Economic freedom is key to addressing Mexico’s economic, security, and civil society concerns. Since President Enrique Peña Nieto began his single six-year term in December 2012, progress has been made in challenging the private and public monopolies and duopolies (and their labor unions) that have historically dominated and hampered huge portions of Mexico’s economy. More remains to be done, especially with regard to Mexico’s hydrocarbons industry.

Mexico’s protectionist and “state corporatist” combines benefit politically powerful rent-seekers in sectors such as energy, telecommunications, construction, food production, broadcasting, financial services, and transportation. They have long been a drag on competitiveness and job creation.

Despite being the third-largest oil producer in the hemisphere and the 10th-largest in the world, Mexico’s hydrocarbons industry has been in decline. The historic energy reforms implemented in August 2014 can open doors for foreign investment in Mexico’s oil and natural gas sectors, but the new hydrocarbons law is overly complicated and needs further revisions if it is to succeed. These modifications include the further streamlining of regulatory oversight and an even more diminished role for the state-owned oil company Pemex. Underperforming, inefficient, and corrupt state-owned enterprises (SOEs) are a major factor restraining development.

The U.S. government can assist Mexico by facilitating trade, regulatory reform, and infrastructure development—all of which will greatly benefit both countries—and by encouraging additional market-oriented reforms.

Mexico’s Oil and Gas Sector

Mexico nationalized its oil sector in 1938, and Petróleos Mexicanos (more commonly known as Pemex) was created as the sole oil operator in the country. Pemex became one of the largest non-publicly traded companies in the world, and the high taxes imposed on it provide close to one-third of total Mexican government revenue. The 1994 North American Free Trade Agreement (NAFTA) removed significant investment barriers and provided security for U.S., Mexican, and Canadian investors, but it specifically excluded the Mexican energy sector and reserved to the Mexican government the right to prohibit foreign investment in the sector.

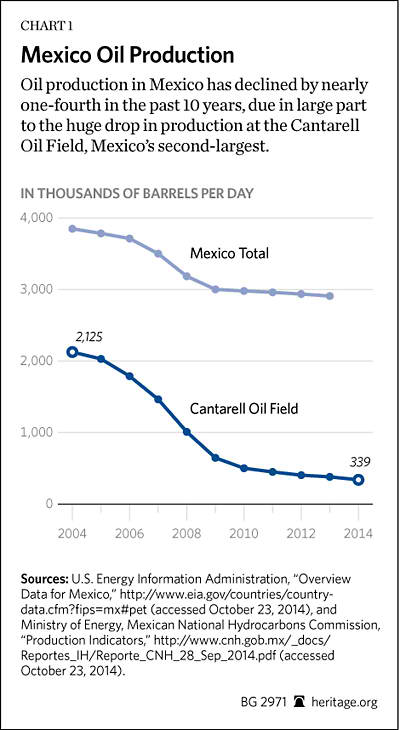

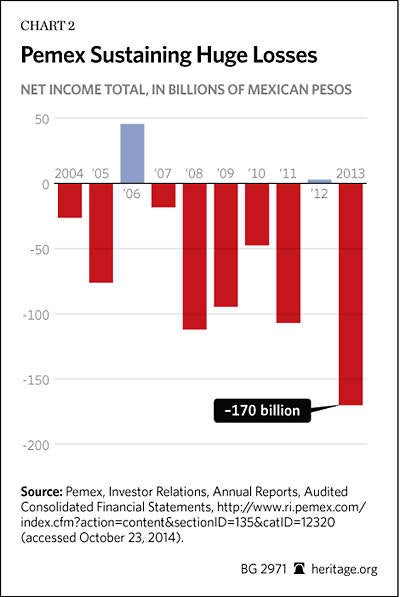

Pemex has been poorly managed for many years and has operated at a loss since 1998. Its debt burden has increased significantly, while its production has steadily declined—down 25 percent from 3.6 million of barrels per day (bpd) in 2004 to 2.5 million bpd in 2013. The company’s powerful labor union has imposed unsustainable pension liabilities on the company.

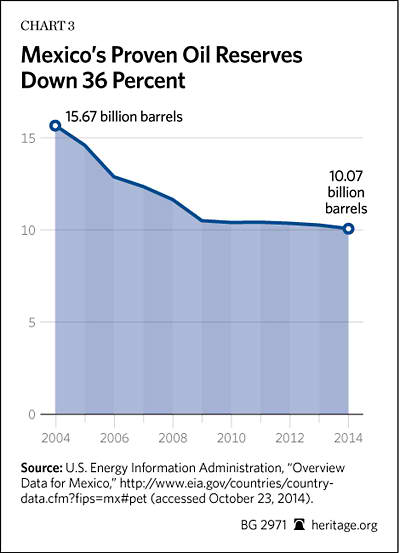

Notwithstanding significant quantities of untapped oil and gas reserves (especially deep offshore and in shale formations), Mexican crude oil production in 2013 reached its lowest point since 1995 and continues to decline in 2014. Today, less new oil is being found than is being produced by a factor of nearly one-third. Until Mexico began importing natural gas from the United States in large quantities,[1] electricity prices in Mexico were very high. Indeed, even today industrial electricity costs remain nearly 80 percent higher than in the U.S.[2]

It is urgent, therefore, that new sources of oil and gas be found and put into production, not only to sustain domestic consumption and export of petroleum products, but also to modernize those sectors and to create less expensive sources of clean fuel to generate electricity. Recent reforms of the country’s energy sector, particularly the hydrocarbons industries, are aimed at doing just that.[3]

Oil and Gas Infrastructure in Mexico

Pemex operates a pipeline network within Mexico of only approximately 3,000 miles that must connect major production centers with domestic refineries and export terminals. This network is clearly inadequate to service all areas of the country and transport the oil and gas from its source to the refineries and the market.

Until recently, Mexico had no international oil pipeline connections; most of its exports were shipped by tanker from three export terminals on the Gulf Coast. With the introduction of energy sector reforms and in conjunction with the opening of Mexico to imports of natural gas flows from the U.S. to Mexico, Pemex has launched an ambitious public-private-sector pipeline construction program on both sides of the border that could cost as much as $8 billion.

- Comisión Federal de Electricidad (CFE),[4] Mexico’s national electrical utility, is seeking bids for three natural gas pipelines that would originate in the U.S., two from the Waha gas hub in West Texas and one from Ehrenberg in Arizona.

- In late summer 2014, CFE entered into a deal with Energy Transfer Partners LP (ETP), to bring additional gas supplies from Texas to Mexico. ETP, a Dallas company, has said it will construct two new pipelines to handle the flow of gas.

Other pipeline construction projects underway include:

- Kinder Morgan, Inc., a Houston-based company, has built a $200 million, 60-mile-long gas pipeline (Sierrita Pipeline) from Tucson, Arizona, to Sasabe, Arizona, on the Mexican border. It is expected to go into service by the end of 2014 and will transport approximately 200 million cubic feet of gas per day. The Kinder Morgan pipeline will connect to a $1 billion network of pipelines in Mexico being built by IEnova, a subsidiary of Mexico’s Sempra Energy.

- Howard Mid-Stream Energy Partners, LLC, of San Antonio, Texas, recently requested permission from U.S. federal regulators to build a gas pipeline in Webb County, Texas, that could transport up to 1.12 billion cubic feet of gas per day to Mexico. Though the pipeline would cross an international border and thus require a permit from the U.S. government, it is not expected to run into delays such as those that have stalled the Keystone XL pipeline from Canada.

Mexico has six refineries, all operated by Pemex, that at the end of 2013 had a total refining capacity of approximately 1.54 million bpd. Pemex also controls 50 percent of the Deer Park Refinery in Texas that produces 334,000 bpd. In 2013, Pemex announced plans to build a $2.5 billion expansion of its Tula Refinery. It is also building a new $10 billion refinery to expand Mexico’s refining capacity.

Opening Mexico’s Oil and Gas Sector to Private Investment

The Hydrocarbon Law and Hydrocarbons Revenue Laws passed by Mexico’s Congress in December 2013 and the additional legislation signed into law on August 11, 2014, open the sector to private and foreign investment for the first time since 1938.

The law provides for new contract models for the exploration and production of oil and gas:

- Licensed Contracts. The contractor may take and own the hydrocarbons in kind at the wellhead and make royalty payments as the oil and gas is marketed.

- Production-Sharing Contracts. The contractor pays a percentage of operating profits and retains in-kind production with a value equal to the recoverable costs and its share of operating profits. The state’s share of production is delivered to the marketing firm retained by the National Hydrocarbons Commission (CNH).

- Profit-Sharing Contracts. The contractor delivers all the production to the marketing firm retained by the CNH, which pays the contractor its share.

- Service Contracts. The contractor delivers all production to the state, which will then pay the contractor its share. Previously, only service contracts in which companies were paid for services were permitted, and companies were not allowed shares or profits derived from the hydrocarbon resources.

Other key elements included in the legislation:

- Maintaining state ownership of sub-soil hydrocarbon resources, but allowing companies to take ownership of these resources once they are extracted and to book reserves for accounting purposes;

- Opening refining, transport, storage, natural gas processing, and petrochemicals sectors to private investment;

- Transforming Pemex into a productive state enterprise with an autonomous budget and a board of directors that does not include union representatives;

- Strengthening four Mexican federal entities with regulatory roles in the hydrocarbons industry: the Ministry of Energy (Secretaría de Energía de México or SENER), the Ministry of Finance, the CNH, and the Energy Regulatory Commission;

- Creating a National Center of Natural Gas Control; and

- Establishing a sovereign wealth fund, the Mexican Petroleum Fund, for stabilization and development, to be managed by the Central Bank.

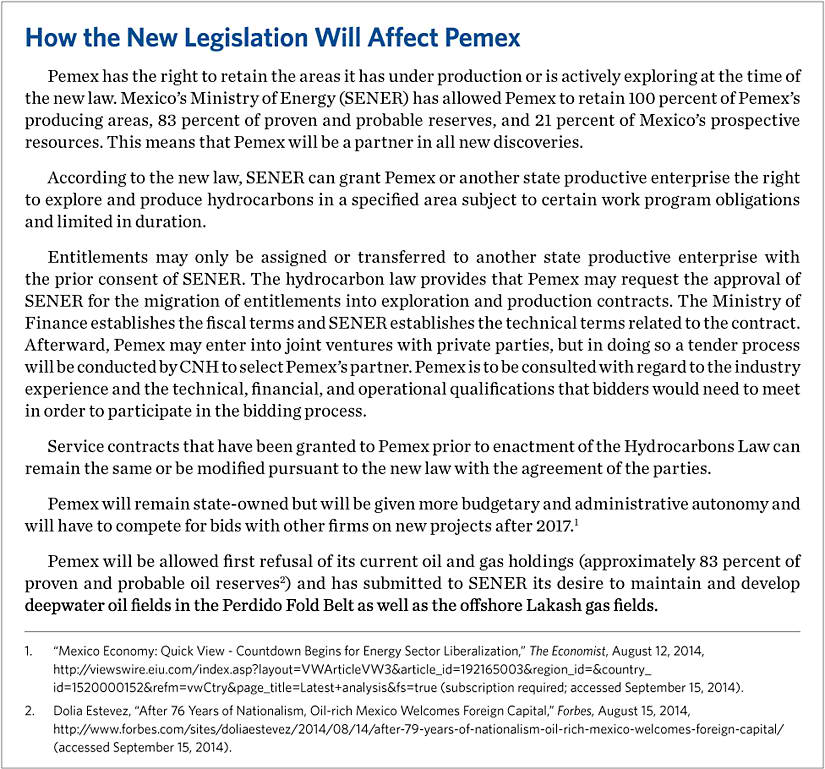

Except for the entitlements granted to Pemex, exploration and production (E&P) contracts will only be granted through a competitive bidding process organized and regulated by SENER, the Ministry of Finance, and the CNH. In this process, SENER will select areas for public bidding and establish the technical and financial qualifications for bidders; the CNH will conduct the bidding process, evaluate bids, and award contracts; and the Ministry of Finance will establish the economic and fiscal terms of the E&P contracts. For E&P activities, the Hydrocarbons Law establishes two different regimes to be regulated by the CNH: entitlements granted to state productive enterprises (such as Pemex) and E&P contracts entered into with private parties or state enterprises. For midstream and downstream activities, the law establishes a permit regime to be generally regulated by SENER and the Energy Regulatory Commission. The executive branch is expected to issue regulations no later than February 2015.

Benefits of the New Law for the Mexican Economy

Reform of the Mexican energy sector is likely to lead to a renaissance of Mexican oil and gas production. With ample reserves, foreign investment in Mexico’s oil and gas sector, particularly by experienced and nearby U.S. companies, will greatly benefit Mexico, especially in the development of the country’s shale oil and gas. The Mexican government predicts that the opening of the energy sector will result in approximately $50 billion in new investments between 2014 and 2018.[5]

Pemex estimates that it could earn between $25 billion and $60 billion as a result of joint ventures it will now be permitted to undertake with international oil and gas companies, while the Manhattan Institute for Policy Research says 2.5 million jobs and more than $1 trillion in revenue could be created by 2025.[6] These figures may be inflated, but there is no question that energy reform will boost oil and gas production in Mexico.[7] With successful energy-sector reforms in Mexico, the U.S. Energy Information Administration (EIA) estimates that oil production could rise to 3.7 million bpd by 2040. A year ago, the EIA estimated that Mexican oil production would likely reach 2.0 million to 2.1 million bpd by 2040.

U.S. companies have developed cutting-edge technology in directional drilling and producing oil and gas from shale formations that have significantly increased U.S. oil and gas production in recent years. In 2000, U.S. shale gas production accounted for about 1 percent of total gas production in the country. By 2010 that percentage had increased to 20 percent. The EIA predicts that shale gas production in the U.S. will account for 46 percent of all U.S. gas production by 2035.

The EIA estimated that 29 percent of total oil production in the U.S. in 2013 came from shale formations. In the fourth quarter of 2013 alone, the U.S. produced more than 3.2 million barrels of shale oil each day—more than 40 percent of total U.S. oil production and 4.3 percent of total global oil production. U.S. crude oil production is now 10.4 percent of the total global oil supply.[8]

Mexican energy reform will open opportunities for U.S. energy and service infrastructure companies that are seeking new markets. Increased production in Mexico will lead to lower energy costs for Mexican consumers and manufacturers and perhaps make Mexico energy independent. The U.S. will benefit from the creation of a stable and secure new energy source on our southern border. In addition, a stronger Mexican economy and more opportunity for Mexican workers will likely further decrease the flow of illegal immigrants from Mexico to the U.S.

Mexico’s commitment to energy reform has already had positive effects on the country’s economy. The value of the Mexican peso has increased and, with the prospect of increased oil and gas production leading to lower energy costs, Mexico’s increased competitiveness will greatly benefit the manufacturing sector.

U.S. companies will further benefit by increasing their business in a neighboring country and may develop new techniques from drilling and producing oil and gas from shale formations that may be different from those in the U.S.

If the shale oil and gas resources in Mexico prove to be extensive, there will need to be an expanded oil and gas pipeline system in Mexico. The Mexican government recognizes this and has already begun investing in its oil and gas infrastructure.

What Should the Mexican Government Do?

With the discovery of oil and gas in shale formations and the development of technology to recover oil and gas from these formations, the U.S. today has a surplus of gas and is approaching oil independence. Mexico has yet to develop its shale oil and gas industry but, if Mexican reserves are as extensive as estimated, increased production of shale energy can contribute greatly to Mexico’s goal of energy independence.

The Mexican government should:

- Remove barriers to foreign investment in the Mexican energy market. Mexico does not currently have the drilling expertise and technology to explore for and produce oil and gas from shale formations. Because of this, President Peña Nieto and his administration have amended Mexico’s oil and gas laws to encourage U.S. and other foreign companies to participate in the development of Mexican oil and gas resources. Nevertheless, barriers to foreign companies entering the oil and gas market in Mexico remain.

- Remove Pemex’s remaining monopolistic power. Prior to recent changes in the law, Pemex essentially had a monopoly on oil and gas development in Mexico. The Peña Nieto administration, in its amendment of the oil and gas laws, took much of the monopolistic power away from Pemex, but it still retains the areas it has under production or was actively exploring at the time of the new law, allowing Pemex 100 percent of producing areas and 83 percent of proven and probable reserves. Pemex will also have a percentage of prospective oil and gas resources, which means that Pemex will always be a partner in new discoveries.

- Simplify the energy market regulatory structure. Even under the new hydrocarbons law, the regulation of oil and gas production by the government of Mexico remains overly complicated and divided among three agencies. Exploration and production contracts are still only granted through a competitive bidding process organized and regulated by the SENER, the Ministry of Finance, and the CNH. Dealing with three separate agencies will be cumbersome, time-consuming, and expensive for foreign oil and gas companies.

- U.S. and other foreign companies with experience in exploring for and producing oil and gas from shale formations are extremely busy elsewhere and will be reluctant to enter the Mexican market if the regulations are too onerous. Mexico should combine these activities under one agency or create a process by which the three agencies have representatives to expedite the applications from interested foreign or private domestic companies.

- Implement a transparent regulatory framework. Mexico should implement a transparent regulatory framework as soon as possible and make contract terms attractive to foreign investment. The percentage interest set aside for Pemex in new discoveries (21 percent) will constitute a deterrent to foreign direct investment. Also, whether Pemex will also be required to contribute 21 percent of any costs associated with developing these new discoveries remains an open question. The Mexican government should reduce the Pemex cut of any new production and clarify the question of cost sharing.

What Should the U.S. Government Do?

The U.S. can assist Mexico and increase gas trade between the two countries by:

- Facilitating the issuance of cross-border pipeline licenses. U.S. regulators can also provide technical assistance to their Mexican counterparts as they transform their country’s energy sector to a more competitive, market-oriented system.

- Increasing its cooperative efforts to assist Mexico in the fight against the cartels. The Mexican government needs to continue its battle against organized crime and ensure that the pipeline and other oil and gas infrastructure is secure. Pemex estimates that it loses approximately $5 billion a year in illegal taps. The Burgos basin area in northern Mexico is dominated by the Mexican drug cartels, which may prove to be a problem until Mexico gains control of the area.