The current budgetary treatment of Fannie Mae and Freddie Mac as off-budget federal entities, meaning that they are excluded from budgeting rules and processes, creates deficit reduction in appearance only with several ill effects. The current cash-flow approach used to report the impact of government-sponsored enterprises (GSEs) on federal finances fails to account properly for taxpayers’ exposure to risk from federal control of Fannie and Freddie. The result is that the entities appear to be a boon for taxpayers because they reduce the reported federal deficit. This fiscal illusion encourages higher federal spending today while putting taxpayers on the hook for future bailouts. Moreover, improper accounting of Fannie and Freddie’s impact on taxpayers hurts efforts to eliminate the GSEs.

The Budget and Accounting Transparency Act of 2014 (H.R. 1872) would address problems with the current accounting for Fannie Mae and Freddie Mac by putting both entities on-budget and calculating their cost to taxpayers by incorporating market risk through a fair-value accounting.[1] This is an important first step toward GSE elimination.

Brief History

The Federal National Mortgage Association (Fannie Mae) and Federal Home Loan Mortgage Corporation (Freddie Mac) are government-sponsored enterprises under conservatorship by the Federal Housing Finance Agency (FHFA). Both entities participate in the secondary mortgage market by buying mortgages and subsequently repackaging and reselling these mortgages as mortgage-backed securities (MBSs) or holding them as part of their portfolio.

Prior to September 2008, the GSEs were shareholder-owned, supposedly private entities which benefited from a direct line of credit with the Treasury and exemptions from Securities and Exchange Commission filings and from state and local income taxes.[2] However, the entities were long seen as benefiting from an implicit government guarantee—a guarantee which has since been made explicit.

The Housing and Economic Recovery Act allowed the FHFA to place Fannie and Freddie in conservatorship, and it allowed the Treasury to provide financial assistance to the entities to prevent their net worth from falling to zero.[3] In short, the government took control of Fannie and Freddie and agreed to shield the entities from bankruptcy. Treasury support for the GSEs comes in the form of senior preferred stock purchases, meaning that the Treasury buys GSE stock with a higher claim on earnings than common stock; since August 2012, Treasury has been entitled to all GSE profits.[4]

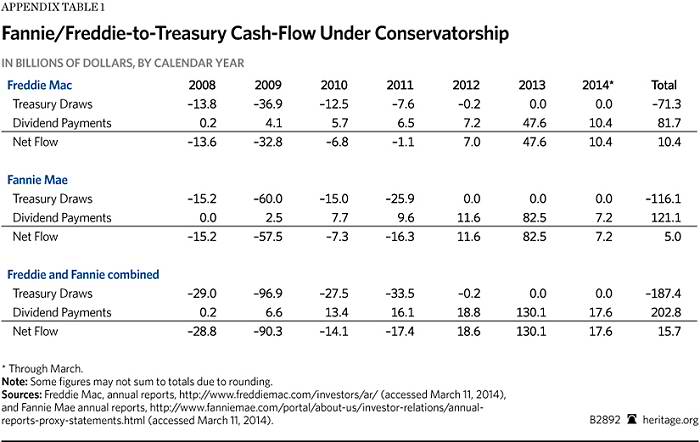

Since the federal government takeover of Fannie Mae and Freddie Mac in September 2008, taxpayers have funneled $189 billion into the government-sponsored enterprises.[5] In 2012, this revenue stream reversed with Fannie and Freddie paying more than $203 billion to the U.S. Treasury since then.[6] The mortgage giants nevertheless remain under federal control as the Treasury has instead laid claim to all of the GSEs’ profits for an indefinite time.

Fannie and Freddie’s Impact on the Budget

The White House Office of Management and Budget (OMB) and the Congressional Budget Office (CBO) differ significantly in their budgetary treatment of Fannie Mae and Freddie Mac.

The GSEs are treated as off-budget entities by the OMB because they are considered separate private entities under temporary federal conservatorship. Sarah Rosen Wartell of the Center for American Progress Action Fund explained the OMB’s position in a hearing before the Committee on the Budget:

According to the 1967 Commission on Budget Concepts, inclusion of an entity’s assets and liabilities in the federal budget depends on three basic factors: ownership, control, and permanence. Under the terms of the Housing and Economic Recovery Act of 2008, FHFA as conservator may take any action that is necessary to return Fannie Mae and Freddie Mac to sound and solvent condition and to preserve and conserve the assets of these firms.… [I]t seems difficult to conclude that the current arrangement between Treasury and the GSEs is permanent.[7]

The problem is that it is not clear whether and how Fannie and Freddie would return to stockholder control. The conservatorship agreement over Fannie and Freddie is remarkably unspecific when it comes to the future fate of the GSEs. Until the firms reach a “sound and solvent condition,”[8] the FHFA may continue to hold Fannie and Freddie under conservatorship. With no clear exit clause, Fannie and Freddie could remain under government control until Congress acts to change their status.[9] Therefore, the arrangement between Treasury and the GSEs should be considered permanent for budgetary purposes.

The CBO projects the GSEs’ impact on the federal budget as if Fannie and Freddie were government entities. According to Deborah Lucas, the CBO’s Assistant Director for Financial Analysis, the

federal conservatorship of Fannie Mae and Freddie Mac and their resulting ownership and control by the Treasury make the two entities effectively part of the government and imply that their operations should be reflected in the federal budget.[10]

This inconsistency between Administration and congressional accounting of Fannie and Freddie’s impact on the budget creates budgetary confusion and has resulted in seeming deficit reduction with adverse consequences for spending restraint.

Budgetary Confusion

In its current Budget and Economic Outlook, the CBO presents a 10-year baseline for government spending, revenues, and deficits.[11] The report also includes actual figures for the past fiscal year and estimates for the current fiscal year. In its reporting of actual outlays in the preceding fiscal year and its estimates for the current fiscal year, the CBO adopts Treasury’s cash-flow method to record Fannie and Freddie’s budgetary impact. In other words, official government scorekeepers only take account of money flowing into the Treasury from the GSEs, or vice versa, while ignoring the budgetary costs of guaranteeing GSE mortgage-backed securities—a cost they would acknowledge if the GSEs were on-budget as other federal loan guarantees are. In its baseline budget projections, however, the CBO does account for the subsidy cost of Fannie and Freddie’s activities in a forward-looking basis.

By the cash-flow method, Fannie Mae and Freddie Mac reduced 2013 outlays and the deficit by $97 billion.[12] This is misleading, however, as this method accounts only for cash transfers between the Treasury and the GSEs, such as stock purchases made by Treasury and dividends paid to the Treasury. The method ignores the risk to taxpayers from backing GSE mortgage guarantees and fails to recognize the substantive taxpayer subsidy provided to the secondary mortgage market through Fannie Mae and Freddie Mac operations under federal control. As Lucas testified before Congress in 2011:

That [cash-flow] approach can postpone for many years the recognition of the costs of new obligations. Subsidized mortgage guarantees may even show gains for the government in the short-term because fees are collected up front but losses are realized over time as defaults occur.[13]

Today, the GSEs are paying dividends to the Treasury that are reducing recorded outlays and recorded deficits, while taxpayers are on the hook for future losses.

In its baseline projections through 2024, the CBO calculates the GSEs’ impact on the budget by projecting the subsidy costs of credit assistance offered by Fannie Mae and Freddie Mac over the lifetime of the securitized mortgage guarantees. To incorporate the market risk associated with the GSEs, the CBO calculates their subsidy cost using a fair-value basis. Using this approach, the CBO estimated that the GSEs would have had a net outlay effect of $5 billion in 2013.[14] Considering the GSEs as on-budget entities, their profits paid to Treasury would have been considered an intra-governmental payment with no effect on reported net outlays and the deficit.

Instead of recording a $5 billion cost for maintaining Fannie and Freddie under federal conservatorship, Treasury recorded a $97 billion offsetting receipt.[15] This means that Treasury did not record GSE payments to the government as revenues, but subtracted the value from federal spending as an offsetting receipt. This lowered reported spending in 2013 by $97 billion and reduced the deficit by that same amount.

Higher Spending Today, Taxpayer Bailout Tomorrow

Were Fannie Mae and Freddie Mac considered to be on-budget entities, the federal government would have reported $3.6 trillion in spending and a $780 billion deficit in 2013. Instead, government spending was effectively underreported by about $100 billion. As the CBO reported in its most recent Budget Outlook, “The decline in outlays between 2012 and 2013 resulted primarily from transactions between the Treasury Department and Fannie Mae and Freddie Mac.”[16] If the OMB continues to treat Fannie and Freddie as off-budget entities, spending in 2014 will once again be underreported. The CBO projects that GSE payments to the Treasury will reduce reported federal outlays and the deficit by $81 billion in 2014.[17]

Just a few months after the Treasury released its figures for fiscal year (FY) 2013, Congress engaged in negotiations to weaken the Budget Control Act’s spending caps for 2014. The final deal struck between Budget Committee chairmen Representative Paul Ryan (R–WI) and Senator Patty Murray (D–WA) increased spending by $63 billion over two years.[18] Undoubtedly, rosy reporting considering short-term improvements in federal spending and the deficit played a role in the decision to increase spending immediately for promised spending reductions in the future.[19]

Failure to consider the GSEs’ mortgage guarantees in budget reporting puts taxpayers on the hook for a taxpayer bailout of mortgages in the future without accounting for those risks today. Taxpayers are ultimately responsible for the nearly $4 trillion in GSE guarantees.[20]

The Congressional Budget Office makes a good- faith attempt to account for the GSEs’ risk to taxpayers by projecting their cost using accrual accounting and a fair-value approach. Accrual accounting captures the lifetime cost of mortgage guarantees and loans at the time when the government takes on the additional responsibility. Fair-value accounting seeks to incorporate the market risks to the taxpayer associated with federal mortgage loan guarantees. For the 2015–2024 period, the CBO projects, the costs for new guarantees and loans held by the GSEs will be $19 billion.[21]

It is important to acknowledge that while the CBO uses a formula to project the budgetary cost of GSE activities, its cost estimate, too, is limited. It does not capture the economic costs of government involvement in the housing market and the extent to which such involvement distorts economic behavior and encourages investment in the housing sector at the expense of other parts of the economy.

Putting the GSEs On-Budget—Toward Their Elimination

Short of their immediate elimination, putting the GSEs on-budget to account for the risks that taxpayers bear from Fannie Mae’s and Freddie Mac’s involvement in the mortgage market is an important first step. The Budget and Accounting Transparency Act of 2014 would accomplish this goal, requiring that “the federal budget reflect the net impacts of programs administered by Fannie Mae and Freddie Mac.”[22]

Given the current accounting treatment of the GSEs by the Obama Administration’s OMB, were Congress to eliminate Fannie Mae and Freddie Mac effective in 2014, the budget would record an $81 billion increase in spending and deficits. While the official record seems to indicate that GSE elimination would worsen the U.S. fiscal situation, common sense suggests that relieving taxpayers of future mortgage guarantee liabilities would improve the budget picture.

If Fannie Mae and Freddie Mac were accounted for on a fair-value basis as on-budget entities, their elimination would rightly show a reduction in spending and the deficit. This is because a fair-value approach would show that taxpayers are subsidizing the GSEs by accounting for their activities over the lifetime of the mortgage guarantees and loans that they issue and by incorporating due market risk.

Moreover, putting the GSEs on-budget would eliminate the billions of dollars in seeming windfall payments the Treasury is receiving from Fannie Mae and Freddie Mac today. In 2013, the GSEs reduced reported spending and deficits by $97 billion. An additional $81 billion windfall is expected in FY 2014, bringing the total cash flow from the GSEs to Treasury to $178 billion in two years. This would also mean that federal spending was underreported by $178 billion for two years, as GSE profits are counted as offsetting receipts, which reduce reported outlays. In contrast, had the GSEs been treated as on-budget entities, the budget would have recorded a $9 billion cost. Thus, spending was effectively underreported by $187 billion.

Lower reported spending and deficit figures are encouraging lawmakers to increase spending and neglect entitlement reform. In the months since Congress and the Administration agreed to raise spending by an additional $63 billion with the Ryan–Murray budget deal, President Obama has further taken any semblance of grand bargain negotiations off the table and is instead pushing for higher spending in his 2015 budget proposal.

An Important Step for Fiscal Restraint and GSE Elimination

Improper accounting in the budget for the downside risks that the GSEs pose for American taxpayers is creating the illusion that the GSEs are a free lunch for Washington. Fannie Mae’s and Freddie Mac’s profits are creating adverse incentives for controlling spending and the debt.

Putting the GSEs on-budget would show taxpayers and Congress that Fannie Mae and Freddie Mac impose a real cost on taxpayers and that eliminating the GSEs would improve federal finances. Proper accounting of the GSEs’ impact on the federal budget is an important step toward their—very necessary—elimination.

—Romina Boccia is Grover M. Hermann Fellow in Federal Budgetary Affairs in the Thomas A. Roe Institute for Economic Policy Studies at The Heritage Foundation.