Banks and non-bank financial firms are extensively regulated in the United States. While banks are even more heavily regulated than other financial firms, virtually all financial companies are subject to extensive restrictions on their activities, capital, and asset composition. There have been many changes to federal rules and regulations during the past few decades, and some of those changes have allowed financial firms to engage in activities from which they were previously prohibited. However, there has never been a substantial reduction in the scale or scope of financial regulations in the U.S.

Regulation of banks, in particular, has increased episodically. Simultaneously, in the name of ensuring stability, U.S. taxpayers have absorbed more of the financial losses due to risks undertaken by private market participants. This combination of policies has produced a massive substitution of government regulation for market competition, which culminated in the 2008 financial crisis. Fixing this framework requires rolling back both government regulation and taxpayer backing of financial losses, making it possible for private citizens to build a stronger financial system that efficiently directs capital to its most valued uses.

Government rules that profess to guarantee financial market safety create a false sense of security, lower private incentives to monitor risk, increase institutions’ financial risk, and protect incumbent firms from new competitors. It is important to reverse these trends because competition in markets drives innovation, lowers prices, prevents excessive risk taking, and allows people to invest their savings in the best investment opportunities. There are many policy solutions to begin restoring the competitive process and strengthening financial markets, such as providing regulatory off-ramps for firms with higher equity funding. This chapter focuses on one option: creating a new federal charter for financial institutions, whose owners and customers absorb all of their financial risks.

Basic Regulatory Off-Ramp

In September 2016, the House Financial Services Committee passed H.R. 5983, a regulatory reform bill called the Financial CHOICE Act.1 This legislation would replace large parts of the 2010 Dodd–Frank Wall Street Reform and Consumer Protection Act, and also provide banks a regulatory off-ramp in the form of a capital election. This off-ramp relieves banks of certain regulations if they improve their ability to absorb losses by funding their operations with higher equity capital. Put differently, the provision exempts banks from regulations if they meet a higher capital ratio, thus credibly reducing their probability of failure and any consequent taxpayer bailouts.

The CHOICE Act’s capital election requires banks to have an average leverage ratio of at least 10 percent. The off-ramp mainly provides relief from Dodd–Frank regulations related to capital and liquidity standards, capital distributions to shareholders, and mergers and acquisitions.2 It effectively relieves qualified banks of compliance with the Basel III capital rules.3 Though there are many ways to implement a regulatory off-ramp, this approach—requiring a firm to meet a higher capital ratio—can easily be expanded to provide additional regulatory relief.

The most obvious method would be to raise the equity-capital threshold above a 10 percent ratio, and increase the list of exemptions as higher capital ratios are met, though implementing an off-ramp in such a tiered fashion would be needlessly complex. An alternative approach is to create a new federal charter under which financial institutions are regulated more like banks were regulated before the modern era of bank bailouts and government guarantees. Broadly, the idea is to replace government regulation and supervision with a sensible disclosure regime contingent on high-equity capital.

A New Federal Charter for Financial Companies

Currently, creating a new national bank requires the approval of a charter application by the Office of the Comptroller of the Currency (OCC) or the state banking regulator in which the headquarters will be located. The Federal Deposit Insurance Corporation (FDIC) must also approve a deposit-insurance application.4 The charter proposed in this chapter would explicitly prohibit FDIC insurance for the proposed new banks or any subsidiaries. Only the OCC would approve these proposed charters because these charters provide exemptions from federal regulations. The OCC currently applies several evaluative factors to new charter applications, and assesses these factors on three main elements: (1) the business plan; (2) the character and competence of the bank’s management and directors; and (3) financial resources.5

The charter proposed in this chapter would essentially restrict the OCC to ensuring the character of management and directors through standard background checks and verifying that the firm meets a relatively high equity ratio. The OCC would no longer, for example, approve an application based on the agency’s assessment of the company’s risk profile, the owners’ ability to attract and maintain community support, or whether the agency believes the company can remain profitable.6 The purpose of eliminating such criteria is to eliminate regulators’ subjective view of the bank’s prospects from the approval process.

Instead, the OCC would verify whether the company satisfies various objective requirements. One of the requirements would be that the bank can absorb substantial losses before it is forced into resolution. The bank would be allowed to operate with relatively few regulatory requirements. The core economic rationales for current subjective evaluations of new banks’ charters center on federal deposit insurance and bailouts, both of which put taxpayers at risk. Eliminating those factors removes the core justification for extensive government regulation. FDIC deposit insurance in particular would not be available to the bank’s depositors.7

Extended Liability, Non-Corporate Entities, Higher Equity

Policies that help to ensure that financial firms’ owners and creditors bear any financial losses impose market discipline on the firms. When financial firms’ capital suppliers have more of their own funds at risk, they invest more carefully and monitor firms’ operations more closely. Prior to the expansion of federal policies that shift those losses to others, financial firms signaled their financial strength by having very high capital ratios (by today’s standards) and by other means, such as extended liability for shareholders.

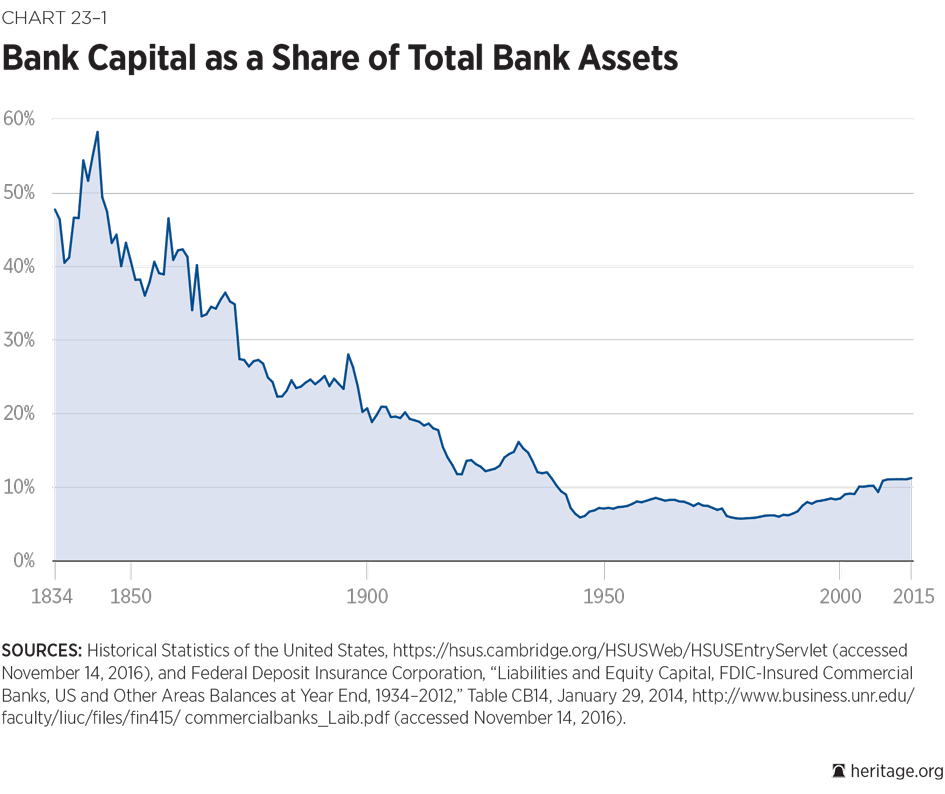

Figure 1 shows capital-to-asset ratios for banks since 1834. The much lower ratios today, due in no small part to federal deposit insurance since 1933, are obvious. Capital ratios were much higher in the 19th century, falling from about 35 percent after the Civil War to 20 percent by 1900.8 While today’s bankers often will argue that 6 percent capital is high enough, it is clear that commercial banking without deposit insurance and bailouts involved significantly higher capital than today’s extraordinarily low levels. Besides capital, owners of banks often were obligated to provide additional funds to banks’ depositors.

Extended liability—by way of double, triple, or, in California, unlimited liability—was common for commercial banks before Congress enacted federal deposit guarantees in 1933 through the FDIC.9 Investment banks were typically partnerships (rather than corporations) until late in the 20th century, with Goldman Sachs being the last of the big firms to go public in 1999.10 Given that there are some financial firms currently organized as general partnerships, it is at least plausible that some investors would be willing to organize financial firms under an extended liability regime if they were allowed to do so as part of a regulatory off-ramp. Such firms would have a disadvantage in raising capital from widespread investors because stockholders would have to be qualified to assume the possible liability, but such a disability relative to publicly traded corporations should not prevent policymakers from giving investors the option of organizing such banks to obtain regulatory relief.11 In some ways, extended liability would be an advantage because the ownership of such banks would be concentrated in owners able and willing to bear the risk in exchange for the rewards.12

The organization of most large financial firms as publicly traded companies without extended liability certainly suggests that a better option, at least at this time, would be to tie a regulatory off-ramp to a higher equity requirement. A natural starting point for thinking about a reasonable equity ratio is something on the order of the ratios prior to the advent of federal deposit guarantees and bailouts. One problem, of course, is that state-chartered banks were the rule in the U.S. banking industry until after the Civil War, and state regulations differed widely. Nonetheless, research indicates that New York banks had an average capital-to-asset ratio of 39 percent in 1850, and that the ratio had fallen to 14 percent by 1900.13 Other estimates indicate that national banks had capital-to-asset ratios between 30 percent and 40 percent from 1866 until just prior to 1900.14

Based on these historical figures, and the fact that such a high capital requirement would only be imposed on a firm that actively chooses to organize under the new charter, one plausible minimum ratio of capital to assets would be 40 percent. Naturally, the new charter would also have to define capital and assets, a process that is more involved now than it was in the early 1900s. Capital should be defined to include only common-equity Tier 1 capital,15 and assets should be a comprehensive measure that includes total off-balance-sheet and net-derivatives exposures.16 The ratio of these two quantities is most nearly comparable to these historic ratios.

While this ratio is extraordinarily high compared to present capital ratios, banks’ current capital ratios (as low as 6 percent) are extremely low by historical standards, and lowest for large banks. The ratios are too low and offload substantial risk and losses onto taxpayers. Policymakers and financial experts have suggested various alternative ratios. For instance, Alan Greenspan, Anat Admati, and Martin Hellwig have suggested that 20 percent capital for all banks is far more consistent with a sound banking system than the current single-digit levels of capital relative to assets.17

An equity ratio at such a relatively high level might well impose higher funding costs on firms adopting the new charter relative to today’s commercial banks and the typical non-banking financial company. However, meeting this relatively high equity ratio would drastically reduce a firm’s probability of failure and lower the probability of taxpayer bailouts under any circumstances. As a result, there is no economic justification for regulating such firms’ operations. The reduction in regulation would provide a benefit to any such highly capitalized bank, a benefit that can be compared to the cost of additional capital. There is a very long list of regulations from which firms organizing under the new charter could be exempt to make this structure attractive and economically feasible.

Regulatory Framework and Exemptions

Banks are highly regulated by both state and federal regulators, perhaps more so than any other business. These regulations can be broadly grouped into: (1) chartering and entry restrictions; (2) regulation and supervision; and (3) examination.18 A goal of this charter proposal, in addition to lowering federal government guarantees and reducing bank bailouts, is to lower federal regulatory restrictions. In practice, both state and federally chartered banks are also subject to state laws and regulations governing the basic transactions with customers.

For instance, state laws, most notably the Uniform Commercial Code, govern practices such as transactions in commercial paper and promissory notes, bank deposits, funds transfers, secured transactions, and contracts.19 While federal law governs federally chartered banks’ rights and obligations as chartered entities, state laws typically govern some banks’ charters, safety, and soundness as well as securities transactions, insurance, real property, and mortgages. This charter proposal does not seek to usurp state laws concerning contracts or which prohibit fraud and material misstatements. The charter should, however, pre-empt state authority over the registration of securities.20

Because the proposal aims to replace government regulation and supervision with a sensible disclosure regime contingent on high-equity capital, the main task of government regulators would be to examine banks to ensure compliance with the capital requirement. Laws that mandate disclosure and enhance enforcement through civil liability rules have a more positive impact than other forms of securities regulations, and evidence suggests that this type of disclosure and private monitoring would work well even in the banking sector.21 Using the proposed charter, therefore, banks would be faced mostly with regulations that focus on punishing and deterring fraud, and fostering the disclosure of information that is material to investment decisions.

Following is an outline of what the regulatory framework would look like for a firm organized under the new charter:

- The OCC would evaluate the new charter, ensuring the character of management and directors through standard background checks.

- The OCC would serve as the primary regulator for the bank, and the agency’s main task would be to ensure that the firm adheres to the capital requirement. The OCC would examine the bank’s assets and capital every six months.

- The firm would have to demonstrate that it meets a 40 percent capital-to-asset ratio with capital defined as common-equity Tier 1 capital, and total assets defined to include off-balance-sheet and net-derivatives exposures.

- After beginning operation, failure to meet the capital requirement would result in the bank losing its charter and being closed.22 A bank that fails to meet the capital ratio would be given a grace period to return capital to 40 percent, say two or three months, and then suspension of operations would be required. Starting from such a high capital level, the losses to depositors and other creditors are likely to be small or zero.

- The firm would be subject to the affiliate restrictions in Section 23A and Section 23B of the Federal Reserve Act. Section 23A limits the aggregate amount of transactions the bank (and its subsidiaries) can conduct with any affiliate to no more than 10 percent of the bank’s capital stock and surplus, and also limits the aggregate amount of transactions the bank (and its subsidiaries) can conduct with all affiliates to no more than 20 percent of the bank’s capital stock and surplus.23 Section 23B essentially restricts financial transactions between affiliates so that the relationship is not used simply to gain preferential terms or treatment relative to what would be available by interacting with, instead, nonaffiliated companies.24

- Bank holding companies would be limited to owning either a traditional bank or one of the newly chartered banks.

- In the act of providing credit, the firm could not lawfully discriminate based on race, color, religion, national origin, sex, marital status, or age, where discrimination is defined as disparate treatment rather than disparate impact.25

The new charter should also include an explicit prohibition against receiving government funds from any source. In particular, the charter should prohibit the firm and any subsidiaries from receiving:

- FDIC deposit insurance,

- FDIC emergency assistance and loan guarantees,

- Federal Reserve discount window borrowing,

- Federal Reserve emergency credit assistance under any Section 13(3) facility,

- Federal Home Loan Bank Advances,

- Loans from any community development financial institution,

- Loans from any government-sponsored enterprise, federal agency, or newly created government assistance program, and

- Federal or state grants from any government agency.

The charter will also exempt the bank from several specific federal regulations. The following is a list of federal regulations from which the newly chartered firm should be exempt:

- Sections 16 and 21 of the Glass–Steagall Act. Many policymakers mistakenly believe that the 1999 Gramm–Leach–Bliley Act (GLBA) repealed the Glass–Steagall Act (the Banking Act of 1933). In fact, the GLBA only repealed sections 20 and 32 of Glass–Steagall, those that generally prohibited commercial banks from affiliating with investment banks. To this day, two major Glass–Steagall restrictions on banks’ securities dealings remain: (1) Section 16, which generally prohibits commercial banks from underwriting or dealing in securities; and (2) Section 21, which generally prohibits investment banks from accepting demand deposits.26 These restrictions should be eliminated because the simpler the bank’s structure, the easier it would be for depositors and shareholders to monitor the bank’s activities.27

- Capital stress tests and financial-stability mandates. The charter should exempt the bank from any and all regulations promulgated under Title I of Dodd–Frank. Title I created the Financial Stability Oversight Council (FSOC) and tasked the FSOC with, among other things, recommending heightened regulations for risk management at financial firms.28

- Federal capital and liquidity rules. The charter will exempt the bank from any federal law, rule, or regulation addressing capital or liquidity requirements or standards.29 In the late 1980s, federal banking regulators introduced the complex Basel capital rules, a purported improvement over the previous capital requirements. While these rules were intended to improve the safety and soundness of the banking system, the Basel system, in particular its reliance on risk weights, contributed to the 2008 financial crisis.30

- Capital-distribution restrictions. The charter will exempt the bank from any federal law, rule, or regulation that permits a federal regulatory agency to object to a capital distribution. If the bank is temporarily below the required capital level, no dividends or share repurchases would be allowed, but otherwise there is no restriction on such distributions to shareholders.

- Merger and acquisition restrictions. Any federal law, rule, or regulation that provides limitations on mergers, acquisitions, or consolidations, should not apply to the bank, provided such proposed merger, acquisition, or consolidation maintains the required capital ratio and is consistent with the anti-trust laws.

- Truth in Lending Act. The Truth in Lending Act (TILA) was enacted in 1968 to provide uniform consumer protection standards in credit markets, and focused mainly on disclosure requirements for items such as finance charges and the annual percentage rate (APR).31 TILA has been amended numerous times, and it now requires extensive disclosures on calculation methods and explanation of cost-related information.32 In the absence of a federal requirement, financial firms will have incentives to provide adequate disclosures to potential customers and, indeed, it is difficult to see how they could operate successfully without doing so.

- The Home Ownership and Equity Protection Act. Congress passed the Home Ownership and Equity Protection Act (HOEPA) as Title I, Subtitle B of the Riegle Community Development and Regulatory Improvement Act of 1994.33 HOEPA amended TILA to subject certain loans—the rates or fees for which exceed specified limits—to heightened disclosure requirements.34 As enacted, these rules applied to closed-end home equity loans and closed-end loans made to refinance existing mortgages that charged either (1) an APR of more than 10 percentage points above the yield on Treasury securities of comparable maturities, or (2) points and fees that exceed the greater of 8 percent of the loan amount or $400 (adjusted annually for inflation).35 HOEPA requires the disclosure of loan information that financial firms will already have incentives to adequately provide. Furthermore, most of the practices that HOEPA prohibits—such as fraud, deception, and document falsification—are already illegal under state laws.36

- Real Estate Settlement Procedures Act. The Real Estate Settlement Procedures Act (RESPA) was passed in 1974, largely to see that borrowers “are provided with greater and more timely information on the nature and costs of the settlement process and are protected from unnecessarily high settlement charges.”37 The high charges with which the act was concerned stemmed from complaints over lenders advertising loans at a low rate of interest provided the borrower used a specified title insurance company; the title company would then charge an inflated price and kick back a portion of the fee to the lender. It is unclear how the borrower benefits from prohibiting such a practice if lenders can simply raise the interest rate they charge, and evidence suggests that RESPA did not achieve its stated purpose of lowering lending rates. Furthermore, the amount of information that lenders are now required to disclose obfuscates rather than informs the typical borrower, and it is unclear that federal regulation of title and closing costs is even desirable.38

- Home Mortgage Disclosure Act. A primary goal of the 1975 Home Mortgage Disclosure Act (HMDA) was to require banks and savings and loan associations to make data about their overall geographic lending patterns publicly available.39 Over time, the focus of HMDA has changed, first to whether banks were lending in the neighborhoods from which their deposit customers lived, then to whether lenders and even non-bank lenders were discriminating, and ultimately to whether certain groups were being targeted with unfavorable loan terms.40 While HMDA has increased the reporting and liability burden on financial institutions, HMDA itself was not designed as part of an experimental study, and the data generally should not be used to prove discrimination.

- Equal Credit Opportunity Act. The 1974 Equal Credit Opportunity Act (ECOA) was intended to promote adequate disclosure of information to and about credit consumers, and also to shield protected classes of consumers from discrimination when applying for credit.41 Over time, the law has been used more broadly, and now is part of the framework used to prove disparate impact using, among other things, a judicial doctrine known as an effects test, whereby regulators can “prohibit a creditor practice that is discriminatory in effect because it has a disproportionately negative impact on a prohibited basis, even though the creditor has no intent to discriminate and the practice appears neutral on its face.”42 As explained above, the charter would include a provision against discrimination—where discrimination is defined as disparate treatment rather than disparate impact—based on race, color, religion, national origin, sex, marital status, or age.

- Fair Housing Act. The Fair Housing Act (FHA) was passed in 1968 to prevent discrimination in housing.43 As one Federal Reserve report notes, the “examination of every institution, whether or not the agency suspects discrimination, is strikingly different from the practices of the federal agencies responsible for other areas of anti-discrimination law enforcement.”44 As explained above, the charter would include a provision against discrimination—where discrimination is defined as disparate treatment rather than disparate impact—based on race, color, religion, national origin, sex, marital status, or age.

- Community Reinvestment Act. The 1977 Community Reinvestment Act (CRA) was supposed to address banks’ provisioning of credit in the communities in which they operate, with a particular focus on how banks provide credit to low-income and moderate-income neighborhoods.45 The CRA was amended in 1989 to require public disclosure of banks’ CRA ratings, and again in 2005 to account for differences in bank sizes and business models.46 The 1999 GLBA required bank holding companies to register with the Federal Reserve, and made approval contingent upon Fed certification that both the holding company and all of its subsidiary depository institutions were (among other requirements) in compliance with the CRA.47 Regulators currently take CRA ratings into account when considering (among other things) applications to open new branches, move existing branches, and merge with other banking organizations.48 Simply put, sound underwriting—not social policies—would guide lending decisions by these newly chartered institutions.

- Money Laundering/Know-Your-Customer rules. The current anti-money-laundering (AML) regulatory framework is clearly not cost-effective. The AML regime costs an estimated $4.8 billion to $8 billion per year, yet results in fewer than 700 convictions annually, a proportion of which are simply additional counts against persons charged with other predicate crimes.49 The current framework is overly complex and burdensome, and its ad hoc nature has likely impeded efforts to combat terrorism and enforce laws. The newly chartered bank should be exempt from the existing reporting requirements, particularly the low-threshold currency-transaction reports (CTRs) and suspicious-activity reports (SARs). In the absence of an AML regulatory framework, these firms would remain legally liable for facilitating criminal behavior.50

- The Volcker Rule. Section 619 of the Dodd–Frank Act imposed a banking regulation known as the Volcker Rule. This rule is intended to protect taxpayers by prohibiting banks from making risky investments (trades) solely for their own profit, a practice known as proprietary trading. Although it sounds logical to stop banks from making “risky bets” with federally insured deposits, this idea ignores the basic fact that banks make risky investments with federally insured deposits every time they make a loan. Furthermore, the practical difficulties associated with implementing the rule caused regulators to spend years working on what ended up being an enormously complex rule.51 Regardless, it makes no sense to subject banks that organize under the charter proposed in this chapter to the Volcker Rule, because such banks would not be eligible for federal deposit insurance.

Conclusion

There is little, if any, justification for heavily regulating financial firms that absorb their own financial losses. Furthermore, centralized government regulation and micromanagement of financial risk has repeatedly failed to maintain the safety and soundness of the financial system. Replacing government regulation of financial firms with true market discipline would lower the risk of future financial crises and improve individuals’ ability to build wealth. It is of course possible that no one would want to start such a bank. The value of current subsidies may well offset the value of being less regulated.

On the other hand, small banks are currently allowed to fail with losses imposed on non-insured depositors and other creditors, and such a charter might have substantial value to some investors and some depositors. There is no reason to prevent people from organizing such banks and depositing funds in these institutions should they wish, and providing the option to organize such banks would give Americans a clear path to prosperity thanks to reduced government regulations.

—Gerald P. Dwyer, PhD, is Professor of Economics and BB&T Scholar at Clemson University, an Adjunct Professor at the University of Carlos III in Madrid, and a Research Associate at the Centre for Applied Macroeconomic Analysis at Australian National University. He was previously Director of the Center for Financial Innovation and Stability at the Federal Reserve Bank of Atlanta. Norbert J. Michel, PhD, is a Research Fellow in Financial Regulations in the Thomas A. Roe Institute for Economic Policy Studies, of the Institute for Economic Freedom, at The Heritage Foundation.

This report is part of Prosperity Unleashed: Smarter Financial Regulation. Government policies have—for decades—empowered regulators to manage private risks and mitigate private losses in an effort to prevent financial-sector turmoil from spreading to the rest of the economy. This approach, rarely contemplated in nonfinancial industries, has demonstrably failed. Prosperity Unleashed: Smarter Financial Regulation provides solutions to the core regulatory problems that existed in U.S. financial markets long before the 2008 financial crisis.

Endnotes

1. The acronym CHOICE stands for Creating Hope and Opportunity for Investors, Consumers and Entrepreneurs. The Committee passed the CHOICE Act on September 13, 2016, by a vote of 30 to 26; the text is available at Congress.gov, “H.R. 5983–Financial CHOICE Act of 2016,” https://www.congress.gov/bill/114th-congress/house-bill/5983/actions (accessed September 14, 2016).

2. Norbert J. Michel, “Money and Banking Provisions in the Financial CHOICE Act: A Major Step in the Right Direction,” Heritage Foundation Backgrounder No. 3152, August 31, 2016, http://www.heritage.org/research/reports/2016/08/money-and-banking-provisions-in-the-financial-choice-act-a-major-step-in-the-right-direction.

3. The Basel III requirements are not directly mandated by Dodd–Frank. The Dodd–Frank Act did not explicitly require adoption of the Basel III rules, but it did include language—mostly in sections 165 and 171— that effectively directed federal banking agencies to implement the Basel III proposals as part of its heightened regulations for specially designated firms. Although the Basel rules themselves are aimed at large international banks, U.S. federal banking regulators have imposed the Basel standards on virtually all U.S. commercial banks beginning in the 1980s. The 1983 International Lending Supervision Act gave federal regulators the explicit authority to regulate banks’ capital adequacy, and to define what constitutes adequate capital levels. See 12 U.S. Code § 3907.

4. Office of the Comptroller of the Currency, “Becoming a National Bank,” February 2011, http://www.occ.treas.gov/publications/publications-by-type/licensing-manuals/becoming-a-national-bank.pdf (accessed September 15, 2016). Chartering a bank holding company (BHC) also requires Federal Reserve approval. As explained above, this chapter suggests having only the OCC approve the new financial institution charter. The OCC has the authority to charter national banks (even uninsured banks) under the National Bank Act of 1864, as amended, 12 U.S. Code Chapter 1 et seq., and federal savings associations under section 5 of the Home Owners’ Loan Act, 12 U.S. Code § 1464.

5. For a general discussion, see Office of the Comptroller of the Currency, “Becoming a National Bank,” pp. 5–10. These OCC regulations are found at 12 C.F.R. 5.20.

6. Most of the current requirements regarding these types of factors are in 12 C.F.R. 5.20(e) through 12 C.F.R. 5.20(h).

7. The bank would of course be required to post this fact—that the bank is not eligible for federally backed deposit insurance—prominently in advertising, on any website, and in any offices frequented at which business with customers is conducted.

8. Howard Bodenhorn, “Double Liability at Early American Banks,” NBER Working Paper No. 21494, August 2015, http://www.nber.org/papers/w21494.pdf (accessed September 15, 2016), and Richard Grossman, “Other People’s Money: The Evolution of Bank Capital in the Industrialized World,” Wesleyan Economics Working Paper No. 2006-020, April 2006, http://repec.wesleyan.edu/pdf/rgrossman/2006020_grossman.pdf (accessed September 15, 2016).

9. Congress amended the National Bank Act and the Federal Reserve Act to remove double liability from national bank shares issued after 1933. In 1935, Congress allowed national banks to terminate double liability after July 1937 on all shares. By the end of World War II, more than half of the states had removed extended liability requirements, with Arizona being the last state to do so in 1956. See Alexander Salter, Vipin Veetil, and Lawrence H. White, “Extended Shareholder Liability as a Means to Constrain Moral Hazard in Insured Banks,” Quarterly Review of Economics and Finance, forthcoming.

10. Though relatively small in size and number, some investment banking firms are still organized as general partnerships. See “Wall Street Partnerships, Brown-Blooded Holdouts,” The Economist, June 16, 2011, http://www.economist.com/node/18836248 (accessed September 15, 2016). Commercial banks are generally not organized as partnerships, though in the past some private banks may have been. The history on private banks in the U.S. is somewhat murky. See Richard Sylla, “Forgotten Men of Money: Private Bankers in Early U.S. History,” The Journal of Economic History, Vol. 36, No. 1 (March 1976), pp. 173–188, http://www.jstor.org/stable/2119809?seq=1#page_scan_tab_contents (accessed October 18, 2016).

11. Several options could be explored in the partnership context, and all of the firms’ debts would not have to be exposed to the same degree of extended liability. General partners could, for instance, take on limited partners with clearly defined limits for only certain types of non-deposit liabilities.

12. Such a framework would also necessitate rules to ensure that owners have sufficient resources. One option would be to adopt rules similar to the SEC’s Regulation D, which define an accredited investor as either a financial institution or a natural person who has an income of more than $200,000 or a residence exclusive net worth of $1 million or more. Incidentally, the new charter proposed herein could also include this type of requirement for shareholders.

13. Bodenhorn, “Double Liability at Early American Banks,” p. 25. The National Bank Acts of 1864 and 1865 did not specify a capital ratio but, instead, established how much capital was required to start a bank based on the population of the town.

14. Grossman, “Other People’s Money,” p. 32.

15. Regulatory capital components are specified at 12 C.F.R. 3.20.

16. There are also several different ways to define a firm’s derivatives exposure; the goal should be to define such exposure as simply as possible without using risk weights. For instance, a flat percentage of notional derivatives could be combined with a firm’s net current credit exposure, and this total could be included in the measure of total assets. See Michel, “Money and Banking Provisions in the Financial CHOICE Act: A Major Step in the Right Direction.”

17. Alan Greenspan, “More Capital Is a Less Painful Way to Fix the Banks,” Financial Times, August 17, 2015, https://www.ft.com/content/4d55622a-44c8-11e5-af2f-4d6e0e5eda22 (accessed October 3, 2016), and Anat Admati and Martin Hellwig, The Bankers’ New Clothes: What’s Wrong with Banking and What to Do About It (Princeton, NJ: Princeton University Press, 2013).

18. For an overview of these bank regulatory functions, see Michael P. Malloy, Principles of Bank Regulation, 3rd ed. (New York: Thomson Reuters, 2011). Also see David Burton and Norbert J. Michel, “Financial Institutions: Necessary for Prosperity,” Heritage Foundation Backgrounder No. 3108, April 14, 2016, http://www.heritage.org/research/reports/2016/04/financial-institutions-necessary-for-prosperity?ac=1#_ftn21.

19. Uniform Commercial Code, https://www.law.cornell.edu/ucc (accessed March 21, 2016). The UCC is not actually “uniform” throughout the country. Different states have enacted somewhat different versions.

20. This is desirable in any case. See Rutheford B. Campbell Jr., “An Open Attack on the Nonsense of Blue Sky Regulation,” The Journal of Corporation Law, Vol. 10, No. 3 (Spring 1985), pp. 556–557, and Rutheford B. Campbell Jr., “Blue Sky Laws and the Recent Congressional Preemption Failure,” The Journal of Corporation Law, Vol. 22, No. 2 (Winter 1997), p. 188.

21. Rafael La Porta, Florencio Lopez-De-Silanes, and Andrei Shleifer, “What Works in Securities Laws?” The Journal of Finance,

Vol. LXI, No. 1 (February 2006), http://onlinelibrary.wiley.com/doi/10.1111/j.1540-6261.2006.00828.x/pdf (accessed March 15, 2016), and James R. Barth et al., “Do Bank Regulation, Supervision and Monitoring Enhance or Impede Bank Efficiency?” Journal of Banking & Finance, Vol. 37 (2013), pp. 2879–2892.

22. The OCC currently retains receivership authority for national banks, even those that are uninsured, at 12 U.S. Code § 191–200. In fact, the OCC recently proposed a new rule to address how the agency would conduct the receivership of an uninsured national bank. See Office of the Comptroller of the Currency, “Receiverships for Uninsured National Banks,” Notice of proposed rulemaking, Federal Register, Vol. 81, No. 177 (September 13, 2016), https://www.gpo.gov/fdsys/pkg/FR-2016-09-13/pdf/2016-21846.pdf (accessed November 1, 2016). Also see Michael H. Krimminger, “Moving Towards a FinTech National Banking Charter?” Harvard Law School Forum on Corporate Governance and Financial Regulation, October 22, 2016, https://corpgov.law.harvard.edu/2016/10/22/moving-towards-a-fintech-national-banking-charter/ (accessed November 1, 2016).

23. These sections specify several covered transactions, including loans, the purchase of investments and securities, and the purchase of assets. See 12 U.S. Code § 371c. The restrictions may have to be written into the charter since the bank would not, in general, be subject to the Federal Reserve Act.

24. These sections specify several covered transactions, including the sale of securities or other assets (including repurchase agreements), and the payment of money or the furnishing of services under a contract or lease. See 12 U.S. Code § 371c–1. The restrictions may have to be written into the charter since the bank would not, in general, be subject to the Federal Reserve Act.

25. Roger Clegg, “Symposium: The Fair Housing Act Doesn’t Recognize Disparate-Impact Causes of Action,” Supreme Court of the United States Blog, January 7, 2015, http://www.scotusblog.com/2015/01/symposium-the-fair-housing-act-doesnt-recognize-disparate-impact-causes-of-action/ (accessed October 5, 2016).

26. Norbert J. Michel, “The Glass–Steagall Act: Unraveling the Myth,” Heritage Foundation Backgrounder No. 3104, April 28, 2016, http://www.heritage.org/research/reports/2016/04/the-glasssteagall-act-unraveling-the-myth?ac=1.

27. Some of the actions by the FSOC are consistent with a belief that banks have complicated corporate structures, which obfuscate the effects of their activities and make them difficult to resolve.

28. 12 U.S. Code § 5322. For a discussion of Title 1 of Dodd–Frank, see Peter Wallison, “Title I and the Financial Stability Oversight Council,” in Norbert J. Michel, ed., The Case Against Dodd–Frank: How the “Consumer Protection” Law Endangers Americans (Washington, DC: The Heritage Foundation, 2016), http://static.heritage.org/2016/The%20Case%20Against%20Dodd-Frank.pdf, and Norbert J. Michel, “The Financial Stability Oversight Council: Helping to Enshrine ‘Too Big to Fail,’” Heritage Foundation Backgrounder No. 2900, April 1, 2014, http://www.heritage.org/research/reports/2014/04/the-financial-stability-oversight-council-helping-to-enshrine-too-big-to-fail.

29. The 1983 International Lending and Supervision Act (Public Law 98–181; 97 Stat. 1284) authorized the federal banking agencies to establish minimum levels of capital, and in 1988 the agencies adopted the Basel capital rules. All such requirements are implemented via rulemaking rather than by statute, and the standards are implemented through multiple rules. See, for instance, Board of Governors of the Federal Reserve System, “Risk-Based Capital Guidelines; Market Risk,” Final Rule, Federal Register,

Vol. 78, No. 243 (December 18, 2013), 12 C.F.R. Parts 208 and 225, https://www.gpo.gov/fdsys/pkg/FR-2013-12-18/pdf/2013-29785.pdf (accessed October 5, 2016), and Office of the Comptroller of the Currency, “Liquidity Coverage Ratio: Liquidity Risk Measurement Standards,” Final Rule, Federal Register, Vol. 79, No. 197 (October 10, 2014), https://www.gpo.gov/fdsys/pkg/FR-2014-10-10/pdf/2014-22520.pdf (accessed October 5, 2016).

30. Kevin Dowd, Martin Hutchinson, Jimi Hinchliffe, and Simon Ashby, “Capital Inadequacies: The Dismal Failure of the Basel System of Capital Adequacy Regulation,” Cato Institute Policy Analysis No. 681, July 29, 2011, http://www.cato.org/publications/policy-analysis/capital-inadequacies-dismal-failure-basel-regime-bank-capital-regulation (accessed October 3, 2016), and Norbert J. Michel and John Ligon, “Basel III Capital Standards Do Not Reduce the Too-Big-to-Fail Problem,” Heritage Foundation Backgrounder No. 2905, April 23, 2014, http://www.heritage.org/research/reports/2014/04/basel-iii-capital-standards-do-not-reduce-the-too-big-to-fail-problem?ac=1#_ftn4.

31. 15 U.S. Code 1601 et seq. TILA is implemented by Regulation Z (12 C.F.R. 1026). TILA was title I of the Consumer Credit Protection Act (Public Law 90–321).

32. Thomas A. Durkin, Gregory Elliehausen, Michael E. Staten, and Todd J. Zywicki, Consumer Credit and the American Economy (New York: Oxford University Press, 2014), pp. 453–481.

33. Riegle Community Development and Regulatory Improvement Act of 1994, Public Law 103–325.

34. Ibid., § 152.

35. Riegle Community Development and Regulatory Improvement Act of 1994 § 152. HOEPA excludes from its coverage residential mortgage transactions (purchase-money mortgages also known as seller or owner financing), open-end credit, and reverse mortgages.

36. Durkin, Elliehausen, Staten, and Zywicki, Consumer Credit and the American Economy, p. 410.

37. 12 U.S. Code 2601 et seq. The Department of Housing and Urban Development (HUD) originally implemented RESPA by Regulation X. Under Dodd–Frank, the Consumer Financial Protection Bureau (CFPB) restated HUD’s implementing regulation at 12 C.F.R. Part 1024 (Federal Register, Vol. 76, No 244 (December 20, 2011), p. 78978). See Consumer Financial Protection Bureau, “Integrated Mortgage Disclosure Rule Under the Real Estate Settlement Procedures Act (Regulation X) and the Truth in Lending Act (Regulation Z),” Federal Register, Final Rule, Vol. 78, No. 251 (December 31, 2013), https://www.gpo.gov/fdsys/pkg/FR-2013-12-31/pdf/2013-28210.pdf (accessed July 20, 2016).

38. Kevin Villani and John Simonson, “Real Estate Settlement Pricing: A Theoretical Framework,” Real Estate Economics, Vol. 10,

No. 3 (September 1982), pp. 249–275, and Mark Shroder, “The Value of the Sunshine Cure: The Efficacy of the Real Estate Settlement Procedures Act Disclosure Strategy,” Cityscape, Vol. 9, No. 1 (2007), http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1089448 (accessed September 30, 2016).

39. The HMDA is implemented by Regulation C, and Dodd–Frank transferred HMDA rulemaking authority from the Federal Reserve Board to the CFPB.

40. Joseph Kolar and Jonathan Jerison, “The Home Mortgage Disclosure Act: Its History, Evolution, and Limitations,” Consumer Finance Law Quarterly Report, Vol. 59, No. 3 (2005), http://buckleysandler.com/uploads/36/doc/HistoryofHMDAapr06.pdf (accessed September 30, 2016), and Patricia McCoy, “The Home Mortgage Disclosure Act: A Synopsis and Recent Legislative History,” Journal of Real Estate Research, Vol. 29, No. 4 (2007), pp. 381–397.

41. The ECOA is implemented by the CFPB’s Regulation B. (See 12 C.F.R., part 1002.) For an overview of policy concerns, see John Matheson, “The Equal Credit Opportunity Act: A Functional Failure,” Harvard Journal on Legislation, Vol. 21 (1982), p. 371,

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1874297 (accessed September 30, 2016).

42. See 12 C.F.R. Part 1002 (Regulation B), Supplement I to §1002.1(a), Section 1002.6—Rules Concerning Evaluation of Applications, December 30, 2011, http://www.consumerfinance.gov/eregulations/1002-Subpart-Interp/2011-31714#1002-1-a-Interp-1 (accessed September 30, 2016). Also see Hans A. von Spakovsky, “‘Disparate Impact’ Isn’t Enough,” Heritage Foundation Commentary, March 22, 2014, http://www.heritage.org/research/commentary/2014/3/disparate-impact-isnt-enough.

43. The FHA is Title VIII of the Civil Rights Act of 1968, as amended (42 U.S. Code 3601, et seq.).

44. John Walter, “The Fair Lending Laws and Their Enforcement,” Federal Reserve Bank of Richmond Economic Quarterly, Vol. 81 (1995), p. 62, http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.202.7566&rep=rep1&type=pdf (accessed July 20, 2016). Also see Roger Clegg, “Silver Linings Playbook: ‘Disparate Impact’ and the Fair Housing Act,” Cato Supreme Court Review (2014–2015), http://object.cato.org/sites/cato.org/files/serials/files/supreme-court-review/2015/9/2015-supreme-court-review-chapter-6.pdf (accessed October 5, 2016).

45. See 12 U.S. Code 2901; the CRA is implemented by Regulations 12 C.F.R. parts 25, 195, 228, and 345.

46. Darryl E. Getter, “The Effectiveness of the Community Reinvestment Act,” Congressional Research Service, 7-5700,

January 7, 2015, https://www.fas.org/sgp/crs/misc/R43661.pdf (accessed October 5, 2016).

47. Code of Federal Regulations, Title 12, Ch. II § 225.82, http://www.gpo.gov/fdsys/pkg/CFR-2013-title12-vol3/pdf/CFR-2013-title12-vol3-part225.pdf (accessed October 5, 2016).

48. Office of the Comptroller of the Currency, “Community Reinvestment Act and Interstate Deposit Production Regulations,” 12 C.F.R. § 25.29, 2005, https://www.occ.gov/topics/compliance-bsa/cra/12cfr25.html#2529 (accessed October 5, 2016).

49. David Burton and Norbert Michel, “Financial Privacy in a Free Society,” Heritage Foundation Backgrounder No. 3157,

September 23, 2016, http://www.heritage.org/research/reports/2016/09/financial-privacy-in-a-free-society.

50. Aside from overt criminal and civil violations, banks would not be permitted, under current law, to rely on willful ignorance as an excuse. In the 2011 Global-Tech Appliances, Inc. v. SEB S.A., the U.S. Supreme Court affirmed the validity of the willful blindness doctrine in both civil and criminal settings. See National Association of Criminal Defense Lawyers, “Criminal Defense Issues: Willful Blindness,” https://www.nacdl.org/criminaldefense.aspx?id=21211 (accessed November 10, 2016).

51. Norbert J. Michel, “The Volcker Rule: Three Years and Nearly 1,000 Pages Later,” The Daily Signal, December 12, 2013,

http://dailysignal.com/2013/12/12/volcker-rule-three-years-nearly-1000-pages-later/. For the final (jointly issued) rule, see Department of the Treasury, “Prohibitions and Restrictions on Proprietary Trading and Certain Interests in, and Relationships With, Hedge Funds and Private Equity Funds,” Federal Register, Vol. 79, No. 21 (January 31, 2014), https://www.gpo.gov/fdsys/pkg/FR-2014-01-31/pdf/2013-31511.pdf (accessed November 10, 2016).