The proposed House and Senate tax reform bills that lawmakers are currently merging into one would mean tax cuts for most Americans. Nevertheless, change—even good change—can bring about uncertainty.

Retirees may be the most concerned about what tax reform will mean for them, as most rely on relatively fixed incomes.

But in fact, the proposed reforms are mostly good news for retirees. For the most part, they would be less affected than other Americans, as the proposed reforms would not change the way Social Security and investment income are taxed.

Many retirees would in fact benefit from the tax bills’ doubling the size of the standard deduction.

While seniors’ earnings and pension income would be subject to new individual income tax brackets and rates, those changes would actually mean tax cuts—not increases—for an overwhelming majority of seniors and retirees.

There are three provisions in the tax reform bills that could particularly affect retirees:

1. Medical Expenses Deduction

Currently, anyone who has high medical expenses can deduct the portion of those expenses that exceeds 10 percent of their income. So a couple who earns $40,000 in income and has $10,000 in medical expenses can deduct $6,000 of those expenses.

The House bill eliminates this deduction, but the Senate bill maintains it and increases the deductible amount to over 7.5 percent of income for 2017 and 2018. In the above example, this would mean a $7,000 deduction.

2. Personal and Elderly Deductions

Currently, in addition to claiming a $4,050 personal exemption, people over 65 can also claim a $1,250 blind or elderly deduction. Both bills eliminate the personal exemption and replace it with a roughly doubled standard deduction.

The House proposal eliminates the elderly deduction, while the Senate bill maintains it.

3. Other Itemized Deductions

Two of the deductions that have received the most attention are changes to state and local taxes and mortgage interest. Both the House and Senate bills eliminate the state and local tax deduction and cap the property tax deduction at $10,000.

For mortgage interest, the Senate bill maintains current policy while the House bill caps the mortgage interest deduction at $500,000, but only for new home purchases. These deductions tend to have less impact on retirees who often have no mortgage or are far enough along in their mortgage payments that they have little mortgage interest.

Retirees typically also have lower state and local income taxes because not all of their income is subject to taxation.

To illustrate just how the House and Senate tax reform packages would affect different retirees, consider these five examples.

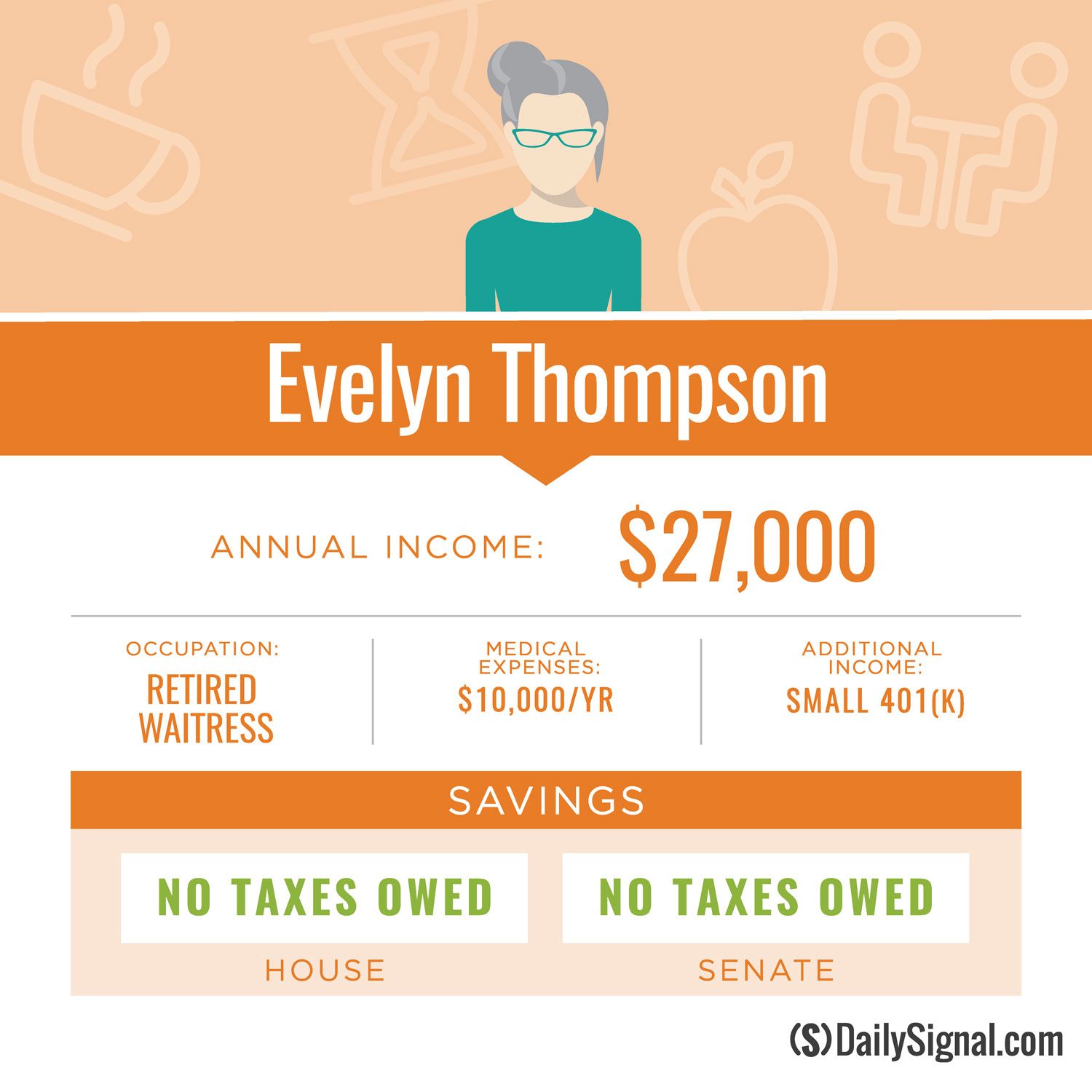

Evelyn Thompson

Evelyn is a retired waitress and a widow. She receives an average-level Social Security benefit of $16,000 per year, as well as $11,000 from her husband’s 401(k). She has $10,000 in medical expenses.

Evelyn’s tax bill will not change under the proposed reforms. She does not pay anything under the current tax system, and she wouldn’t pay anything under the reform proposals because they do not change the taxation of Social Security benefits or investment income.

Moreover, the proposed increases in the standard deduction, coupled with lower tax rates, make up for her loss of the medical expense deduction in the House proposal.

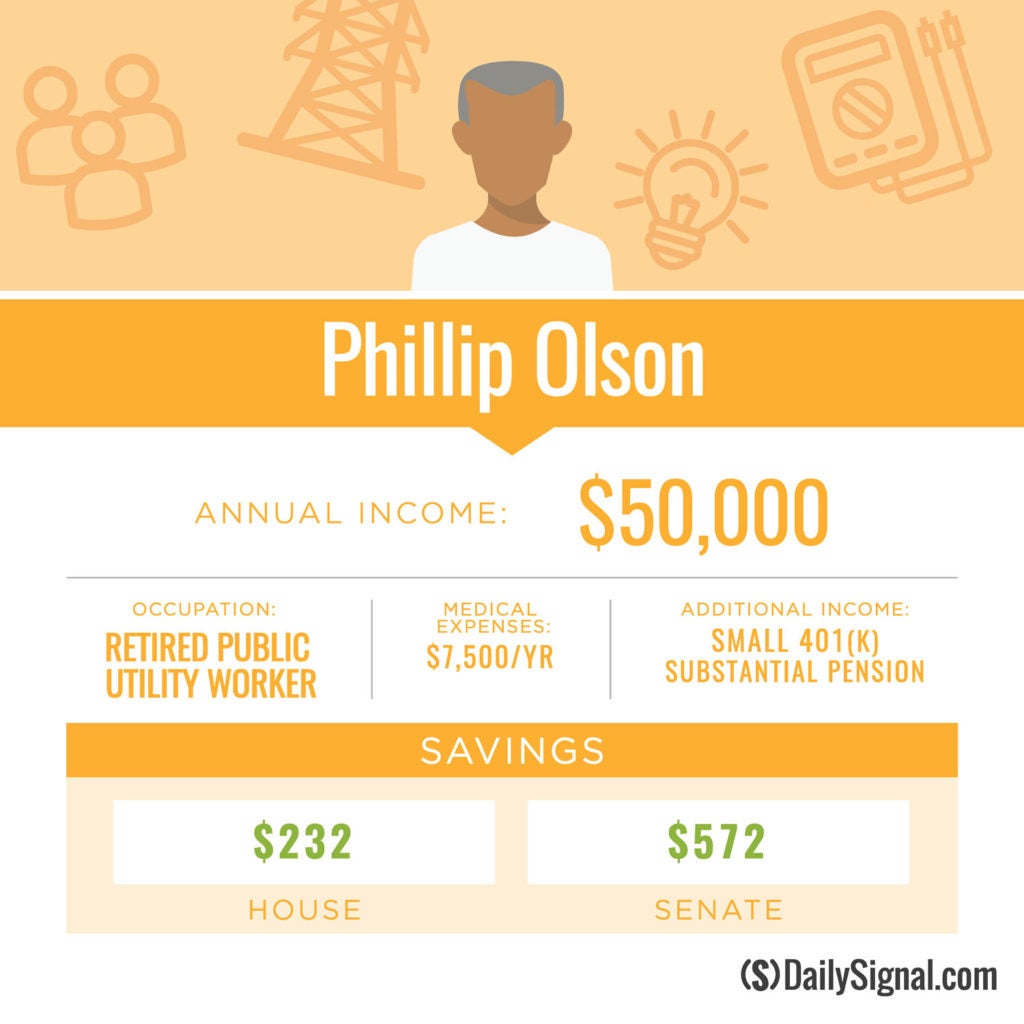

Phillip Olson

Phillip is a retired utility worker. He earned an average income throughout his career, but now receives a significant pension and even saved a little on his own through a 401(k).

His combined retirement income is $50,000 a year, consisting of $16,000 in Social Security benefits, a $28,000 pension, and $4,000 in 401(k) income. Phil has $7,500 in medical expenses, and he currently pays $3,988 in federal taxes.

Phil’s tax bill would go down by $232 under the House’s proposal (to $3,756) and by $572 under the Senate proposal (to $3,416). This would mean a 5.8 percent tax cut under the House proposal and a 14.4 percent tax cut under the Senate proposal.

These tax cuts would come from lower marginal tax rates on his $28,000 in pension income. In addition, no changes would be made to the taxation of Phil’s $18,000 in Social Security benefits, or his $4,000 in 401(k) income.

Although Phil has $7,500 in medical expenses, the higher standard deductions under the House and Senate bills make it not worthwhile for him to deduct these expenses, meaning he would face less paperwork and a simpler tax-filing process. Phil would also benefit from lower tax rates on his income.

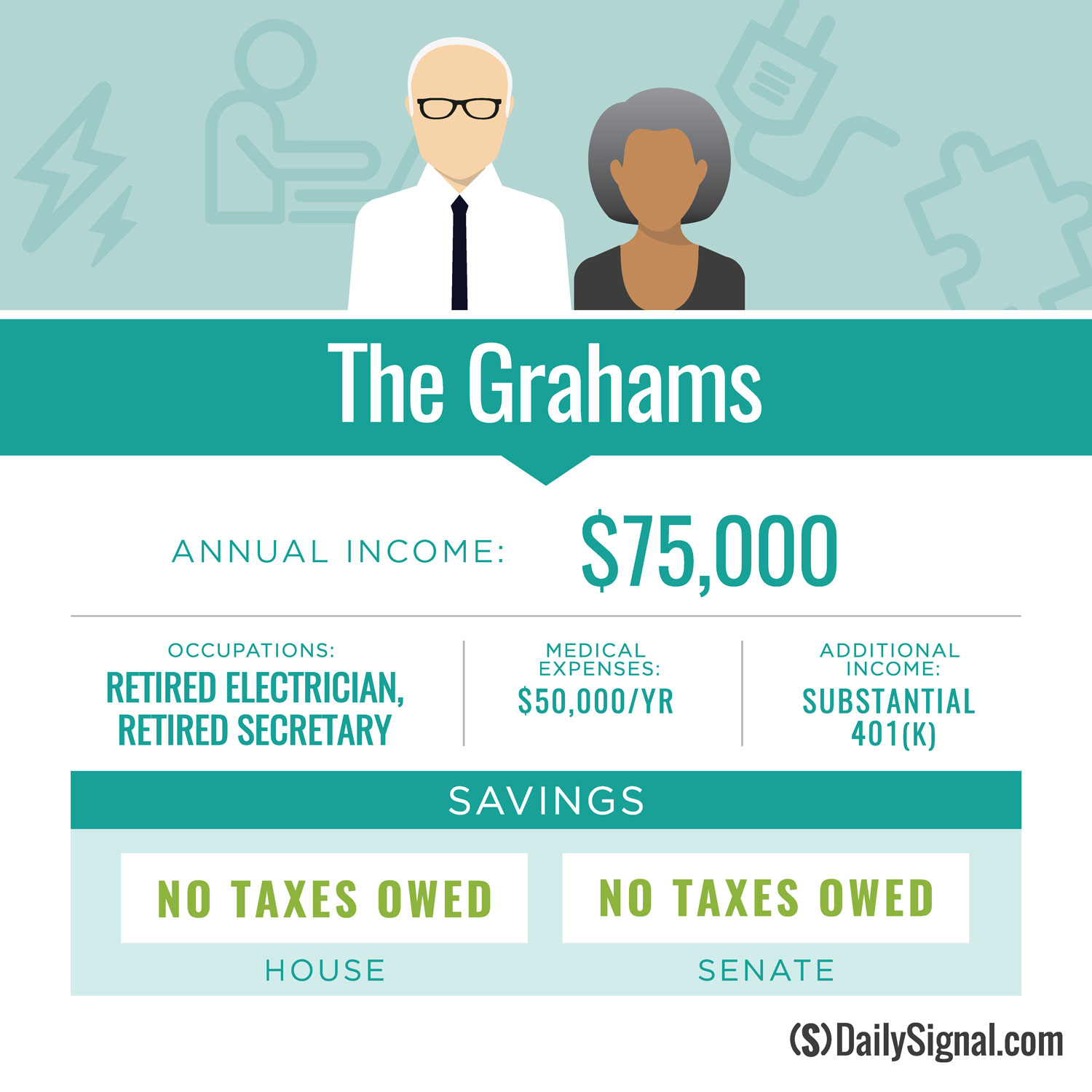

Craig and Grace Graham

The Grahams are a middle-income retired couple with very high medical expenses. Craig was an electrician and Grace was a secretary.

Together, they receive $25,000 a month from Social Security and $50,000 from their 401(k) savings, making for a total income of $75,000. However, Craig’s health has deteriorated significantly and he had to enter a nursing home this year, which resulted in $50,000 in out-of-pocket medical costs.

Because all of their income comes from Social Security and investments—which the proposed reforms do not change—the Grahams’ tax bill would not change under either the House or Senate proposals. In each case, they would owe nothing in federal income taxes.

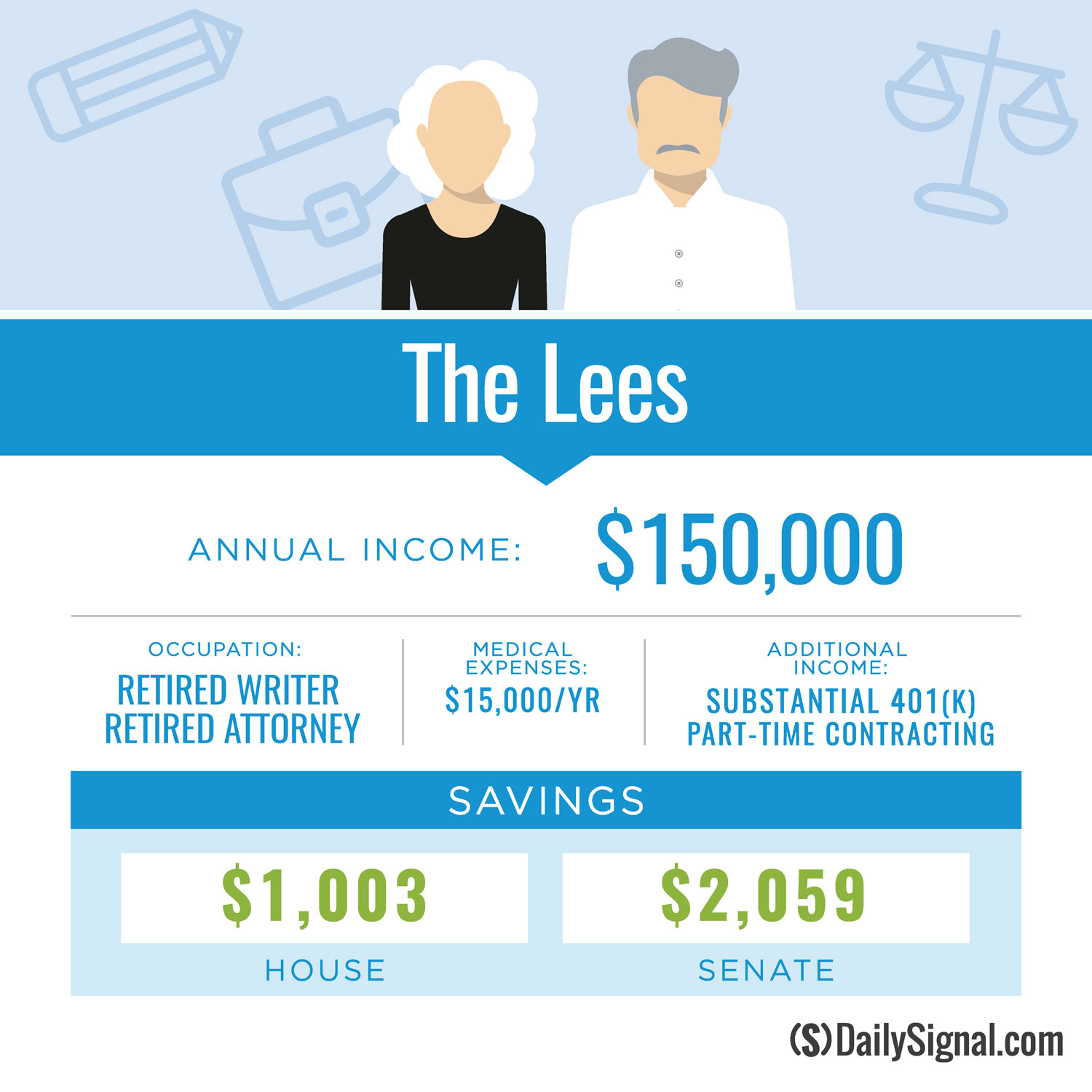

Michael and Sarah Lee

The Lees are a semi-retired, upper-income couple. Michael was a writer and Sarah was an attorney, but both still do some contract work on the side.

The Lees have a combined income of $150,000 a year, consisting of $50,000 in earnings, $50,000 in Social Security benefits, and $50,000 in investment income from their 401(k)s. They have $15,000 in out-of-pocket medical expenses, and currently pay $15,613 in federal income taxes.

Under the House proposal, they would pay $1,003 less (their federal income tax bill would be $14,610), and under the Senate proposal they would pay $2,059 less (their federal income tax bill would be $13,554). This would mean a 6.4 percent tax cut under the House proposal and a 13.2 percent tax cut under the Senate proposal.

Although the Lees’ taxable income would go relatively unchanged under both proposals, they would receive significant tax cuts under both the House and Senate bills due to lower tax rates on their earned income.

Hector and Carmen Garcia

The Garcias’ are a wealthy retired couple. At one time, they jointly operated their own real estate development company, which they have since passed on to their children.

The Garcias have accumulated significant savings, and they receive $950,000 in investment income each year along with $50,000 in Social Security benefits. The Garcias make generous charitable donations of $100,000 a year, they have $25,000 in medical expenses, and they pay about $79,000 in state and local taxes.

Although the Garcias do not need all of their income to cover their own expenses, they enjoy using their wealth to help their children with their business ventures, to support some family members who live outside the U.S., and to contribute to each of their 10 grandchildren’s college accounts.

Under the current tax system, the Garcias pay $151,768 in federal income taxes. Under the proposed House bill, their taxes would increase by $12,744 (to $164,512) and under the Senate bill, their taxes would rise by $12,149 (to $163,917).

This would mean an 8.4 percent tax increase under the House proposal and an 8 percent tax increase under the Senate proposal. These increases would come from a loss of their state and local income tax deduction and the $10,000 cap on the property tax deduction.

While the Garcias would lose these deductions, they would keep other deductions—such as for charitable donations—that are worth more under the proposed reform packages because both House and Senate bills would eliminate the phaseout of itemized deductions, which exists in the current tax code.

Good Changes for Most Retirees

Understandably, many retirees may be concerned about how tax reform will affect them. But the bare facts of these two tax reform bills should be reassuring: Tax reform, for the vast majority of American seniors, is great news.

Moreover, although not represented in seniors’ individual income tax bills, the corporate and small business tax provisions contained in the proposed reforms would benefit seniors both through their investment incomes and their purchases.

That’s because the benefits of lower corporate taxes flow to individuals who own stock in those corporations, workers who are employed by those corporations, and consumers who purchase goods and services from those corporations.

As the House and Senate move toward reconciling their two similar tax bills, American seniors can rest assured that this bill is a win for them.

This piece originally appeared in The Daily Signal