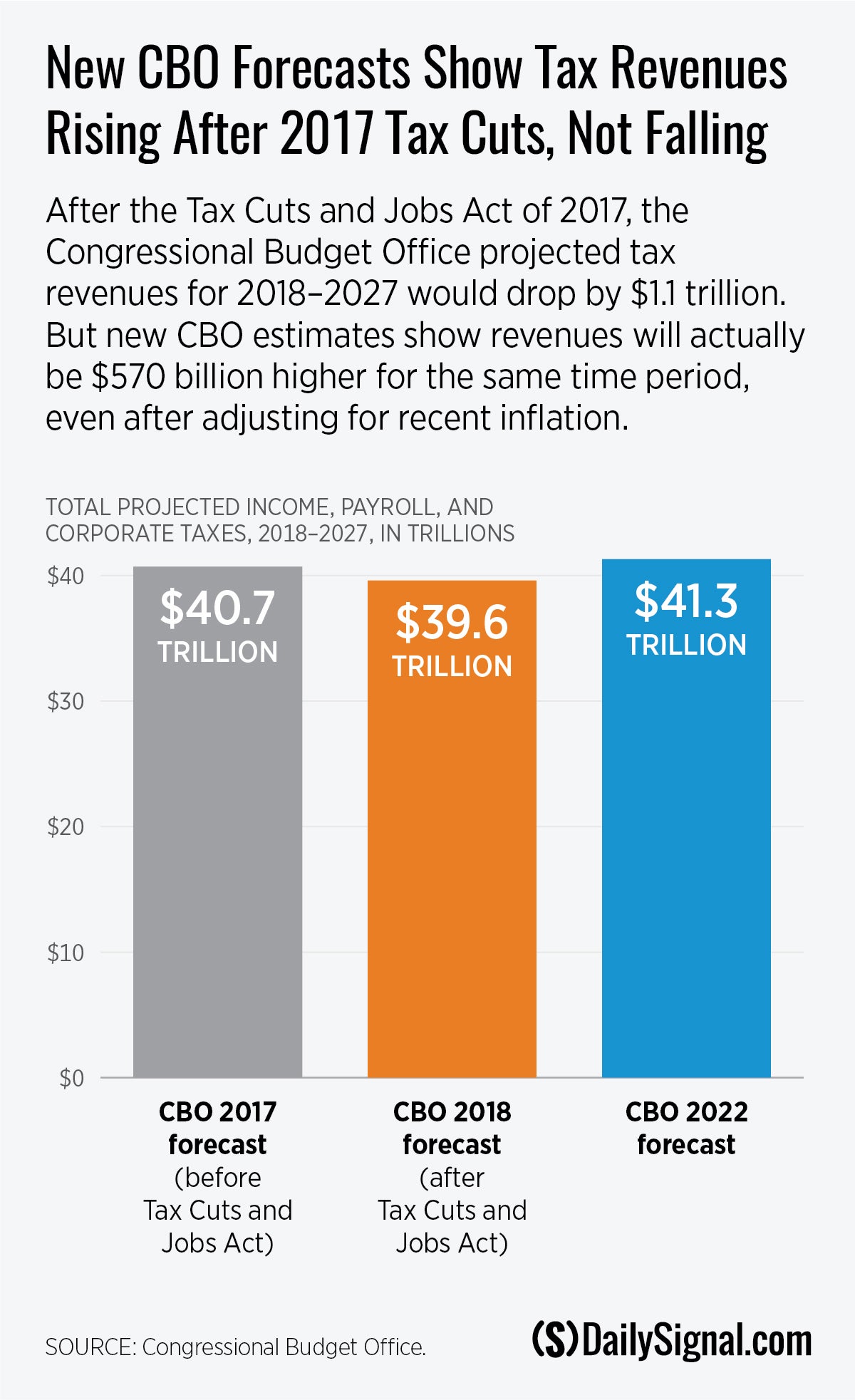

The Congressional Budget Office’s May 2022 forecast shows that the government now expects to bring in more tax revenue in the decade following the 2017 “Trump tax cuts” than it had projected prior to the December 2017 passage of tax reform.

It doesn’t look like the tax cuts—which government scorekeepers said at the time would cost $1.5 trillion over 10 years—have been anything like the fiscal nightmare that some on the left would lead us to believe.

In March, Speaker of the House Nancy Pelosi, D-Calif., called the 2017 Trump tax cuts a $2 trillion “GOP tax scam.”

Sen. Bernie Sanders, I-Vt., accused Republicans of hypocrisy for supporting the tax cuts but opposing Congress’ massive spending spree.

The Biden White House issued a press release claiming “the Trump tax cuts had added $2 trillion to deficits over a decade.”

But the numbers tell a different story. Despite the political rhetoric, tax revenues are up.

Adjusting the forecasts to actual 2022 dollars, prior to the tax cuts the government projected $40.7 trillion of income tax, corporate tax, and payroll tax revenues between 2018 and 2027. The latest budget forecasts project $41.3 trillion of revenues for that period. Instead of reducing revenues by $1.5 trillion, the latest forecasts suggest tax revenues will come in $570 billion higher than expected.

What about the corporate tax cuts? Surely cutting the corporate tax rate from 35% to 21% must have dramatically reduced corporate tax revenue?

Not according to the government budget numbers.

The government now expects to bring in $3.8 trillion in corporate tax revenues between 2018 and 2027, almost identical to the $3.9 trillion forecasted prior to the tax cuts. Moreover, since taxes don’t exist in a vacuum—and the corporate tax reform propelled higher income growth and therefore higher income taxes and payroll taxes—the corporate tax reform likely paid for itself.

Could the Congressional Budget Office have simply underestimated tax revenues in the pre-tax cuts forecast?

Maybe. But the budget office says that historically it has more often overestimated revenues. According to the government forecasters, “CBO’s revenue projections have been too high, on average, in recent decades, mainly because of the difficulty of forecasting the timing and nature of economic downturns.”

So, then, why didn’t the expected drop in tax revenues happen, especially given that the decade included a global shutdown related to the pandemic? The budget office’s forecasts make at least five references to the “unexplained strength” of tax receipts.

According to economists Tyler Goodspeed and Kevin Hassett, after the 2017 tax cuts, business investment soared 9.4% compared to the pre-tax cuts trend. For corporations, real investment rose 14.2%. Similarly, a 2021 Heritage Foundation report showed the dramatic growth in investment and wages that occurred after the tax cuts. A key driver in the surge in investment was multinational firms who chose to reinvest in U.S. markets instead of offshoring.

Conservatives anticipated the cut in the corporate rate and the allowance of full expensing of capital purchases would drive strong growth in investment. The full expensing provisions allow businesses to immediately deduct the cost of machinery and equipment, instead of following convoluted depreciation schedules lasting up to 20 years.

The reinvestment in America that tax reform spurred paid real dividends for the typical household, increasing their annual rate of income growth tenfold.

Real median household incomes grew by more than $5,000 in 2018 and 2019 alone. By contrast, in the 30 years prior to 2017, real median household income grew by a total of $7,600, or about $250 per year.

Then, starting in 2020, as the economy was roaring along with record high wages, record low unemployment, strong labor force participation, and low inflation, the government’s multitrillion-dollar hyperactive response to the pandemic took the economy and the budget off the rails.

Because of the glut of new spending, the Congressional Budget Office now projects that federal outlays will be more than $9 trillion higher between 2020 and 2029 than it forecast at the start of 2020. Unlike the Trump tax cuts, it appears the final price tag on the recent federal spending binge will be even higher than originally advertised.

All Americans are paying part of that price now in the form of higher inflation.

As of February 2021, the Congressional Budget Office was forecasting 1.9% inflation in 2021 and inflation at or below 2.4% throughout the decade. Instead, after the spending spree, the April 2022 inflation figures showed that Americans are paying 8.3% higher prices than they were a year ago.

If interest rates rise significantly in response to the inflation, then Americans may end up paying the price for the excess spending for many years to come.

Because of the combined effect of increases in interest rates and the debt, by 2032, the forecasts show that the entire economic output of Alaska, Delaware, Idaho, Maine, Montana, New Hampshire, North Dakota, Rhode Island, South Dakota, West Virginia, and Wyoming would be insufficient to pay the annual interest on the national debt. That’s 11 states.

The higher interest rates caused by Washington’s overspending will also crowd out business investment and leave workers with lower real wages than they would otherwise have.

Congress and the Biden administration must stop making it harder to do business and work in America. It’s time to reverse our current course and instead double down on pro-growth policies that were working well just over two years ago.

Unfortunately, many of the provisions of the Trump tax cuts are set to expire over the next few years. The capital expensing provisions under current law will gradually expire between 2023 and 2027.

Lawmakers should unapologetically push to permanently extend tax reforms that drive investment and growth in America, while simultaneously plucking the nation’s overdrawn credit card away from their overspending colleagues.

This piece originally appeared in The Daily Signal