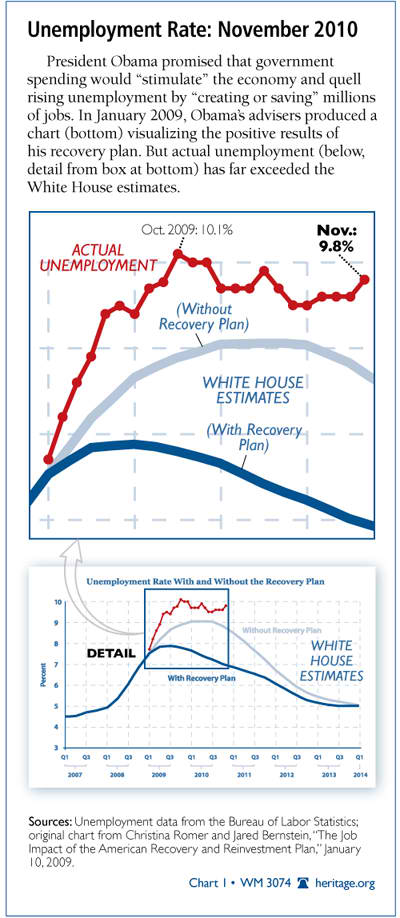

The November employment report threw a bucket of cold water on hopes for an accelerating recovery. The Bureau of Labor Statistics reported that private sector employers added only 50,000 net jobs. Unemployment rose to 9.8 percent and has remained above 9 percent for 19 consecutive months. This ties the record for the longest such stretch since World War II. Weekly hours were flat in November, and average wages increased by just one cent.

The labor market remains mired in a deep recession. This is no time for Congress to raise taxes on business owners and entrepreneurs. Congress should act quickly to extend current tax rates for all Americans.

The November Employment Report

The November employment report showed that the labor market weakened in November. The household survey found that unemployment rose 0.2 percentage points to 9.8 percent—the highest unemployment since April. The unemployment rate rose for both adult men (+0.3 points) and adult women (+0.3 points). Fully10.0 percent of adult men who want jobs cannot find them, and the unemployment rate is much higher for minorities.

The payroll survey also reported weak job creation. Private sector employers added just 50,000 net jobs. Total employment rose by 39,000 net jobs, as government employment fell by 11,000 net jobs with local government losses (–14,000) overcoming increases in federal (2,000) and state (1,000) workers. Total employment remains 7.4 million jobs below its pre-recession peak. The health care (+19,000) and temporary help service (+40,000) sectors created the most net new jobs. However, retailers shed jobs (–28,000), and manufacturers continued to eliminate positions (–13,000).[1] The construction industry (–5,000) fell again in November after October’s small uptick.

The November payroll survey contained one silver lining: Revisions to the September and October reports showed that employers created 38,000 more net jobs in the past two months than previously estimated.

Other economic indicators gave more discouraging news, though. The labor force participation rate remained at its lowest level in 25 years (64.5 percent). Spring and summer increases in hours at work had offered hope that hiring would pick up. However, those increases have not continued. Average weekly hours remained at the same level as August (34.3 hours). Average hourly earnings increased by just one cent in November to $22.75.

Tax Increases and Uncertainty

This report is discouraging, because there are signs that the labor market should be rebounding faster than it is. Businesses have added 357,000 temporary positions over the last year, which usually means that an increase in permanent jobs is about to appear. Economic growth, while slow, usually has stronger employment growth than has happened in the past six months. Policymakers are asking the question of why employers are not adding to their payroll staff.

Policy decisions in Washington have made businesses reluctant to hire and invest. Businesses cannot estimate what their future health care costs or tax burdens will be. Furthermore, the Obama Administration has created regulatory uncertainty by reversing many of its own decisions. For example, business investment in some energy plants ground to a halt as the Administration overturned existing construction permits.

Several presidents of the regional Federal Reserve Banks have cited business uncertainty over Washington decisions as a reason that businesses have not expanded. For example, Jeffrey Lacker, president of the Richmond Federal Reserve, said in an October speech that with “the continuing uncertainty about tax rates for 2011 (now less than three months away), business planners may be finding it more difficult than usual to project economic conditions or the financial implications of prospective hiring and investment commitments. While it is hard to estimate the magnitude of the effects of these fears, or to disentangle them from general expectations of weak demand growth, they are too broad and deep for me to dismiss as implausible the notion that they have significantly dampened consumer and business spending of late.”[2]

Now, the impending tax hikes are four weeks away, and businesses are reacting. Some firms have already starting issuing special dividend payments ahead of the tax increases.[3] Businesses have to make absolute decisions, and many of them have decided not to hire or expand due to the higher taxes and business costs. This is rational and expected behavior when Speaker Nancy Pelosi (D–CA) and the House voted December 2 to triple the top tax rate on dividends next year.

Many businesses that are going to be affected by the tax hikes are small business owners who employ workers. Only about a quarter of individuals who report small business income on the individual tax return hire workers. However, 100 percent of these small business income owners with income over $1 million hire employees. Raising taxes on small business owners who actually employ workers is causing them to further delay hiring and expanding their payroll.

Uncertain Uncertainty

Congress cannot change the uncertainty the President has created by a capricious regulatory policy and will need to repeal Obamacare when the new Congress takes office next year. However, Congress can change the uncertainty over tax policy by quickly extending the 2001 and 2003 tax cuts. During a weak economic recovery with a sluggish labor market, tax hikes on businesses will only prolong this period of elevated unemployment rates.

Rea S. Hederman, Jr., is Assistant Director of and a Senior Policy Analyst and James Sherk is Bradley Fellow in Labor Policy in the Center for Data Analysis at The Heritage Foundation.