There is growing talk of Congress pursuing tax reform through the creation of an “innovation box” instead of focusing on broad business tax reform. This would be a mistake.

An innovation box, often called a patent box in Europe, offers lower tax on certain types of income derived from intellectual property, or IP.

Earlier this year, it seemed possible Congress and President Obama would work together on reforming the business side of the tax code, leaving the individual side for the future. Such an approach made sense, as the business tax system is the biggest current inhibitor of growth in the code.[1] However, more than halfway through the year, there has been no progress on such a deal—and there will likely be none before the year ends.[2]

In lieu of such reform, Congress is pursuing a scaled back approach to business reform. Currently, there is talk on Capitol Hill of reforming the international portion of the business tax code and tying it to a bill that replenishes the Highway Trust Fund (HTF).[3] As part of that package, some in Congress are discussing taxing certain types of income derived from IP at a lower rate by creating an innovation box.

The idea for an innovation box in the U.S. has taken form only in the past few months. Lost in the rush is a discussion of whether a box is sound policy. Indeed, innovation boxes are not sound policy and are difficult to construct properly. Congress should not rush to implement one. Rather, it should focus on lowering business tax rates and establishing a territorial system for multinational businesses.

Lowers Taxes on Income from Qualifying IP

An innovation box offers lower tax on certain types of income derived from IP. Income from things such as patents, trademarks, copyrights, know-how, brands, business processes and formulas, designs, logos, customer lists, and other types of IP are eligible for inclusion in the box in some combination in the countries that have them. If a business has income that fits the definition of the box, it can put that income in the box and pay lower taxes, either through a lower rate on the income or by claiming a large exemption of the income from tax thus exposing a small remaining portion of the income to the country’s business tax rate.

IP is generally highly mobile, which means that businesses can sell it to subsidiaries in low-tax jurisdictions without moving plant, equipment, and employees. Contrary to common perception, businesses must have a business or economic reason for selling the IP to a subsidiary in another country, such as the subsidiary is utilizing the IP there. Businesses cannot move IP solely for tax benefits without conflicting with transfer pricing laws.

If businesses are able to price the IP low enough and still adhere to applicable transfer pricing laws, they will reap tax savings as long as the IP generates income. There is inherent risk in such a transaction, however. IP is volatile and, in a short period of time, can shift from being profitable to being valueless. If IP does lose its value, the business in question could end up worse off due to the transaction. Nevertheless, the potential tax savings creates an incentive for businesses to sell their IP to subsidiaries in low-tax countries.

The motivation for countries that have higher tax rates to create innovation boxes is to encourage businesses not to move their IP to those low-tax locations. Retaining this IP helps maintain the country’s tax base, which in turn allows it to raise more tax revenue. A secondary justification is that it encourages job creation by businesses in innovative industries that create the IP that usually qualifies for inclusion in the box[4]—a highly arguable proposition.

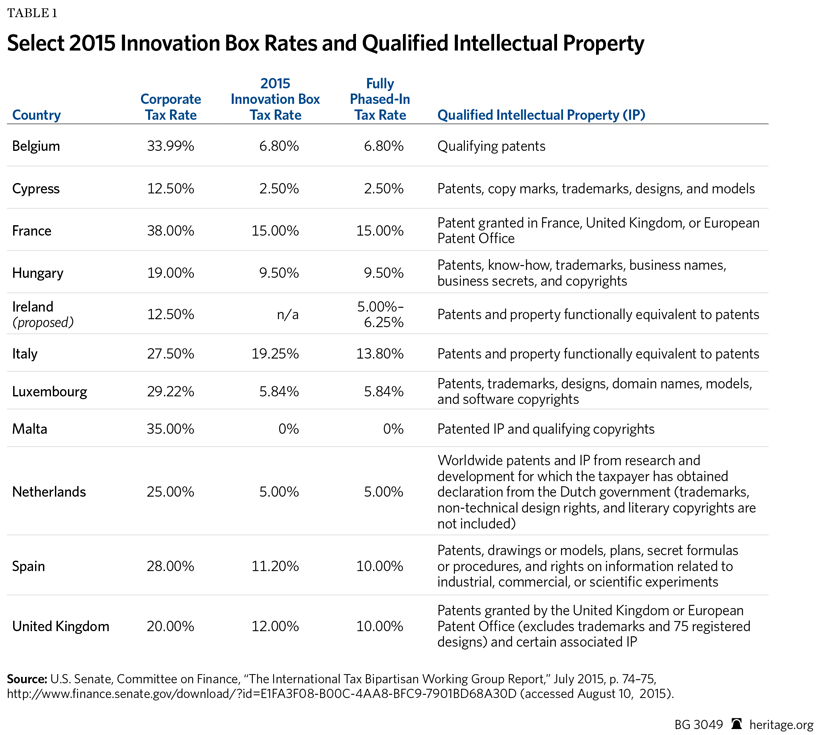

Many countries in Europe have innovation boxes that they have established in recent years. The United Kingdom (U.K.) was the latest to create one. Other countries that have them include Belgium, France, Hungary, Italy, Luxembourg, The Netherlands, and Spain.

Each of these boxes is unique to the country that offers it. The countries offer different rates on qualifying income, define the qualifying income differently, and have different rules for administering the boxes.[5]

Multiple Justifications for an Innovation Box in the U.S.

The push for the U.S. to create an innovation box intensified when the Senate Finance Committee’s Working Group on International Tax Reform released its report in early July. The group, co-chaired by Senators Rob Portman (R–OH) and Charles Schumer (D–NY), recommended that Congress create an innovation box, although they did not include any details of how the box should be constructed.

The group’s stated reason for wanting an innovation box was as follows:

The co-chairs agree that we must take legislative action soon to combat the efforts of other countries to attract highly mobile U.S. corporate income through the implementation of our own innovation box regime that encourages the development and ownership of IP in the United States, along with associated domestic manufacturing. They continue to work to determine appropriate eligibility criteria for covered IP, a nexus standard that incentivizes U.S. research, manufacturing, and production, as well as a mechanism for the domestication of currently offshore IP.[6]

That statement, despite being vague, conveys the multiple motivations for creating an innovation box:

-

Protect U.S. businesses from OECD BEPS. The ongoing work of the Organization for Economic Co-operation and Development’s (OECD) BEPS (Base Erosion and Profit-Shifting) project, which seeks to make it harder for businesses to sell their IP between their subsidiaries, is one of those motivations. If the U.S. Treasury Department decides to enforce as many of the recommendations of OECD’s BEPS guidelines as it can without congressional approval, U.S. businesses will end up paying higher taxes.

They already pay an uncompetitive amount of tax because the U.S. has the highest business tax rate in the OECD and because it taxes businesses on their foreign income under its worldwide system. Raising taxes on U.S. businesses would make an already untenable situation even worse. Some see an innovation box as a way to preempt harm from the BEPS project because the box could potentially lower taxes for the type of income the project would target.

-

Combat the high business tax rate. The high business tax rate in the U.S. is another potential argument for an innovation box. It is imperative that Congress lower the rate from over 39 percent (including the 35 percent federal rate and the average rate of the states) to, at least, the OECD average of 25 percent—preferably below that mark. The high rate makes the U.S. the least competitive developed nation for businesses—foreign and domestic—to locate new investment. This is harming job creation and wage growth for U.S. workers.

Because tax reform that would lower the rate is unlikely to happen in the next two years, some see an innovation box as a way to lower the rate some businesses pay on at least a portion of their income.

- Backstop anti-base erosion policies.Talk of an innovation box has often been tied to a potential plan to move from the worldwide system to a territorial one, which would also happen in conjunction with filling the gap in the HTF. Under this plan, the U.S. would establish a territorial tax system (or dividend exemption regime) but would retain the highest business tax rate in the world.

This situation would increase the incentive for U.S. businesses to move their IP to foreign locations. Given the high rate in the U.S., such a move is already attractive to American businesses; the worldwide system, however, requires businesses to, at some point, pay U.S. tax on their foreign income. Consequently, the worldwide system slightly reduces the incentive of shifting IP.

Under a territorial system, these businesses would not pay that extra tax, thereby increasing the incentive to move IP offshore. This reality, however, is not an argument against territorial taxation; to the contrary, moving to such a system would be a boon for the U.S. economy.[7] However, strong base erosion and profit-shifting policies are necessary under a territorial system to prevent U.S. businesses from moving abroad income that should remain in the U.S.

If Congress moves to a territorial system, so long as the high rate is preserved, it will increase the stress on those policies. In that context, an innovation box could be viewed as an additional base erosion measure that would backstop the other policies put in place to deter base erosion and profit shifting. The lower rate it offers would lessen the incentive for U.S. businesses to sell more of their IP abroad.

-

Other countries have such policies. Another argument for an innovation box holds that other countries, including some of our major competitors, have them, so the U.S. should as well. Supporters also argue it is a way to encourage job creation in the innovative and technology fields that would likely see the greatest benefits from the box.

Innovation Box Is Not Sound Policy

Lost in the many arguments made in favor of an innovation box is a discussion of whether it is sound tax policy. In fact, for several reasons, it is not:

-

Picks winners and losers. An innovation box picks winners and losers. All business income should be taxed at the same rate. An innovation box would break this vital factor for maintaining tax neutrality. Those businesses that earn income that qualifies for the box will see their profitability and competitiveness increase sharply because their taxes will fall. Businesses that do not earn such income will see no benefits and therefore will suffer in comparison. It is unfair to force those businesses left out of the box to pay an uncompetitive amount of tax while allowing businesses that happen to be in a congressionally favored industry to enjoy the benefits of lower taxes.

It is not only unfair, but such favoritism distorts the economy by shifting resources to industries that benefit from the box. Such distortions make the economy less productive, which reduces output and wages compared to the ideal system that taxes all income alike.

An innovation box would function much like state tax incentives. States grant lower taxes to attract companies that promise to create jobs. When they grant these incentives, they do not lower taxes for businesses already located in the state. This is unfair to the existing businesses, and the incentives most often fail to create jobs in the states.

-

Not a substitute for a lower rate. Because it would apply only to some forms of income chosen by Congress, many businesses would still face the highest-in-the-world U.S. tax rate on all their income. Hence, an innovation box is no substitute for a lower rate.

-

Lower rate and territorial system needed first. An innovation box, at this point, would be severely premature. Certainly, other countries have them, but those countries also have lower business tax rates than the U.S. Most have territorial systems, and most have substantially better tax treatment for capital investment. These are the factors most harming economic growth, job creation, and wage increases in the U.S. Therefore, Congress should focus first on lowering the tax rate, moving to a territorial system, and making 50 percent expensing permanent (as a first step toward full expensing). Implementing a box without lowering the rate and scrapping the worldwide system would only put an ineffectual Band-Aid on a problem that needs major surgery.

-

Creates new hurdle for tax reform. If the U.S. business tax system was in line with international norms, Congress would likely have no need even to consider an innovation box. Consequently, Congress should focus its energies on modernizing the business tax system. If it provides an innovation box first, the businesses that benefit from it could then oppose broad business tax reform, depending on how low the box lowers their taxes. Congress should be reducing hurdles to tax reform—not creating new ones.

-

Base erosion and profit-shifting concerns legitimate but premature. A reformed business tax system that had a lower rate and was territorial would require strong anti-base erosion and profit-shifting policies. There is no consensus about the right way to construct these policies, and the systems vary by country. The ongoing BEPS work at the OECD is partly an attempt to create uniform standards, but there is no way to know if the forthcoming proposals will be more effective than current systems or if they will have negative economic effects that make them undesirable to implement.

Congress needs to create a territorial system and pick adequate base erosion and profit shifting policies. It could start with what former Chairman of the Ways and Means Committee Dave Camp (R–MI) proposed in his 2014 tax reform plan.[8] After a few years, Congress could then evaluate whether those policies are working, need adjustment, or need to be changed completely. Only in the last case should Congress then reconsider an innovation box.

-

Tax reform better response to OECD BEPS. If the Treasury Department implements some of the OECD’s BEPS policies without congressional approval and raises taxes on U.S. businesses in the process, there are still better alternatives to an innovation box. For instance, Congress could reform business taxes by lowering the rate and moving to a territorial system—a solution that would lower taxes for all businesses.

Furthermore, Congress can stop Treasury from implementing policies it disagrees with by using its power of the purse. It may also put a moratorium on the implementation of a regulation. And a future President would have the power to instruct Treasury to stop enforcing those policies. Importantly, none of these avenues for stopping BEPS requires Congress to create an innovation box.

Rushing Poor Policy

Innovation boxes are complicated to construct. As such, the law needs to explicate the types of income that will qualify for the box, and the rules regarding the box’s use need to be well defined. The U.K., the last major country to create a box, took several years to fully establish its system[9]—Congress is looking to do so in just a few months. On such a compressed schedule, it could make mistakes that could lead to harmful unintended consequences.

Without question, the immediate creation of the innovation box would be poor policy. If, however, Congress decided to pursue such an unsound policy, below are just a few of the many questions it needs to answer. There are several additional technical questions it would have to answer in addition to these.

-

What type of income would qualify for the box? This is the most pressing question as pertains to establishing an innovation box. Assuming it limited the box to IP, Congress would need to determine what types of IP it would allow to qualify for inclusion. There is a multitude of types of IP, and those that Congress would want to qualify would tie directly to what it wants to accomplish by creating the box, something it has yet to make clear. Presumably, Congress would intend for the box to incentivize, at least partly, innovation for high-tech fields under the pretext that such innovation would create jobs in the U.S. This would undoubtedly lead to cronyism, as businesses would fight to make sure their IP qualified and their competitors’ did not.

-

How would it define the qualifying IP and allocate income to the IP? By its nature, IP defies a fixed definition. Yet Congress would need to define, in explicit detail, the guidelines that IP would have to meet to qualify for the box. Even if Congress were able to provide such a definition, the IRS would be under constant strain as businesses try to make their IP fit the parameters of the box. An onslaught of litigation would likely follow.

Furthermore, determining how much of a business’s income is generated by qualifying IP would be extremely difficult. Armies of lawyers, accountants, and economists would be employed making these determinations and quarreling with the IRS.

The situation would be analogous to that which plagues transfer pricing, income sourcing, and expense allocation rules that guide inter-company transactions today. Transfer pricing works well when businesses sell tangible items to their subsidiaries for which there is an established market. It becomes significantly more complicated when they sell IP because defining the income associated with particular IP is difficult. There are rarely markets in which an arm’s-length price for the IP can be determined, which means calculating the income IP earns is fraught with uncertainty. It is impossible, even in principle, to determine what the correct price is. Rules for determining how much income IP placed in an innovation box earns would experience the identical complication.

Isolating the income that IP placed inside an innovation box earns would be the most troublesome challenge with which Congress would have to deal.

-

How would it apply a lower rate? Innovation boxes in different countries apply lower taxes to the qualifying income either by lowering the rate at which they tax the income or by allowing businesses to exempt a sizeable portion of the income from tax and applying the business tax rate to the remaining income. Congress would need to decide which system it would use, although both result in the same outcome: lower taxes for the qualifying income.

-

Would expenses still be deductible (tax gross or net income)? An innovation box would substantially lower tax on qualifying income. Depending on how Congress allowed businesses to deduct concurring expenses, it would substantially affect the size of the tax cut. Some countries disallow or reduce the expenses businesses can claim against income that qualifies for the box. Others allow full deductions for those expenses. If a country reduces the expenses businesses can claim, it reduces the size of the tax cut.

Depending on how an innovation box treats the expenses incurred from the income that qualifies, it would likely create an incentive for businesses to allocate expenses to income that does not fit inside the box. This would further reduce their taxes because it would reduce higher-taxed forms of income. Allocating how much of certain expenses are incurred with certain forms of income is as difficult as determining the income that IP earns and would require extensive rules.

-

How would it treat losses associated with the IP in the box? Congress would also have to determine what options are available to businesses that experience losses on IP they previously put in the box. If Congress allows businesses to claim losses on the IP outside the box, it would create an even larger benefit. Furthermore, would Congress allow businesses to carry forward or back losses on IP in an innovation box to offset further taxes paid when their IP was profitable?

-

Does a business have to participate directly in the creation of the IP for it to qualify for the box? Businesses acquire IP in numerous ways. For example:

- They can fund research and development (R&D) that leads to its creation within their business;

- They can fund the R&D efforts of subsidiaries and then own fully or partially the resulting IP;

- They can hire a contract R&D business to create IP for them; or

- They can buy IP from another business that created it.

Congress would need to detail which acquisition methods would allow IP to gain entry to the box. This is a highly important question for Congress to resolve because what it decides will have a significant impact on how the box functions.

Congress would also need to determine if IP funded or acquired outside the U.S. would be eligible for the box. And does the U.S. business have to be actively engaged in the IP’s creation, or if it can only fund it?

-

Would only new IP be eligible? Or would previously developed IP qualify as well? How Congress decides this question will largely be determined by what it wants the box to accomplish. For instance, if it sees the box as a way to encourage more innovation, it would restrict the box to new IP created after its enactment. If it sees the box as a way to reduce the harm of the high corporate tax rate, it would allow old IP into the box, resulting in large windfall gain to owners of existing IP.

-

How does the box interact with the R&D credit? Assuming Congress continues the R&D credit, as it has since the early 1980s, it would have front-end and back-end incentives for businesses to engage in R&D and create IP. These policies could serve different purposes depending on how Congress structures the box. However, Congress would need to consider if the box and the R&D credit both end up accomplishing the same goal, whether both policy instruments are necessary.

Conclusion

It is premature for Congress to consider an innovation box in the U.S. Instead, Congress first needs to reform the business tax system by reducing the tax rate and moving to a territorial system. Such reform is critical, as the current high tax rate and worldwide regime are the biggest inhibitors of economic growth in the tax code today. If Congress made those long-overdue and important improvements, there would likely be no need for an innovation box in the U.S.

—Curtis S. Dubay is Research Fellow in Tax and Economic Policy in the Thomas A. Roe Institute for Economic Policy Studies, of the Institute for Economic Freedom and Opportunity, at The Heritage Foundation.