The House passed its version of the Tax Cuts and Jobs Act on Thursday, a bill that would reform the tax code by lowering marginal rates for most households, corporations, and small businesses.

The Senate is also working on its own version of the bill. Though the complete details are yet to be finalized, both the House and Senate versions contain enough in common that we can estimate the effect these bills would have on the economy once a new equilibrium is reached. Most of these effects would likely occur within the 10-year budget window.

The following estimates reflect the House bill as reported out of the Ways and Means Committee and the chairman’s mark being debated in the Senate Finance Committee. (The version that the House passed is nearly identical to the bill reported out of committee).

Main Reforms in the Bill

Both versions of the Tax Cuts and Jobs Act reduce the corporate tax rate from 35 percent to 20 percent, reduce tax rates on non-corporate (pass-through) businesses, and increase the present discounted value of capital cost recovery allowances.

The capital cost recovery allowance improvements are primarily a function of a reduced class life for structures in the Senate bill, and higher section 179 expensing thresholds, as well as temporary expensing for machinery and equipment in both the House and Senate bills.

The Senate bill generally lowers the rates on pass-through entities to a greater degree than the House bill.

Long-Run Estimates

The economy and our tax code are complex systems. A complete analysis of any tax reform proposal should reflect that complexity. However, a simple estimate that focuses on the key marginal rate changes is sufficient to give an idea of the magnitude of the economic effects without resorting to complicated models.

The estimates presented here are within a reasonable range of values, based on empirical studies as described below in the methodology section.

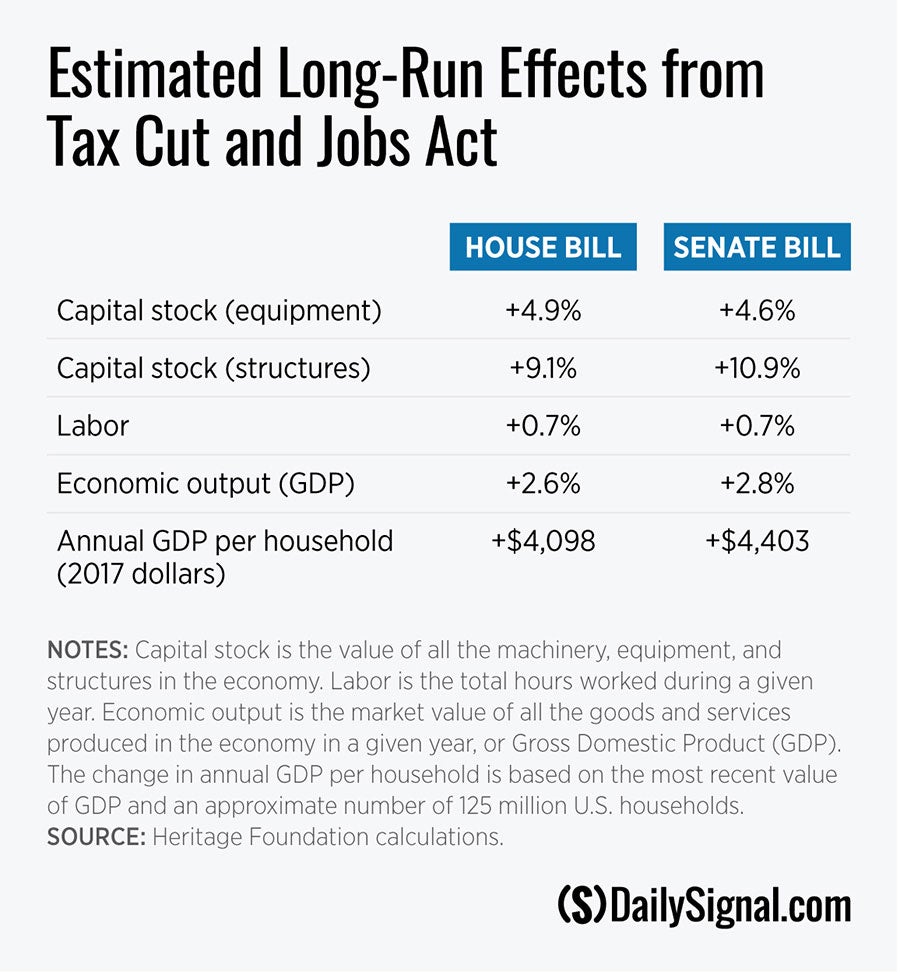

We estimate that the House bill would increase the capital stock related to equipment by 4.9 percent, and the capital stock related to structures by 9.1 percent. These estimates are very similar to the comparable projections for the Senate bill (4.6 percent and 10.9 percent for equipment and structures, respectively).

The House bill is projected to boost long-run gross domestic product (GDP) by 2.6 percent, and the Senate version is expected to increase long-run GDP by 2.8 percent. To put that number in perspective, the increase in GDP translates into an increase of $4,000 to $4,400 per household. These results are comparable to other recently published estimates, such as those released by the Tax Foundation and the Council of Economic Advisers.

Both bills only temporarily change the rules for expensing of new investment. We calculated the effects of the bills when the expensing rules are in place and the effects after the expensing changes have expired. Our reported estimates are the simple average of the two, which reflects business’ expectations that the changes in expensing rules may or may not be made permanent at a later date.

If the expensing rules were made permanent, we estimate that GDP would be 3.0 percent higher than baseline under both bills. If the expensing rules were to expire, we estimate the House bill would increase GDP by 2.3 percent and the Senate bill would increase GDP by 2.6 percent.

Methodology

Our estimate is based on a standard neoclassical production function, which shows how the amount of capital and labor used in production determine economic output. When more capital or labor is used in production, output increases.

Our estimates reflect the steady-state values of capital and labor. In the steady state, the capital stock and hours worked per person have reached their equilibrium values because the marginal costs from additional investment and work just equal the marginal benefits, after taxes. However, economic growth continues due to increases in population and technological innovation.

The presence of taxes on businesses and households creates differences between the returns generated by investment and the returns paid to savers, as well as differences between the wages paid by employers and the wages received by workers.

These differences create lost opportunities. Firms don’t invest and households don’t work on projects where the marginal benefit is lower than the amount of the tax. Economists often call this loss dead-weight loss or excess burden.

Our analysis shows the effects of the Tax Cuts and Jobs Act through two channels. The first channel focuses on the demand for financing capital. A firm considering an investment in capital has to weigh the marginal cost of the capital investment against its marginal benefit, which is its projected return. The cost of capital to a firm is a function of the return it pays to equity and debt holders, the rate of depreciation of capital, and the taxes due on that capital. The equation for calculating the cost, originally set forth by Robert Hall and Dale Jorgenson, is referred to as the user cost of capital. Higher corporate tax rates increase the user cost of capital. Additionally, increases in the present discounted value of capital cost recovery allowances decrease the user cost of capital.

The second channel focuses on the supply of labor. When households decide how much to work, they have to weigh the marginal benefit of their after-tax wages against the marginal cost of activities other than work. An increase in after-tax wages increases the benefit to households from forgoing other activities, resulting in additional hours worked.

The lower the corporate tax rate, the greater the number of investment projects that are economically worthwhile, and higher the steady-state level of capital. Similarly, the lower the income tax rate, the greater the number of job opportunities that are economically worthwhile, and the higher the steady-state level of hours worked.

Economic growth would increase temporarily following the passage of the Tax Cuts and Jobs Act as the economy would move to a new steady state with a higher per-capita GDP. The benefits of these reforms would accrue every year as the economy would operate in a steady state with higher GDP into the indefinite future.

Details About How the Estimate Was Conducted

We take the nominal rate of the return to capital to be 9 percent, which is the approximate average annual nominal return on the S&P 500 from 1871 to 2017. Recent yields on Baa corporate bonds have averaged around 5 percent. We take the inflation rate to be 2 percent, which is the value that the Federal Open Market Committee judges to constitute stable prices. Assuming that companies rely on debt for 25 percent of their financing, these values imply a required real rate of return of 6 percent. We assume that interest rates remain the same following the change in taxes.

The marginal tax rates for pass-through entities change with income and type of pass-through entity. We simplify the range of rates and take the current law to have a marginal rate of 28 percent, the House bill to lower the marginal rate to 25 percent, and the Senate bill to lower the marginal rate to 21 percent.

For depreciation rates, we use 0.13 for equipment and 0.03 for structures, which correspond to the average depreciation relative to the current-cost stock of each asset type as reported by the Bureau of Economic Analysisin the period 2006-2016.

The user-cost elasticity of capital describes the percentage change in the capital stock given a one percent increase in the user cost of capital. It also corresponds to the elasticity of substitution between capital and labor in production. The larger this value, the easier it is for firms to change the mix of capital and labor used in production. The standard neoclassical Cobb-Douglas production function implies a value for this elasticity of -1. A recent report from the Council of Economic Advisersnotes a consensus in the literature around this value.

The cut in the corporate tax rate only applies to corporations, which hold about 75 percent of private, non-residential fixed assets, according to data from the Bureau of Economic Analysis. The changes in expensing will apply to all firms. Our estimates of the change in capital stock reflect the distribution of capital holdings by legal form of organization.

The output elasticity of capital describes the percentage change in output that follows a one percent increase in capital. We use values of 0.15 for equipment and 0.13 for structures, which are both taken from a paper by Akos Valentinyi and Berthold Herrendorf.

Though both bills maintain the graduated income tax brackets, for simplicity we reduce the several marginal income tax brackets to a single marginal rate. We take a weighted average of the marginal rates according to the proportion of filers in each bracket as reported by the U.S. Census. The weighted changes are dominated by the $15,000-$75,000 bracket, which contains approximately half of households. We take both bills to increase after-tax wages by 4 percent.

We use a labor supply elasticity of 0.3. In a survey, Michael Keanesuggests that this is a typical estimate for the labor supply elasticity of individuals. It is also the value used by the Tax Foundation in their Taxes and Growth model.

We use a value of 0.6 for the output elasticity of labor. That value approximately corresponds to the share of labor’s compensation in output.

Additional Considerations

The estimates we report are for our preferred values. Changing the parameters of the model or incorporating additional features will produce slightly different estimates, though they should be within the range of what we report here.

There is some disagreement in the literature about the appropriate value for the user-cost elasticity of capital. However, a relatively recent survey by Robert Chirinko reports a number of estimates in that range, but places more weight on estimates in the range of -0.4 to -0.6. Using these alternative values suggests that the change in GDP due to changes in the cost of capital would be half as large as reported in the table above. We also note that the lower the elasticity of substitution between capital and labor, the higher the increase in labor productivity and wages from additional investment.

Additionally, there is a range of estimates for labor supply elasticity. This range is in part due to differences between labor supply at the individual household level and at the aggregate, economy-wide level. Individuals tend to work around 40-hour work weeks, and may change hours only a little in response to lower taxes. However, lower income taxes are more substantial factors for people deciding whether or not to enter the workforce. Thus, while the micro estimates may place the elasticity of labor supply around 0.3, Edward Prescott and Johanna Wallenius suggest that the aggregate labor supply elasticity is around 3. That elasticity would imply that the effects of the Tax Cuts and Jobs Act on labor supply are 10 times larger than what we have reported in our estimates. However, we choose to use the conservative elasticity value in our estimates.

All of our estimates assume that wages and interest rates remain constant. The changes in the tax code constitute shifts in the demand for capital financing and the supply of labor. Wages and interest rates will only stay constant if the supply of savings and the demand for labor are perfectly elastic. The former is more plausible once the international mobility of capital is considered. The lower the elasticity of these curves, the larger the increase in returns and decrease in pre-tax wages, and the smaller the increases in capital and labor.

This calculation is not meant to substitute for the full analysis of a more detailed model. However, the simplicity of the calculation clarifies the mechanisms at work.

The Tax Cuts and Jobs Act would lower the cost of capital and increase after-tax wages, which would increase the capital stock and number of hours worked, both of which would cause an increase in GDP.

This piece originally appeared in The Daily Signal