of its own health system with the rest of America.

Robert E. Moffit, Ph.D

Deputy Director of Domestic Policy Studies