With the new federal tax relief for 529 accounts, many families are wondering if their state will extend tax relief under their laws for K–12 private school tuition expenses. The 2017 law amended 26 U.S.C. § 529(c), adding “expenses for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school” to the definition of “qualified higher education expense.”1This subsection of the statute deals with tax treatment of 529 accounts for designated beneficiaries and contributors under federal law, and the amended language makes clear that it only changes subsection (c) of the federal statute. The general definitions section of the statute, § 529(e), defines “qualified higher education expenses” and does not include K–12 private or religious schools.

Many states point to § 529(e) in their laws, and some of these states have extended the federal tax break through guidance issued by the state’s treasurer or 529 plan. Other states generally reference any qualified expenses found in § 529, and some states are interpreting this section to extend the federal tax break under their laws. State lawmakers should revise statutes to make clear that 529 accounts may be used for any expenses authorized by any section of 529. States should not rely on guidance from the state’s treasurer or 529 plan that conflicts with the plain text of their statutes and instead should amend those statutes to automatically align with any future changes to this section of federal code.

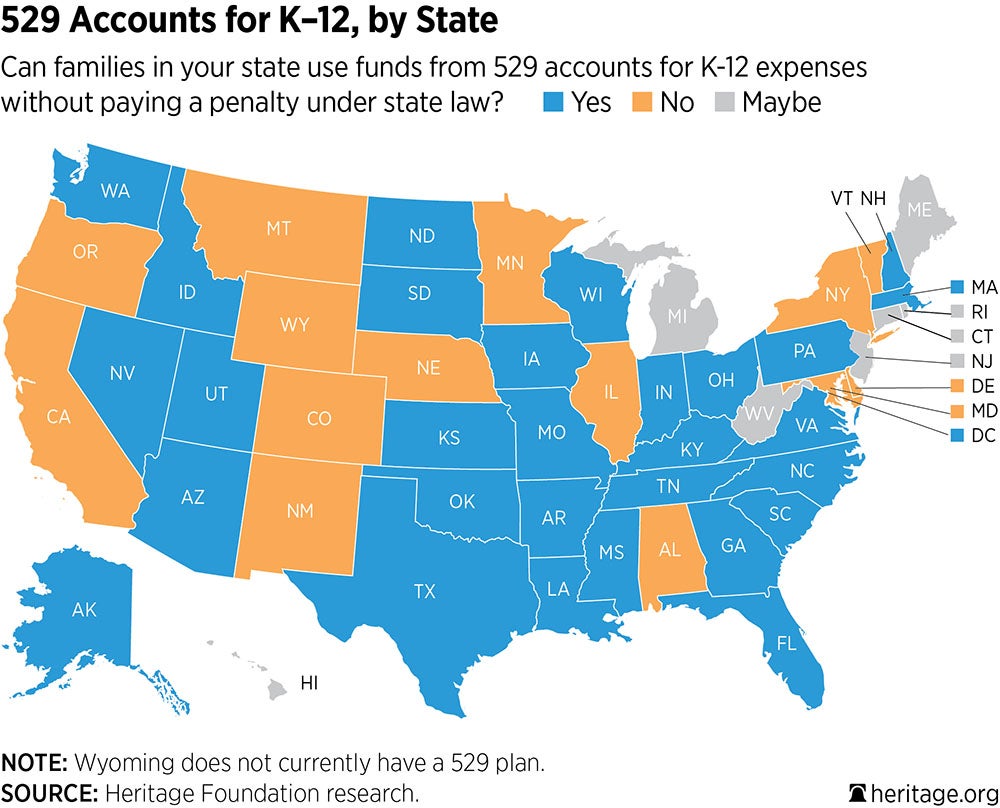

Below is a look at the status of 529 accounts in every state.

Can Families in Your State Use Funds from 529 Accounts for K–12 Expenses Without Incurring Penalties Under State Law?2

- Alabama. No. In January 2018, H.B. 251 was introduced in the Alabama House of Representatives and would have aligned with the amended federal language. By the time H.B. 251 passed in March, that language had been stripped from the bill. The Alabama Department of Revenue advises that “qualified higher education expenses” are those defined in section 529, while the Office of the State Treasurer indicates that funds may only be used at an “eligible educational institution” and the definition under section 529 does not include K–12 schools.3

- Alaska. Yes. Alaska does not have personal income tax, so there would not be a state tax penalty.

- Arizona. Yes. In 2019, Gov. Doug Ducey signed S.B. 1349, which changed the definition of “qualified higher education expenses” to include “tuition to enroll in or attend an elementary or secondary public, private or religious school pursuant to section 529 of the internal revenue code.”4

- Arkansas. Yes. Arkansas amended its law this year, defining qualified higher education expenses as “tuition and other permitted expenses as set forth in 26 U.S.C. § 529, as in effect on January 1, 2018.”5

- California. No. California law states that qualified higher education expenses are “expenses of attendance at an institution of higher education as provided in paragraph (3) of subsection (e) of Section 529 of the Internal Revenue Code of 1986, as it is amended from time to time, if, as determined by the board, the amendment is consistent with the purposes of this article.”6

- Colorado. No, although Colorado has indicated this is under legal review. Colorado law states that qualified higher education expenses “has the same meaning as that term is defined in section 529 of the internal revenue code.”7

- Connecticut. Maybe. Connecticut law states that qualified higher education expenses include “tuition, fees, books, supplies and equipment required for the enrollment or attendance of a designated beneficiary at an eligible educational institution, including undergraduate and graduate schools and any other higher education expenses that may be permitted by Section 529.”8

- Delaware. No. Delaware law states that qualified higher education expenses include “tuition and other permitted expenses as presently set forth in 26 U.S.C. § 529(e) or as hereafter permitted by such successor or amended section for the enrollment or attendance of a designated beneficiary at a higher education institution.”9

- Florida. Yes. Florida does not have personal income tax. Florida law states that qualified higher education expenses are set by the Florida Prepaid College Board, consistent with the Internal Revenue Code.10

- Georgia. Yes. On April 3, 2018, the Georgia Path2College 529 Plan announced distributions made for K–12 tuition at public, private, or religious schools are income tax free “up to a maximum of $10,000 of distributions” per taxable year.11

- Hawaii. Maybe. Hawaii law states that qualified higher education expenses include “any qualified higher education expense defined in section 529 of the Internal Revenue Code.”12

- Idaho. Yes. In March 2018, the state amended its law to align with the federal change, stating that qualified higher education expenses “shall have the meaning provided in 26 U.S.C. section 529.”13

- Illinois. No. Illinois law defines “qualified expenses” as “tuition, fees, and the costs of books, supplies, and equipment required for enrollment or attendance at an eligible educational institution.” “Eligible educational institutions” include public and private colleges, junior colleges, graduate schools, and certain vocational institutions.14

- Indiana. Yes. In May 2018, the state amended its law to include “tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school located in Indiana and…permitted under Section 529 of the Internal Revenue Code.”15

- Iowa. Yes. In May 2018, the Iowa legislature amended its definition of “qualified education expenses” to include “elementary and secondary school expenses for tuition described in section 529(c)(7) of the Internal Revenue Code.”16

- Kansas. Yes. Kansas law states that qualified higher education expenses are any expenses included in section 529 of the Internal Revenue Code, “as amended.”(FN 17) The Kansas Department of Revenue released a memo confirming that residents can use 529 accounts for K-12 expenses.17

- Kentucky. Yes. In July, the state amended its definition of qualified educational expenses to include “tuition of up to…$10,000 per year in connection with enrollment or attendance at an elementary or secondary public, private, or religious school.”18 The state has instructed the company that manages 529 plans for Kentucky and several other states to “take measures to modify… account withdrawal request forms to allow account owners…to permit direct payments to K-12 schools.”19

- Louisiana. Yes. The state legislature passed a law in May 2018 creating a new program that allows families to save for public or private elementary and secondary school.20 While that program is being set up, families that had already opened a plan with the state’s Student Tuition Assistance and Revenue Trust before December 31, 2017, are authorized to make a one-time withdrawal of $10,000 or less to pay for elementary or secondary schools.

- Maine. Maybe. Maine law states that “higher education expenses” are “certified expenses for attendance at an institution of higher education as those expenses are defined by…the Internal Revenue Code.”21

- Maryland. No. Maryland law states that “qualified higher education expenses” are limited to expenses defined in “529(e) of the Internal Revenue Code.”22

- Massachusetts. Yes. Although Massachusetts law limits qualified higher education expenses to those defined in “26 U.S.C. 529(e)(3),”23 U.Fund, Massachusetts’ 529 plan, indicates that “up to $10,000 per year can be applied toward K-12 tuition expenses.”24

- Michigan. Maybe. Michigan law says “qualified higher education expenses” are those “defined in section 529 of the Internal Revenue Code.”25

- Minnesota. No. Minnesota law states “qualified higher education expenses” are those “defined in section 529(e)(3) of the Internal Revenue Code,” and a “qualified distribution” means “a distribution made from an account for qualified higher education expenses of the beneficiary.”26

- Mississippi. Yes. Mississippi defines qualified higher education expenses as “any higher education expense defined in Section 529 of the Internal Revenue Code.”27The State Treasurer indicates that the federal change “appl[ies] to MACS” (Mississippi Affordable College Savings Program).28

- Missouri. Yes. Although Missouri law states that “qualified higher education expenses” are the “qualified costs of tuition and fees and other expenses for attendance at an eligible educational institution, as defined in Section 529(e)(3) of the Internal Revenue Code,” Missouri’s 529 Savings Plan indicates that “Missouri taxpayers can use MOST 529 assets to pay for expenses for tuition in connection with enrollment or attendance for K–12 with no state tax consequences.”29

- Montana. No. Montana law states that “qualified higher education expenses” are those “defined in section 529(e)(3) of the Internal Revenue Code.”30

- Nebraska. No. Nebraska law defines “qualified higher education expenses” as “certified costs of tuition and fees, books, supplies, and equipment required for enrollment or attendance at an eligible educational institution.”31Nebraska State Treasurer Don Stenberg indicated that “withdrawals from NEST accounts to pay for K–12 tuition will be considered non-qualified withdrawals under current state law.”32

- Nevada. Yes. Nevada does not have personal income tax.

- New Hampshire. Yes. New Hampshire does not have personal income tax.

- New Jersey. Maybe. New Jersey law states that “qualified higher education expenses” are those “described in paragraph (3) of subsection (e) of section 529 of the federal Internal Revenue Code,” but New Jersey’s Treasurer released a statement saying, “Because New Jersey law incorporates the provisions of IRC section 529, New Jersey follows the federal expansion and considers a withdrawal from an IRC section 529 savings plan used for tuition at private, religious, elementary, and secondary schools a qualified higher education expense for New Jersey Gross Income Tax purposes.”33

- New Mexico. No. New Mexico law references “qualified higher education expenses, as defined pursuant to Section 529 of the Internal Revenue Code.”34The New Mexico Education Trust Board asked the state’s taxation and revenue department to review the change in federal law and issue an advisory letter on its impact on state law. The department indicated that state law “does not provide an exemption from New Mexico State income tax” for 529 withdrawals for K–12 tuition.35

- New York. No. New York law states that “qualified higher education expenses” are “any qualified higher education expense included in section 529 of the Internal Revenue Code.” The New York Department of Taxation and Finance notes that “K–12 distributions would not be considered qualified distributions under New York statutes and would require the recapture of any New York State tax benefits that accrued on contributions.”36

- North Carolina. Yes. The North Carolina legislature amended its law as part of its budget bill—over the veto of Governor Roy Cooper. The law states that Parental Savings Trust Fund accounts may be used for “the costs of education expenses of eligible students in accordance with section 529 of the Code.”37

- North Dakota. Yes. Although the state defines “qualified higher education expenses” as those that are “defined in section 529 of the Code,” College SAVE, the state’s 529 Plan, indicates that “North Dakota taxpayers can use College SAVE 529 assets to pay for expenses for tuition in connection with enrollment or attendance for K–12 with no state tax consequences.”38

- Ohio. Yes. The state amended its law in March 2018 “to allow tax deductible contributions to Ohio 529 plans for K–12 education expenses.” It provides that “higher education expenses” are those “that meet the definition of ‘qualified higher education expenses’ under section 529 of the Internal Revenue Code.”39

- Oklahoma. Yes. Oklahoma law states that “qualified higher education expenses” include “tuition, fees, books, supplies, and equipment required for the enrollment or attendance of a designated beneficiary at an eligible educational institution.”40The state’s College Savings Plan noted: “Effective January 1, 2018, distributions for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school are Oklahoma and federal income tax free up to a maximum of $10,000 of distributions for such tuition expenses per taxable year.”41

- Oregon. No. The state legislature passed a law in June stating, “If a taxpayer makes a withdrawal from a savings network account for higher education…to pay expenses in connection with enrollment or attendance at an elementary or secondary school, the amount of the withdrawal that is attributable to contributions that were subtracted from federal taxable income under ORS [Oregon Revised Statute] 316.699 and the amount of the withdrawal that is attributable to previously untaxed earnings and gains” will be added to federal taxable income.42

- Pennsylvania. Yes. Pennsylvania defines “qualified higher education expenses” as those expenses “defined by section 529 of the Internal Revenue Code.”43PA 529, the state’s College Savings Program, indicates that 529 funds may be used “to pay for expenses for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school up to $10,000 per year, per beneficiary.”44

- Rhode Island. Maybe. Rhode Island law defines “qualified higher education expenses” as “tuition, fees, books, supplies and equipment required for enrollment or attendance at an institution of higher education, and other education costs defined by federal law.”45

- South Carolina. Yes. South Carolina law states that “qualified higher education expenses” are “any higher education expense defined in Section 529 of the Internal Revenue Code.” Future Scholar, South Carolina’s College 529 Savings Plan, notes, “Effective January 1, 2018, families may withdraw up to an aggregate of $10,000 a year per beneficiary tax free to cover K–12 tuition at public, private, or religious elementary or secondary schools…. There is not a distinction between K–12 withdrawals and withdrawals to a college or university.”46

- South Dakota. Yes. South Dakota does not have personal income tax. South Dakota defines “qualified higher education expenses” as “tuition, fees, books, supplies, and equipment required for enrollment or attendance…at an eligible education institution, and any other expenses qualifying as a qualified higher education expenses under section 529 of the Internal Revenue Code.”47

- Tennessee. Yes. Tennessee does not have personal income tax.

- Texas. Yes. Texas does not have personal income tax.

- Utah. Yes. Although Utah law states that “higher education costs” are “qualified higher education expenses as defined in Section 529(e)(3),”48the state’s my529 indicates that “Utah residents … will not face a recapture of previously claimed Utah state income tax benefits if they withdraw up to … $10,000… to pay for K-12 tuition expenses at public, private, and religious schools.”49

- Vermont. No. Vermont law defines “postsecondary education costs” as “the qualified costs of tuition and fees and other expenses for attendance at an institution of postsecondary education, as defined by the Internal Revenue Code.”50The Vermont Higher Education Investment Plan notes that withdrawals for K–12 tuition expenses “may be subject to a 10% [sic] recapture penalty…and tax on the gain realized with respect to the withdrawals.”51

- Virginia. Yes. Virginia law states that college savings trust account funds may be used for “qualified higher education expenses at eligible educational institutions, as both such terms are defined in § 529 of the Internal Revenue Code.”52Virginia 529 indicates that funds may be used for private or religious K–12 tuition.53

- Washington. Yes. Washington does not have personal income tax.

- Washington, DC. Yes. Although DC’s law indicates that qualified higher education expenses “shall have the same meaning as in section 529(e)(3) of the Internal Revenue Code,”54the DC College Savings Plan says, “Account owners can treat withdrawals for K-12 tuition expenses as ‘qualified higher education expenses’ with respect to both the federal and DC tax benefit.”55

- West Virginia. Maybe. West Virginia law defines “qualified higher education expenses” as those “permitted under 26 U.S.C. § 529.”56

- Wisconsin. Yes. Edvest, Wisconsin’s College Savings Plan, notes that “distributions for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school are federal and Wisconsin income tax free up to a maximum of $10,000 of distributions for such tuition expenses per taxable year per Beneficiary.”57

- Wyoming. Wyoming does not currently have a 529 plan.

—Jonathan Butcher is Senior Policy Analyst in the Center for Education Policy of the Institute for Family, Community, and Opportunity at The Heritage Foundation, and Elizabeth Slattery is Legal Fellow in the Edwin Meese III Center for Legal and Judicial Studies at The Heritage Foundation.

ENDNOTES:

-

U.S. Code § 529 (c)(7).

-

This paper is for informational purposes only and is not intended to serve as tax or legal advice. You should consult a tax or legal advisor to determine the impact of the federal and state laws on your particular situation.

-

See Alabama Department of Revenue, “Alabama 529 Savings Plan FAQ,” https://revenue.alabama.gov/individual-corporate/alabama-529-savings-plan-faq/ (accessed November 3, 2018), and Office of Alabama State Treasurer, “CollegeCounts 529,” http://treasury.alabama.gov/collegecounts/ (accessed November 3, 2018).

-

Fifty-fourth Arizona Legislature, First Regular Session, S.B. 1349, https://apps.azleg.gov/BillStatus/BillOverview/71984.

-

Ark. Code § 6-84-103(14) (2018).

-

Cal. Com. Code § 69980, http://leginfo.legislature.ca.gov/faces/codes_displayText.xhtml?lawCode=EDC&division=5.&title=3.&part=42.&chapter=2.&article=19 (accessed November 3, 2018).

-

Colo. Rev. Stat. § 23-3.1-302, https://codes.findlaw.com/co/title-23-postsecondary-education/co-rev-st-sect-23-3-1-302.html (accessed November 3, 2018).

-

Rute Pinho, “Federal Changes to 529 Plans,” Connecticut Legislature Office of Legislative Research, January 23, 2018, https://www.cga.ct.gov/2018/rpt/pdf/2018-R-0036.pdf (accessed November 3, 2018).

-

Del. Code Ann. tit. § 3485, http://delcode.delaware.gov/title14/c034/sc12/index.shtml (accessed November 3, 2018).

-

Fla. Stat. § 1009.981, http://www.leg.state.fl.us/statutes/index.cfm?mode=View%20Statutes&SubMenu=1&App_mode=Display_Statute&Search_String=florida+529+savings+plan&URL=1000-1099/1009/Sections/1009.981.html (accessed November 3, 2018).

-

News Release, Path2College, “Important News: Federal Tax Cuts and Jobs Act of 2017 Includes Changes to Section 529 College Savings Plans,” April 3, 2018, https://www.path2college529.com/buzz/?id=1049 (accessed November 3, 2018).

-

Haw. Rev. Stat. Ann. § 256:1–7, http://files.hawaii.gov/tax/legal/hrs/hrs_256.pdf (accessed November 3, 2018).

-

Idaho Code Ann. 33-5401(11), https://legislature.idaho.gov/statutesrules/idstat/Title33/T33CH54/SECT33-5401/ (accessed November 28, 2018).

-

Ill. Comp. Stat. § 505, http://www.ilga.gov/legislation/ilcs/ilcs3.asp?ActID=210&ChapterID=4 (accessed November 3, 2018).

-

Ind. Code Ann. § 6-3-3-12(h), http://iga.in.gov/legislative/laws/2018/ic/titles/006#6-3-3 (accessed November 20, 2018).

-

12D.1(2)(k), https://www.legis.iowa.gov/docs/publications/LGR/87/SF2417.pdf (accessed November 3, 2018).

-

K.S.A. § 75-643 and 646; Kansas Department of Revenue, “Estimated Impact of the Federal Tax Cuts and Jobs Act,” February 14, 2018.

-

Ky. Rev. Stat. Ann. § 164A.305(13)(b), http://www.lrc.ky.gov/Statutes/statute.aspx?id=47977 (accessed November 28, 2018).

-

David Lawhorn, Kentucky Education Savings Plan Trust Manager, letter to Randy Brady, TIAA Tuition Financing, Inc., July 10, 2018, http://thf-legal.s3.amazonaws.com/Amy%202018/2018%20K-12%20TIAA%20authorization%20letter.pdf (accessed November 28, 2018).

-

Louisiana Legislature, 2018 Session, HB 650, https://legiscan.com/LA/text/HB650/2018 (accessed November 3, 2018).

-

20-A M.R.S. § 11471(7) (2018).

-

Md. Code Ann. Education §18-1901(n).

-

Mass. Gen. Laws Chapter 62, § 3(B)(a)(19) (2018), https://malegislature.gov/Laws/GeneralLaws/PartI/TitleIX/Chapter62/Section3 (accessed November 14, 2018).

-

Massachusetts Educational Financing Authority, U.Fund College investing Plan, https://www.mefa.org/products/u-fund-college-investing-plan/ (accessed November 28, 2018).

-

MCL 390.1472, http://www.legislature.mi.gov/(S(bd25lei0ex05akd4ha54nn4t))/mileg.aspx?page=getobject&objectname=mcl-390-1472&query=on&highlight=section%20AND%20529 (accessed November 3, 2018).

-

Minn. Stat. Ann. § 136G.03, https://www.revisor.mn.gov/statutes/cite/136G.03 (accessed November 3, 2018).

-

Miss. Code Ann. § 37-155-105, https://codes.findlaw.com/ms/title-37-education/ms-code-sect-37-155-105.html (accessed November 28, 2018).

-

State Treasury of Mississippi, “Can MACS Be Used to Pay for Elementary and Secondary Tuition Expenses?” https://www.treasurerlynnfitch.ms.gov/collegesavingsmississippi/Pages/MACS-FAQs.aspx#01 (accessed November 28, 2018).

-

Missouri’s 529 College Savings Plan (MOST), “MOST Tax Benefits,” https://www.missourimost.org/home/why-choose-most/most-529-tax-benefits.html (accessed November 3, 2018).

-

Mont. Code Ann. § 15-52-103.

-

Neb. Rev. Stat. § 85-1802, https://nebraskalegislature.gov/laws/statutes.php?statute=85-1802 (accessed November 3, 2018).

-

Nebraska State Treasurer’s Office, “College Savings Plan: State Legislation Needed for NEST Plans to Be Used for K–12,” https://treasurer.nebraska.gov/csp/ (accessed November 3, 2018).

-

N.J.S.A. 18A:71B-36, https://law.justia.com/codes/new-jersey/2016/title-18a/section-18a-71b-36/ (accessed November 3, 2018); New Jersey Department of the Treasury, Division of Taxation, “Notice: New Jersey’s Gross Income Tax Treatment of IRC Section 529 Savings Plans and Private, Religious, Elementary, and Secondary Schools,” August 2, 2018 (accessed December 6, 2018).

-

N.M. Stat. § 7-2-2.

-

Alicia Romero, Tax Information and Policy Office, State of New Mexico Taxation and Revenue Department, letter to John Monforte, April 23, 2018, https://static1.squarespace.com/static/5702d49b2fe1312243f9bddc/t/5b325ba50e2e722aa6288e4a/1530026955716/NewMexicoTaxationRevenueDepartmentAdvisoryComment.pdf (accessed November 3, 2018). See also The Education Trust Board of New Mexico, “The Education Plan: Recent Federal Tax Law Changes,” https://www.theeducationplan.com/recent-federal-tax-law-changes (accessed November 3, 2018).

-

Office of the New York State Comptroller, “NY’s 529: Federal Tax Reform Update,” https://www.osc.state.ny.us/college/529.htm (accessed November 3, 2018).

-

N.G. Gen. Stat. § 116-209.25(b); North Carolina General Assembly, 2017-18 Session, S.B. 99, p. 232.

-

Bank of North Dakota’s 529 Plan, “Tax-Deferred Growth,” https://www.collegesave4u.com/home/features-and-benefits/tax-benefits.html (accessed November 3, 2018).

-

132nd Ohio General Assembly, S.B. 322, https://legiscan.com/OH/text/SB22/id/1774556/Ohio-2017-SB22-Enrolled.pdf (accessed November 3, 2018).

-

Okla. Stat. tit. § 70-3970.3, http://webserver1.lsb.state.ok.us/os/os_70-3970.3.rtf (accessed November 1, 2018).

-

Press Release, Oklahoma 529 College Savings Plan, “Important News: Federal Tax Cuts and Jobs Act Includes Changes to Section 529 College Savings Plans,” April 3, 2018, https://www.ok4saving.org/buzz/?id=1047 (accessed November 3, 2018).

-

Bill 4080, 79th Oregon Legislative Assembly, 2018 Regular Session, House.

-

Pennsylvania General Assembly, 1992, Act 11.

-

PA529, “FAQs,” https://www.pa529.com/faqs/ (accessed November 1, 2018).

-

R.I. Gen. Laws § 61-57-3, http://webserver.rilin.state.ri.us/Statutes/TITLE16/16-57/16-57-3.HTM (accessed November 1, 2018).

-

South Carolina Future Scholar 529 College Savings Plan, “Common Questions,” https://futurescholar.com/resources/common-questions/#withdrawing-funds (accessed November 1, 2018).

-

SDCL 13-63-1, http://sdlegislature.gov/Statutes/Codified_Laws/DisplayStatute.aspx?Type=Statute&Statute=13-63-1 (accessed November 1, 2018).

-

Utah Code Annotated § 53B-8a-102.5(7), https://le.utah.gov/xcode/Title53B/Chapter8A/53B-8a-S102.5.html?v=C53B-8a-S102.5_2017032520170325 (accessed November 29, 2018).

-

my529, “Check State Laws Before K-12 Tuition Withdrawals,” https://my529.org/newsletter-april-2018/check-state-laws-before-k-12-tuition-withdrawals/ (accessed November 28, 2018).

-

Vt. Stat. Ann. tit. 16 V.S.A. § 2876, https://legislature.vermont.gov/statutes/section/16/087/02876 (accessed November 1, 2018).

-

Vermont Higher Education Investment Plan, “How To’s,” https://www.vheip.org/how-tos/#make-a-withdrawal (accessed November 1, 2018).

-

Va. Code Ann. § 23.1-700, https://law.lis.virginia.gov/vacode/title23.1/chapter7/section23.1-700/ (accessed November 3, 2018).

-

Virginia 529, “Qualified Higher Education Expense,” https://www.virginia529.com/resources/key-terms/#qualified-higher-education-expense-qhee (accessed November 1, 2018).

-

D.C. Code Ann. § 47-4501(9) https://code.dccouncil.us/dc/council/code/sections/47-4501.html (accessed November 28, 2018).

-

DC College Savings Plan, “Important DC Tax Deduction Update,” https://www.dccollegesavings.com/home/k-12-tuition-update.html (accessed November 28, 2018).

-

W. Va. Code § 18-30-3.

-

News release, Edvest (Wisconsin’s College Savings Plan), “Important News: Federal Tax Cuts and Jobs Act of 2017 Includes Changes to Section 529 College Savings Plans,” May 8, 2018, https://www.edvest.com/buzz/?id=979 (accessed November 1, 2018).