My name is David R. Burton. I am Senior Fellow in Economic Policy at The Heritage Foundation. I would like to express my thanks to Chairman Chabot, Ranking Member Velázquez, and members of the committee for the opportunity to be here this morning. The views I express in this testimony are my own, and should not be construed as representing any official position of The Heritage Foundation.

Entrepreneurship matters. It fosters discovery, innovation and job creation. It leads to more productive production processes that improve productivity and real wages. Entrepreneurs develop new and less expensive products that improve consumer well- being. They make markets more efficient. New firms account for most of the net job creation in the United States. Moreover, the vast majority of economic gains from innovation and entrepreneurship accrue to the public at large, rather than entrepreneurs.

Entrepreneurship is in decline. The rate of new business formation has seriously declined and barely exceeds business exits. Many other indicia of entrepreneurial health also indicate that the United States has placed an unprecedented burden on small and start-up businesses. Accordingly, job creation, productivity improvements and welfare-enhancing innovation have slowed.

Although there are many reasons that entrepreneurs are struggling, the tax system is a major contributing factor. This is both because of the direct impact of the tax system on small and start-up firms and because of its adverse impact on the economy overall. The current tax system reduces the incentives to work, save and invest. It raises the cost of capital and reduces access to capital. It imposes high taxes on risk taking, harms the international competitiveness of U.S. businesses and impedes economic growth. Moreover, the tax system is monstrously complex, imposing inordinately high compliance costs on small and start-up firms.

Entrepreneurship Matters

Entrepreneurship matters.1 It fosters discovery and innovation.2 Entrepreneurs also engage in the creative destruction of existing technologies, economic institutions and business production or management techniques by replacing them with new and better ones.3 Entrepreneurs bear a high degree of uncertainty and are the source of much of the

dynamism in our economy.4 New, start-up businesses account for most of the net job creation in the economy.5 Entrepreneurs innovate, providing consumers with new or better products. They provide other businesses with innovative, lower cost production methods and are, therefore, one of the key factors in productivity improvement and real income growth.6 In terms of the neo-classical growth model, entrepreneurship is an important factor affecting the rate of technological change and the marginal productivity of capital.7 The vast majority of economic gains from innovation and entrepreneurship accrue to the public at large, rather than entrepreneurs.8 Entrepreneurs are central to the dynamism, creativity and flexibility that enables market economies to consistently grow, adapt successfully to changing circumstances and create sustained prosperity.9

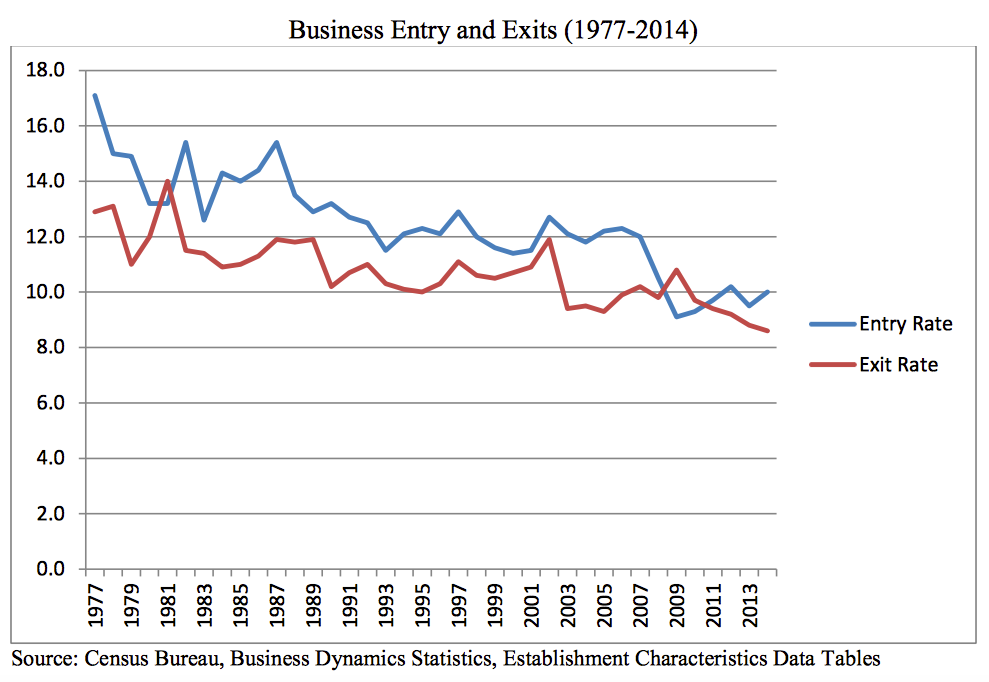

Entrepreneurship is in Decline

Entrepreneurship is in decline. As the chart below illustrates, the business entry (or formation) rate has been steadily declining since 1977 but the business entry rate dropped very steeply in 2008 and has barely recovered.10 While the business entry rate now exceeds the business exit rate, by historical standards the net business formation rate is very anemic.

The share of firms aged 16 years or more has increased by 50 percent over the last two decades.11 High-Tech companies are shedding more jobs than they are creating.12 Although recovering with the substantial increase in equity market values over the past several years and the regulatory improvements in the 2012 JOBS Act “IPO On-Ramp” provisions,”13 Initial Public Offerings (IPOS) remain substantially below the previous two decades.14 Although there is improvement since the depths of the recession, small and start-up businesses continue to struggle.15 The decline in entrepreneurship is one of the key factors causing anemic U.S. economic performance.

Helping to Restore Prosperity by Removing Impediments to Entrepreneurship

There are multiple reasons for the decline in entrepreneurial activity.16 The key to reversing the decline in entrepreneurship is to systematically reduce the legal impediments to entrepreneurship. There is not any one policy change – or even a few – that will lead to a sudden renaissance in entrepreneurship. Since the decline is caused by the combined weight of many poor public policies, the solution requires systematically improving public policy in a wide variety of areas. It is clear, however, that the tax system is a leading reason for the poor economic performance of recent years and that tax reform offers a means of substantially improving the economy, increasing wages and giving rise to a renaissance in entrepreneurship.

The remainder of my testimony examines the sources of complexity in the tax code and its economic effects more generally. It then discusses proposed improvements to the tax system. My discussion of proposed reforms is divided into two parts. The first section discusses reforms to the existing tax system that will aid entrepreneurship. The second section addresses more major or fundamental tax reform.

Sources of Complexity in the Tax Code

The compliance costs17 associated with the income tax have been estimated to be in the range of $67 billion to $410 billion.18 The higher estimate, which is quite plausible given its derivation, is 2.2 percent of Gross Domestic Product (GDP) and about 12 percent of federal receipts. These high compliance costs have a disproportionately adverse impact on small and start-up businesses. Compliance costs do not increase linearly with size.

Among the four largest sources of complexity in the tax law are (1) the capital cost recovery system; (2) inventory accounting; (3) employee benefit taxation, particularly the retirement savings (qualified account) rules; and (4) international taxation.

Under current law, there are generally five different capital cost recovery or depreciation systems with which businesses must contend. They are: (1) the Modified Accelerated Cost Recovery System (MACRS) using the General Depreciation System (GDS);19 (2) the Modified Accelerated Cost Recovery System (MACRS) using the Alternative Depreciation System (ADS);20 (3) the depreciation rules under the alternative minimum tax (AMT);21 (4) the depreciation rules applicable for determining earnings and profits22 and (5) expensing.23 As discussed below, for economic and administrative reasons, capital expenses should simply be deducted in the year incurred (i.e. expensed).

Inventory accounting also introduces a high degree of complexity.24 The Internal Revenue Code section 263A uniform capitalization rules are especially complex. Firms with gross receipts under $10 million annually are allowed to use less complex rules. But for any size firm that maintains inventory, these rules are a major burden.

The taxation of employee benefits is a major source of complexity. The tax treatment of qualified plans is absurdly complex. But the rules governing health insurance, FSAs, HSAs, tuition assistance, life and dental insurance and a host of other matters introduce complexity and costs.

And for firms that operate internationally, the income souring and expense allocation rules, the intercompany pricing rules, the foreign tax credit rules (especially the separate basket limitations), the controlled foreign corporation rules and subpart F, the export sourcing rule and many other provisions introduce a very high degree of complexity.

The incremental reforms outlined below address all of these sources of complexity except the international tax provisions. Major tax reform would address all of them.

Primary Impediments to Economic Growth in the Tax Code

The current U.S. tax system has a very substantial negative impact on the economy. It has high marginal tax rates that reduce the incentive to work, save and invest. The U.S., for example, has the highest corporate tax rate in the industrialized world. It substantially raises the cost of capital by double, treble or even quadruple taxing savings and investment. It place U.S. businesses and at competitive disadvantage in international markets. It is riddled with special tax preferences. And it imposes large compliance costs on U.S. businesses, which has a disproportionately negative impact on small firms.

The solution is to reduce marginal tax rates, particularly on businesses, to expense

capital, to eliminate true tax preferences and to simplify the tax system.25 Major tax reform along these lines can be expected to increase GDP by about 10 percent over 10 years. Truly fundamental tax reform would increase GDP by about 15 percent over 10 years.

Incremental Reforms to the Current Tax System

Incremental improvements to the current tax system that Congress should consider are outlined below.

- Expensing of Investment in Machinery and Equipment. Amend Internal Revenue Code §179 to permanently allow annual capital expenses of up to $1 million to be deducted when incurred. Expensing would simplify small firms’ tax returns, reduce compliance costs, reduce small firms’ cost of capital and aid cash flow.26

- Retirement Account Simplification. Very few small employers offer retirement accounts because of the complexity, high compliance costs and regulatory risk of doing so.27 This makes it more difficult for them to attract employees and more difficult for both the small business owners and their employees to save for retirement. This is one of the most complex areas of the tax law and desperately in need of simplification.28 One possible solution would be to amend the Internal Revenue Code to create a Small Business Uniform Retirement Account as a voluntary alternative for employers with 500 or fewer employees to replace: (1) simplified employee pensions (SEPs), (2) salary reduction simplified employee pensions, (3) SIMPLE IRA plans, (4) SIMPLE 401(k) plans, (5) Keogh plans, (6) regular 401(k)s (with respect to employers with 500 or fewer employees), (7) profit-sharing plans (with respect to employers with 500 or fewer employees), (8) money purchase pension plan (with respect to employers with 500 or fewer employees), and (9) employee stock ownership plans (with respect to employers with 500 or fewer employees). The Small Business Uniform Retirement Account would (1) have check the box eligibility, (2) uniform employee eligibility, (3) automatic enrollment of employees with an option to opt-out, (4) no non-discrimination, coverage or key employee rules, (5) allow contribution levels to be chosen by the employee, (6) be maintained through a financial institution and (7) be available to employees and self-employed persons (including partners and LLC members).

- Reduce the Top Long-term Capital Gains Tax Rate to 20 percent or Less. Evidence shows that a capital gains rate much above 20 percent actually reduces federal revenues. In addition, a high capital gains tax rate reduces the willingness of investors to invest in relatively risky start-up and growth companies and impedes capital formation. The top long-term capital gains tax rate should not exceed 20 percent (including the Obamacare investment income tax).29

- Permit Cash Method Accounting for Firms with up to $10 million in Gross Receipts. Cash method accounting is simpler and aids cash flow.30

- S Corporation Liberalization. Permit S corporations to have more than one class of stock, non-resident alien shareholders (subject to 30 percent withholding on dividends) and more than 100 shareholders. The latter is particularly important if S corporations are going to have practical access to the crowdfunding or Regulation A+ provisions in the JOBS Act which allows companies to raise small amounts from a large number of investors using provision enacted by the JOBS Act.31 It is preferably for the S corporation rules to emulate the partnership rules so there would be no shareholder limit but S corporation status would not be available to publicly traded corporations. See Internal Revenue Code §7704.

- Repeal the Obamacare Health Insurance Tax. Obamacare imposes an excise tax on health insurance premiums that effectively is aimed at small businesses because larger firms self-insure (with or without stop-loss insurance) and therefore do not pay health insurance premiums. It is roughly equivalent to a 2.5 percent tax. This tax should be repealed.32

- Reduce the Tax Rate of Pass-Through Entity income to the Corporate Tax Rate. Reduce the tax rate paid on income from S corporations and other pass-through entities (e.g. LLCs) to no more than the top corporate tax rate (currently 35 percent). Ideally, however, the tax rate on pass-through entity income and other income would be both low and the same. Otherwise, Congress must draft rules distinguishing between pass-through entity income, on the one hand, and labor and portfolio investment income on the other. Such rules will inevitably lead to complexity.

- Increase the Incentive Stock Option (ISO) Cap Limitation from $100,000 to $250,000. Internal Revenue Code section 422(d) limits incentive stock options to $100,000 in aggregate stock value (not gain). This limits the utility of ISOs as a means to attract talent.

- Full Deductibility for Health Insurance Purchased by the Self-Employed. Currently, health insurance costs incurred by the self-employed (which includes partners and LLC members) are deductible for income tax purposes but not for purposes of the 15.3 percent self-employment tax. This creates a special tax burden on the self-employed not borne by anyone else in the economy. There should be parity for the self-employed with those who are employed. Internal Revenue Code §162(l)(4) should be repealed.

- Clarify Rules Governing to What Extent Distributions from Pass-Through Entities are Subject to Payroll Taxes. This issue has existed since at least the 1980s and it has never been adequately resolved. It causes a lot of audits and a lot of uncertainty. Reasonable, clear and uniform rules governing “reasonable compensation” and investment income should be adopted for partnerships, S corporations and C corporations.

- Clarify Employee/Independent Contractor Rules. This issue has existed since at least the 1970s and it has never been adequately resolved. Current law involves evaluating 20 factors and any test with 20 factors is inherently ambiguous and will be arbitrary in application.33 The current state of the law causes a lot of audits and a lot of uncertainty. Provisions should be adopted providing bright line tests for determining who is definitely an employee and who is definitely a contractor and allowing the employer to choose whether a payee is an employee or a contractor in ambiguous cases, subject to 1099 reporting and moderate backup withholding if contractor status is elected.34

- Estate and Gift Tax Reduction. The unified credit should be increased so that $10 million is effectively excluded from the estate and gift tax. For 2017, the amount that is effectively excluded is $5.5 million. Family farms and businesses should not either have to be sold to pay estate taxes when parents die or incur huge life insurance premiums to provide the means of paying the tax.35 Ideally, of course, the estate and gift tax should be repealed entirely.

Major Tax Reform

Fundamental tax reform would reduce compliance costs considerably and result in dramatically higher rates of capital formation, economic growth and job creation. The goal of fundamental tax reform is a simple, flat rate, territorial consumption tax to replace the individual and corporate income tax and the estate and gift tax. This can take one of four forms. (1) A Hall-Rabushka-Armey-Forbes flat tax, (2) A consumed income tax (also known as an expenditure tax, cash-flow tax, inflow-outflow tax or the new flat tax), (3) a national sales tax or (4) a Business Transfer Tax (BTT) (also known as a business flat tax, business consumption tax or business activity tax) or, potentially, some combination of these.36 Major tax reform is a major step towards fundamental tax reform and would therefore reduce compliance costs considerably and result in higher rates of capital formation, economic growth and job creation.

Under the leadership of House Speaker Paul Ryan (R–WI) and House Ways and Means Committee Chairman Kevin Brady (R–TX), House Republicans released a blueprint for their tax reform initiative in June 2016.37 Since that time, the Ways and Means Committee has been drafting legislation and working toward a consensus among Republicans on the committee. This plan is certainly major tax reform and would have a substantial positive impact on the economy and entrepreneurs.

The Ryan–Brady “Better Way” blueprint would provide the lowest marginal tax rates since the 1920s, and expense machinery, equipment and structures. The top individual tax rate would be 33 percent (compared to 43.4 percent today); the top tax rate on C corporations would be 20 percent (compared to 35 percent today); and the top tax rate on pass-through businesses would be 25 percent (compared to 43.4 percent today). Many other changes would be made. It would have a dramatic positive economic impact. The Tax Foundation estimates it would increase GDP by 9.1 percent over 10 years, and reduce revenues by $191 billion over 10 years.38 The federal government is expected to raise $43 trillion in tax revenue over the next 10 years.39 Thus, the Brady plan is projected to reduce revenues by less than one-half of one percent.

This plan is most succinctly understood as a graduated rate version of the Hall– Rabushka flat tax.40 The two primary differences between the Better Way plan and the traditional Hall–Rabushka flat tax are that the Better Way plan has a border-tax adjustment and, instead of taxing only wages at the individual level, it has an additional tax on dividends, interest, and capital gains at half the statutory rate. It is therefore a very large step toward the right tax base with much lower marginal tax rates than those of the current system.

It would aid small businesses for two reasons. First, it would result in a much stronger economy. Second, it would reduce the burden of the tax system on entrepreneurs. Corporate and pass-through tax rates would decline sharply. All capital and inventory acquisition expenses would be immediately deductible. Capital gains tax rates would fall to 16.5 percent or less, depending on the tax bracket. It would substantially simplify the tax system. Thus, small and start-up firms can expect to see their marginal tax rates decline and their cost of capital decline. They will incur lower compliance costs. And their investors will pay lower marginal tax rates as well.

Thank you.

ENDNOTES:

1 For an introduction to the literature, see Paul Westhead and Mike Wright, Entrepreneurship: A Very Short Introduction (Oxford University Press: 2013).

2 Israel M. Kirzner, Competition and Entrepreneurship (University Of Chicago Press: 1973); Israel M. Kirzner, “Entrepreneurial Discovery and the Competitive Market Process: An Austrian Approach,” Journal of Economic Literature, Vol. 35, No. 1 (1997); Randall Holcombe, Entrepreneurship and Economic Progress (Routledge: 2006); William J. Baumol, The Microtheory of Innovative Entrepreneurship (Princeton University Press: 2010).

3 See, e.g., Joseph Schumpeter, Capitalism, Socialism, and Democracy (1942), pp. 81-86 http://digamo.free.fr/capisoc.pdf; W. Michael Cox and Richard Alm, "Creative Destruction," Concise Encyclopedia of Economics (Liberty Fund: 2007) http://www.econlib.org/library/Enc/CreativeDestruction.html; Henry G. Manne, “The Entrepreneur in the Large Corporation,” in The Collected Works of Henry G. Manne, Vol. 2 (Liberty Fund: 1996).

4 Frank H. Knight, Risk, Uncertainty, and Profit (1921) http://www.econlib.org/library/Knight/knRUP.html.

5 Magnus Henrekson and Dan Johansson, “Gazelles as Job Creators: A Survey and Interpretation of the Evidence,” Small Business Economics, Vol. 35 (2010), pp. 227–244 http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1092938; Ryan Decker, John Haltiwanger, Ron Jarmin, and Javier Miranda, "The Role of Entrepreneurship in US Job Creation and Economic Dynamism," Journal of Economic Perspectives, Vol. 28, No. 3 (Summer 2014), pp. 3–24 http://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.28.3.3; Salim Furth, "Research Review: Who Creates Jobs? Start-up Firms and New Businesses," Heritage Foundation Issue Brief #3891, April 4, 2013 http://www.heritage.org/research/reports/2013/04/who-creates-jobs-startup-firms-and-new-businesses.

6 Ralph Landau, “Technology and Capital Formation,” in Technology and Capital Formation, Dale W. Jorgenson and Ralph Landau, editors (MIT Press, 1989).

7 See, e.g., Robert M. Solow, Growth Theory: An Exposition (Oxford, 2000). Legal institutions, human capital and other factors are also important determinants of economic growth. See N. Gregory Mankiw, David Romer and David N. Weil, "A Contribution to the Empirics of Economic Growth," The Quarterly Journal of Economics, Vol. 107, No. 2 (May, 1992), pp. 407-437 http://www.fordham.edu/economics/mcleod/mankiw-romer-weil-a-contribution.pdf; Robert J. Barro, Economic Growth (MIT Press: 2nd edition, 2003).

8 Yale economist William Nordhaus has estimated that 98 percent of the economic gains from innovation and entrepreneurship are received by persons other than the innovator. See William D. Nordhaus, “Schumpeterian Profits in the American Economy: Theory and Measurement,” Cowles Foundation Discussion Paper No. 1457, April 2004 https://cowles.econ.yale.edu/P/cd/d14b/d1457.pdf. Even if he is wrong by a factor of ten, this would still mean that 80 percent of the gains from entrepreneurship go to the public rather than the entrepreneur.

9 See, Decker et al, supra; C. Mirjam van Praag and Peter H. Versloot, "What is the Value of Entrepreneurship? A Review of Recent Research," Small Business Economics, Volume 29, Issue 4 (December 2007) , pp 351-382 http://link.springer.com/article/10.1007%2Fs11187-007-9074-x; G. R. Steele, “Laissez-faire and the Institutions of the Free Market,” Economic Affairs, September 1999 http://www.lancaster.ac.uk/staff/ecagrs/Laissez%20faire.pdf.

10 Census Bureau, Business Dynamics Statistics, Establishment Characteristics Data Tables http://www2.census.gov/ces/bds/estab/bds_e_all_release.xlsx.

11 Ian Hathaway and Robert Litan, "The Other Aging of America: The Increasing Dominance of Older Firms," Brookings Institution, July 2014 http://www.brookings.edu/~/media/research/files/papers/2014/07/aging%20america%20increasing%20dom inance%20older%20firms%20litan/other_aging_america_dominance_older_firms_hathaway_litan.pdf; see also Decker et al, supra.

12 John Haltiwanger, Ian Hathaway and Javier Miranda, “Declining Business Dynamism in the U.S. High- Technology Sector,” Kauffman Foundation, February 2014 http://www.kauffman.org/~/media/kauffman_org/research%20reports%20and%20covers/2014/02/declining _business_dynamism_in_us_high_tech_sector.pdf.

13 Title I, The Jumpstart Our Business Startups Act, Public Law 112–106, April 5, 2012 http://www.gpo.gov/fdsys/pkg/PLAW-112publ106/pdf/PLAW-112publ106.pdf.

14 David R. Burton, "Reducing the Burden on Small Public Companies Would Promote Innovation, Job Creation, and Economic Growth," Heritage Foundation Backgrounder No. 2924, June 20, 2014 http://www.heritage.org/research/reports/2014/06/reducing-the-burden-on-small-public-companies-would- promote-innovation-job-creation-and-economic-growth.

15 Wendy Guillies, “Kauffman Foundation 2015 State of Entrepreneurship Address,” February 11, 2015 http://www.kauffman.org/~/media/kauffman_org/resources/2015/soe/2015_state_of_entrepreneurship_spee ch.pdf; John Dearie and Courtney Geduldig, Where the Jobs Are: Entrepreneurship and the Soul of the American Economy (Wiley: 2013); William C. Dunkelberg and Holly Wade, “NFIB Small Business Economic Trends,” August 2014 http://www.nfib.com/Portals/0/PDF/sbet/sbet201408.pdf.

16 For an international survey of regulatory impediments to entrepreneurship and a literature survey, see Doing Business 2014: Understanding Regulations for Small and Medium-Size Enterprises (World Bank: 2013) http://www.doingbusiness.org/~/media/GIAWB/Doing%20Business/Documents/Annual- Reports/English/DB14-Full-Report.pdf ; for a list of regulatory impediments to entrepreneurship in the United States and proposed reforms to address them, see David R. Burton, “Building an Opportunity Economy: The State of Small Business and Entrepreneurship,” Testimony before The Committee on Small Business, United States House of Representatives, March 4, 2015 http://smallbusiness.house.gov/uploadedfiles/3-4-2015_final_burton_tesimony_final.pdf .

17 Compliance costs include legal, accounting and administrative costs but not lost economic output (i.e. the deadweight loss or excess burden of the tax system).

18Scott A. Hodge, “The Compliance Costs of IRS Regulations,” Tax Foundation Fiscal Fact No. 512, June 2016, https://files.taxfoundation.org/legacy/docs/TaxFoundation_FF512.pdf and Jason J. Fichtner and Jacob M. Feldman, “The Hidden Costs of Tax Compliance,” Mercatus Center, May 20, 2013, https://www.mercatus.org/system/files/Fichtner_TaxCompliance_v3.pdf.

19Internal Revenue Service, “4. Figuring Depreciation Under MACRS,” https://www.irs.gov/publications/p946/ch04.html.

20 Ibid.

21 See “Instructions for Form 4626, Alternative Minimum Tax – Corporations,” https://www.irs.gov/pub/irs-pdf/i4626.pdf. For shareholders, partners or members of pass-through entities, the individual AMT would apply.

22 26 CFR 1.312-15. Earnings and profits is primarily used to determine if a corporate distribution is a taxable dividend or a return of capital.

23 Internal Revenue Code §179 and various special expensing provisions.

24 Accounting Periods and Methods, Inventories, IRS Publication 538 https://www.irs.gov/pub/irs- pdf/p538.pdf .

25 For a more complete discussion, see David R. Burton, "A Guide to Tax Reform in the 115th Congress," Heritage Foundation Backgrounder No. 3192, February 10, 2017 http://www.heritage.org/sites/default/files/2017-02/BG3192.pdf.

26 David Burton, "Constructive Small Business Expensing Bill Introduced," The Daily Signal, April 11, 2014 http://dailysignal.com/2014/04/11/constructive-small-business-expensing-bill-introduced/; Curtis Dubay, “Ways and Means Committee Following Right Approach on Tax Extenders,” The Daily Signal, May 27, 2014 http://dailysignal.com/2014/05/27/ways-means-committee-following-right-approach-tax- extenders/.

27 Kathryn Kobe, “Small Business Retirement Plan Availability and Worker Participation,” Small Business Administration, Office of Advocacy, March 2010, Table 2 (only 28 percent of firms with under 100 employees offered some kind of retirement plan in 2006) https://www.sba.gov/sites/default/files/rs361tot.pdf.

28 See generally, David C. John, “Pursuing Universal Retirement Security Through Automatic IRAs and Account Simplification,” Testimony before The Committee on Ways and Means, United States House of Representatives, April 17, 2012 http://www.heritage.org/research/testimony/2012/04/pursuing-universal- retirement-security-through-automatic-iras-and-account-simplification.

29 J.D. Foster, "Obama’s Capital Gains Tax Hike Unlikely to Increase Revenues," Heritage Foundation Backgrounder #2391, March 24, 2010 http://www.heritage.org/research/reports/2010/03/obamas-capital- gains-tax-hike-unlikely-to-increase-revenues; Stephen J. Entin, 'President Obama’s Capital Gains Tax Proposals: Bad for the Economy and the Budget," Tax Foundation January 21, 2015 http://taxfoundation.org/blog/president-obama-s-capital-gains-tax-proposals-bad-economy-and-budget.

30 Then Ways and Means Committee Chairman Dave Camp proposed this in his Tax Reform Act of 2014 discussion draft. See section 3301 http://waysandmeans.house.gov/uploadedfiles/ways_and_means_section_by_section_summary_final_0226 14.pdf.

31 Rep. French Hill introduced H.R. 4831 (114th Congress) which would disregard crowdfunding and Regulation A shareholders for purposes of the subchapter S shareholder limit count. See David Burton, “The Tax Law Makes It Almost Impossible for ‘S Corporations’ to Use Equity Crowdfunding,” Daily Signal, April 19, 2016 http://dailysignal.com/2016/04/19/the-tax-law-makes-it-almost-impossible-for-s- corporations-to-use-equity-crowdfunding/ .

32 David R. Burton, "Obamacare’s Health Insurance Tax Targets Consumers and Small Businesses," Heritage Foundation Issue Brief #4075, October 31, 2013. http://www.heritage.org/research/reports/2013/10/obamacare-s-health-insurance-tax-targets-consumers- and-small-businesses.

33 For general background see “Present Law and Background Relating to Worker Classification for Federal Tax Purposes,” Joint Committee on Taxation, [JCX-26-07] May 8, 2007 http://www.jct.gov/x-26-07.pdf. See also “Independent Contractor or Employee,” IRS Publication No. 1779 https://www.irs.gov/pub/irs- pdf/p1779.pdf ; IRS Rev. Rul. 87-41 (1987); Treas. Reg. § 31.3121(d)-1 Who are employees.

34 A withholding rate of 25 percent would reflect the 15.3 percent payroll tax plus an approximately 10 percent average income tax liability.

35 William W. Beach, “Seven Reasons Why Congress Should Repeal, Not Fix, the Death Tax,” Heritage Foundation Web Memo #2688, November 9, 2009 http://www.heritage.org/research/reports/2009/11/seven-reasons-why-congress-should-repeal-not-fix-the- death-tax; John L. Ligon, Rachel Greszler and Patrick Tyrrell, “The Economic and Fiscal Effects of Eliminating the Federal Death Tax,” Heritage Foundation Backgrounder #2956, September 23, 2014 http://www.heritage.org/research/reports/2014/09/the-economic-and-fiscal-effects-of-eliminating-the- federal-death-tax.

36 David R. Burton, "Four Conservative Tax Plans with Equivalent Economic Results," Heritage Foundation Backgrounder No. 2978, December 15, 2014 http://www.heritage.org/research/reports/2014/12/four-conservative-tax-plans-with-equivalent-economic- results ; David R. Burton, "A Guide to Tax Reform in the 115th Congress," Heritage Foundation Backgrounder No. 3192, February 10, 2017 http://www.heritage.org/sites/default/files/2017- 02/BG3192.pdf.

37Paul Ryan and Kevin Brady, “A Better Way: Our Vision for a Confident America, Tax,” June 24, 2016, https://abetterway.speaker.gov/_assets/pdf/ABetterWay-Tax-PolicyPaper.pdf.

38Kyle Pomerleau, “Details and Analysis of the 2016 House Republican Tax Reform Plan,” Tax Foundation Fiscal Fact No. 516, July 2016, https://files.taxfoundation.org/legacy/docs/TaxFoundation_FF516.pdf.

39 Congressional Budget Office, The Budget and Economic Outlook: 2017 to 2027, January 2017, Summary Table 1, CBO’s Baseline Budget Projections, p. 2, https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/51129-2016outlook.pdf.

40Graduated rate versions of the Hall–Rabushka flat tax are often called an “X Tax” after David Bradford’s proposal. See David F. Bradford, Untangling the Income Tax (Cambridge, MA: Harvard University Press, 1986). See also Report of the President’s Advisory Panel on Federal Tax Reform, 2005, http://govinfo.library.unt.edu/taxreformpanel/final-report/index.html.

*******************

The Heritage Foundation is a public policy, research, and educational organization recognized as exempt under section 501(c)(3) of the Internal Revenue Code. It is privately supported and receives no funds from any government at any level, nor does it perform any government or other contract work.

The Heritage Foundation is the most broadly supported think tank in the United States. During 2014, it had hundreds of thousands of individual, foundation, and corporate supporters representing every state in the U.S. Its 2014 income came from the following sources:

Individuals 75%

Foundations 12%

Corporations 3%

Program revenue and other income 10%

The top five corporate givers provided The Heritage Foundation with 2% of its 2014 income. The Heritage Foundation’s books are audited annually by the national accounting firm of RSM US, LLP.

Members of The Heritage Foundation staff testify as individuals discussing their own independent research. The views expressed are their own and do not reflect an institutional position for The Heritage Foundation or its board of trustees.