The United States does not have a private-sector health insurance system, let alone a functioning competitive market for insurance or health services. In fact, the federal government has been the dominant force in American health care for decades, long before the recent massive expansion of the government’s role in the 2010 Patient Protection and Affordable Care Act (PPACA).[1] Through overly restrictive policies, Medicare, Medicaid, and tax subsidies, the federal government has dominated the operation of the U.S. health care system for the past half-century.[2] It is primarily federal policies that are responsible for driving up costs and making health insurance unaffordable for so many Americans.[3]

The argument over the future of U.S. health care is essentially an argument over how to best allocate scarce resources in this large and important sector of the national economy. Proponents of centralized government control of health care are fond of saying that reliance on a private-sector approach in the U.S. has been tried and failed. According to their arguments, most Americans are enrolled in private insurance, costs are high, and the insurance is insecure. They claim that the private marketplace is therefore to blame for many of the problems prevalent in U.S. health care.

The major flaw in such arguments is that the United States is not a competitive market and never really has been. It is therefore incorrect to look at the broad performance of the largely uncompetitive American health care system and make judgments about whether a competitive health system would work well or not.

Assessing the value of competition in health care thus requires taking a more indirect approach to searching for evidence, most especially by looking at more isolated instances when consumers have been presented with cost-conscious choices in health care.[4] The findings from this kind of examination can then be supplemented with reviews of what has happened when other previously overregulated industries were deregulated as well as with careful critiques of the theoretical arguments that suggest that health care is fundamentally ill-suited to a competitive marketplace. From this kind of an assessment, a clear picture emerges—a competitive marketplace would not only work well in health care but would also bring great benefits to the American consumer.

Debunking the Claims Against Markets in Health Care

Many economists believe that health care is inherently different from other industries and cannot operate in a normal marketplace. They argue that governmental regulation, however unsatisfactorily it may be administered, is better than allowing a dysfunctional marketplace to misallocate resources and generate inequities.

These views generally rest on the theoretical arguments offered by distinguished economist Kenneth Arrow some two generations ago.[5] In a famous 1963 essay, Arrow identified a number of characteristics of health care that, he argued, made it unsuitable for normal competition in the marketplace:

- Health care expenses are random and therefore not predictable.

- Health care is plagued by barriers to entry for potential new suppliers of services.

- Health care requires trust in the doctor–patient relationship.

- Providers have more information than patients; therefore, patients are not capable of making well-informed decisions.

- Patients do not see bills until after services have been offered.

Although some of these points are indisputable, collectively they do not necessarily mean that the country is better off with a heavily regulated approach to health care as opposed to one driven more by market forces.

For starters, the question is one of balance. The health system will always be regulated to some degree, such as with licensure requirements for physicians and oversight of insurance. The question is: To what degree will market prices and competition in the health sector be given the necessary space to work, or will Arrow’s arguments lead policymakers to adopt a completely regulated approach to allocating health resources?

Recently, Avik Roy of the Manhattan Institute studied Arrow’s points and made the case that they should not prevent a move toward a market-based system.[6] First, Roy points out that the concept of unpredictable expenses is not unique to health care. From durable goods to services, people purchase extended warranties to protect against unforeseen catastrophic failures. Health insurance serves the same purpose.

Additionally, Roy suggests that in many industries—including the airline, finance, and legal sectors of the economy—there are barriers to entry for new entrants. Barriers to entry, however, are no reason to completely abandon a market system. Of course, market barriers in medicine are particularly onerous and fundamentally distort provider supply. Certificate-of-need laws make it difficult for hospitals to expand, for instance.[7] These barriers, however, should not be accepted as unchangeable facts; on the contrary, policymakers should work toward lowering them.

Evidence from other countries illustrates why lowering these barriers to entry is important. In India, Devi Shetty, a surgeon, has taken advantage of economies of scale to develop large, 1,000-bed hospitals that make health care more affordable. Dr. Shetty’s heart treatment hospital charges $2,000 for open-heart surgery—American hospitals average slightly more than 150 beds and charge between $20,000 and $100,000—while providing high-quality care.[8] Dr. Shetty is currently setting up a chain of similar hospitals in the Cayman Islands to make his services more accessible to patients from the United States as well as the rest of the world.[9]

Roy also points out that the significance of trust is not unique to health care markets. Trust is required in many simple economic transactions, such as purchasing a car or buying a plane ticket, and is important in many other industries, ranging from clothing stores to airlines. In these and other industries, the concept of building trust has become an important aspect of customer relationship management.[10]

Furthermore, informational asymmetry is not nearly as much of a problem today as it may have been in the past. A number of academic studies suggested that, when offered meaningful information, consumers make well-informed decisions. Additionally, as a result of the proliferation of computer technology and websites such as WebMD.com, NJHospitalCompare.com, and PharmacyChecker.com, health care information has become radically more accessible to consumers of all income levels.[11]

Arrow’s final criticism, that delayed billing is inherent in health care, is not true, as a growing number of examples indicate. When consumers are more directly engaged in paying for health services, pre-service price transparency becomes the norm rather than the exception.

Empirical Evidence: Consumer-Directed Health Plans

The U.S. health care system is generally not a competitive marketplace. In particular, current law largely restricts consumers to purchasing insurance within their own states. Additionally, current tax policy offers a tax advantage to employer-based health insurance but not individually purchased insurance, causing most Americans to gravitate toward job-based coverage instead of buying insurance on their own. These distortions, generated by government policy, have largely insulated consumers from their health care choices.[12]

The dearth of true competition in the health care industry does not mean, however, that there is no evidence of what type of health care consumers might choose in a competitive environment. In fact, there have been numerous academic studies that shed light on the subject and point to the very positive impact consumer choice would have on costs and quality.

Several studies strongly suggest that health care shares many common characteristics with competitive industries. In a 1994 study published in the Journal of Health Care Marketing, Goutam Chakraborty, Richard Ettenson, and Gary Gaeth studied patient choice in health insurance and determined nearly 20 factors significantly affected what consumers selected in terms of health insurance. The most notable factors were hospitalization coverage, the choice of physicians, insurance premiums, dental coverage, and options for choosing hospitals.[13]

Since the Chakraborty study, a series of peer-reviewed academic papers have consistently shown consumers to be highly sensitive to health insurance premiums, with a willingness to switch to more cost-efficient plans.[14] Other research has found that providing consumers with information about quality raises this sensitivity.[15] A number of other studies have found that even hospital choice is driven by consumer decision making.[16] The proliferation of information online, accessible by people of all income levels, has made comparing medical providers easier than it has ever been.[17]

One of the most important developments in health policy in recent years has been the rapid growth of consumer-directed health plans (CDHPs). CDHPs constitute a fundamental change in the manner in which health care has traditionally functioned by placing the focus on consumers. Through tax-free health savings accounts (HSAs) and health reimbursement accounts (HRAs), CDHPs allow consumers to treat their health care expenses as they would other expenses. These plans are often associated with high-deductibles for catastrophic care. Many studies have confirmed that CDHPs are effective at decreasing the rate of growth of health spending and create pressure for much greater price transparency.[18]

These results should not be surprising. One of the most well-known studies of consumer behavior in health care, by economist Joseph Newhouse of the RAND Corporation, found that those who had “free” health care consumed more care than they needed.[19] In other words, consumers are price sensitive in health care, just as they are in every other sector of the economy. Since the RAND study, there has been a significant body of academic research suggesting that CDHPs can lower spending and make people more prudent about their health care expenditures, including use of hospital and physician services and the purchase of prescription drugs.[20]

The CDHP concept was tested prominently in the state of Indiana. Then-Governor Mitch Daniels (R) signed the Healthy Indiana Plan into law, offering HSA plans to employees of the state and their families. An evaluation of the plan by Mercer found that the HSAs decreased the state’s health care expenses by roughly 11 percent. The evaluation suggested a distinct change in behavior as consumers had begun to ask important questions about providers and treatments, as well as about the prices of generic medications.[21] These results indicate that the HSAs worked as planned: Consumers became engaged, and the market pressure that resulted produced better results for the state’s taxpayers as well as those enrolled in the plans.

Some critics have asserted that CDHPs will cause people to underuse necessary care.[22] There is plenty of evidence suggesting otherwise, however. In a properly functioning market, CDHPs, and their variants, will compete with more traditional health insurance plans. With easily accessible information, consumers will be able to properly decide which plans are best for them.[23] Some with chronic illnesses may choose to stick with more traditional, comprehensive plans, whereas others may migrate toward CDHPs or their variants.

Other critics contend that CDHPs will attract healthy low-risk enrollees and traditional plans will subsequently consist of more chronically ill patients at a higher cost.[24] This phenomenon is known as “adverse selection.” A recent study published in Health Services Research investigated the presence of adverse selection in the health offerings from the University of Minnesota. In the study, employees had the option to choose a CDHP or a more traditional plan. The study found no evidence that CDHPs had disproportionally enrolled lower-risk individuals.[25]

Moreover, appropriate risk-adjustment mechanisms should minimize the distortions from risk segmentation among competing insurers. In fact, proper risk-adjustment mechanisms can help stimulate the development of innovative and integrated approaches to treating the most chronically ill patients, as recent research has suggested.[26]

The Design of Medicare Part D

One of the best examples of the effects of competition in a government-controlled health care sector lies within Medicare. The Medicare drug benefit, Medicare Part D, was enacted in 2003 and provides a voluntary prescription-drug benefit to seniors.[27] Enactment of the drug benefit added $14 trillion to an already insolvent program.[28] Nevertheless, the authors of the law succeeded in building an element of competition within the defined benefit structure of Medicare.

The design is straightforward. Private insurance plans submit bids indicating the premium they will charge to provide covered drugs. Based on these bids, the government then calculates what its contribution will be by region. The government’s contribution will not vary based on the plan selected by a beneficiary. If a beneficiary selects a relatively expensive plan, she must pay the additional premium herself. Requiring this type of patient-level involvement helps ensure that beneficiaries will be cost-conscious consumers.[29]

Some critics question the ability of seniors to shop carefully for their coverage.[30] Recent research, however, suggests that many seniors have indeed started to shop around for health care more effectively, such as comparing the use of generic drugs with prescription drugs.[31]

The program has also performed better than anticipated, because the competitive aspect of the program exceeded expectations. As of 2012, over 60 percent of Medicare participants are enrolled in Medicare Part D, and about 90 percent have drug coverage of some type (many remain enrolled in retiree plans sponsored by former employers).[32] In addition, approximately 90 percent of senior citizens are satisfied with their Part D coverage, and slightly less than 70 percent claim they are better off under the program.[33] This customer satisfaction is illustrated by the high degree of loyalty to Part D plans observed among seniors participating in the program.[34] Obviously, many of the seniors like a program that is heavily subsidized by taxpayers and thus seniors do not pay the full cost of the program. There is data to suggest that the ability to choose between many different plans that offer a wider variety of drugs makes Part D more popular than the Veterans Affairs Drug program that tightly regulates the drugs it offers.[35]

In 2005, prior to full implementation of the law in 2006, the Congressional Budget Office (CBO) estimated that spending on the drug benefit in 2012 would be $126.8 billion. Actual spending on the program was $55 billion, 57 percent below the CBO’s 2005 estimate.[36] Recent research by CBO shows that there are more insurers competing to offer plans in Part D than anticipated, which has helped hold down cost, because more competition translates into lower prices.[37]

There have been various attempts to explain the discrepancy in costs, with one explanation being that enrollment levels are lower than initially anticipated. However, Joseph Antos of the American Enterprise Institute has pointed out that lower enrollment represents only about 17 percent of lower than projected cost experience.[38] As a result, the bulk of the reduced cost experience is attributable to other factors, such as competition among drug plans to reduce prices as well as increased use of generic drugs.[39]

Lessons from Airline and Trucking Deregulation

Although health care has unique features as a service industry, it is not the only sector of the American economy that has experienced overly excessive regulation. The airline and trucking industries were previously much more heavily regulated than they are today, but both underwent large and positive transformations with price deregulation. The evidence of what occurred in those industries is instructive.

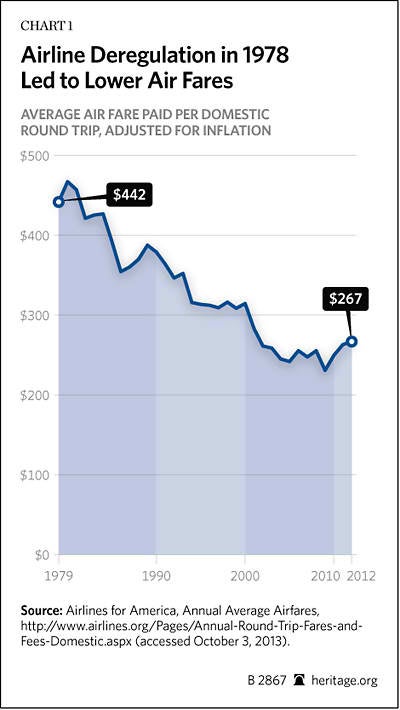

Airlines. From the late 1930s through the late 1970s, the Civil Aeronautics Board (CAB) regulated all domestic airline routes and determined prices, routes, and schedules. Concerned that these regulations were fostering inefficiency and unnecessarily raising costs, President Jimmy Carter initiated a program of substantial deregulation of the industry. In 1978, he signed into law the Airline Deregulation Act of 1978 that gradually phased out the CAB’s ability to set prices, lowered barriers to entering the airline industry, and gave airlines greater flexibility to use less frequently traversed routes.[40] In the 30-plus years since airline deregulation’s inception, the results have been astounding:

- Airline deregulation has reduced costs for consumers by an estimated $19 billion to $20 billion per year.[41]

- Deregulation led to the evolution of the classic hub-and-spoke system in Charlotte, Detroit, Phoenix, St. Louis, and many other cities. Those living near these cities have far more options for flights and destinations. Additionally, those living in small cities on the spokes of the hub have access to myriad destinations via the hubs.[42]

- Deregulation has allowed entrepreneurs to build successful new companies like Southwest and JetBlue that have transformed the industry with low-price, short point-to-point service.[43]

Chart 1, based on airfare data from the U.S. Department of Transportation, illustrates the decline in the average air fare as a result of the Airline Deregulation Act of 1978.[44]

Contrary to what the skeptics had argued, deregulation did not diminish the safety of air travel. The airline industry has been able to produce exactly what its consumers want: high-quality travel, particularly in terms of safety, at much lower cost.[45]

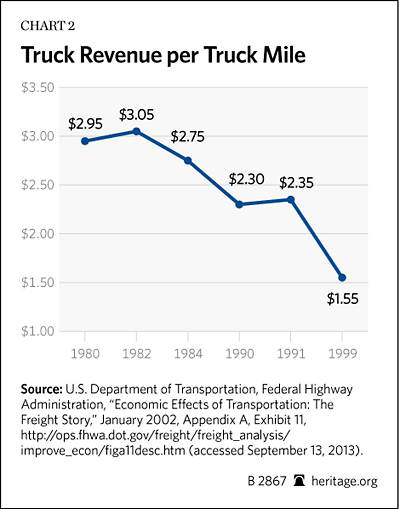

Trucking. Since 1935, the trucking industry has been controlled by the Interstate Commerce Commission (ICC), which previously imposed heavy regulations that restricted entry into the market (and thus protected incumbent companies), as well as the prices and routes of carriers. After it became apparent that overregulation was unnecessarily increasing costs, Senator Ted Kennedy (D–MA) worked with President Carter to deregulate the industry. In 1980, President Carter signed the Motor Carrier Act of 1980, which restricted the ICC’s regulatory authority over the industry.[46] Like the Airline Deregulation Act, the Motor Carrier Act eased entry into the market, generated greater flexibility in choosing routes by competing companies, and allowed more market-based pricing by the companies themselves. Once again, the results were extremely positive:

- Competition in the industry grew dramatically. A decade after deregulation, the number of licensed carriers in the industry had more than doubled.[47]

- Costs for consumers fell. Shipping rates for all but the largest shipments dropped by as much as 40 percent following deregulation.[48]

- Inefficient firms were eliminated from the market. Just four years after the Motor Carrier Act had been signed into law, the number of companies that had ceased intercity operations had increased nearly tenfold. [49]

- A marked increase in truckers’ ability to offer on-time and flexible service made business easier for manufacturers.[50]

Chart 2 depicts the decline in trucking rates in terms of truck revenue per truck mile (in dollars) over the course of the first 19 years after deregulating the industry.[51]

Conclusion

An important component of the national debate on health care is cost-estimation. Reform plans should be evaluated based not only on how they affect federal spending and taxation but also how they affect private health insurance premiums and insurance coverage rates.

Reforms that rely heavily on regulation and governmental control are relatively easy for the estimators to assess. For instance, if the government imposes a cap on health spending, most models reflexively assume that the cap will hold down costs (despite much real-world evidence to the contrary). These models fail to capture the subsequent erosion in quality that would occur as a result of such caps.

It is far more difficult for researchers to assess what would happen with market-driven reforms because such reforms rely so heavily on incentives to influence behavior, not mandates and controls. For instance, both the CBO and Centers for Medicare and Medicaid Services vastly overestimated the cost of the Medicare drug benefit during its first seven years of operation.[52] Although it is difficult to estimate the effects of market-driven reforms, it is by no means impossible. As indicated in this paper, there is an abundance of microeconomic evidence that consumers behave rationally when confronted with market signals in health care. They will seek out high-value, lower-cost options when they are spending their own money, as has been exemplified by Medicare part D, tests of CDHPs, and other demonstrations of consumer incentives.

These market-based approaches rely on defined contribution systems to support insurance purchases by consumers, which have far more potential to control costs, as illustrated in recent research published in the Journal of Law, Medicine, and Ethics.[53]

Based on this plethora of evidence, one can have a great deal of confidence that a market-driven health system would work as one would expect it to—driving out waste and inefficiency and rewarding high quality and lower costs with greater market share. Fortunately, these benefits of competition in health care are starting to become more widely appreciated, even in key government agencies. The CBO recently issued a report quantifying the federal budgetary savings that would result from migrating Medicare toward a competitive premium support system.[54 ]It is very important to build upon this growing confidence in competition so that, in the future, consideration by Congress of health reform plans that relay on markets and competition is done with a full understanding of the benefits such plans would produce for consumers, the federal budget, and the American economy.

—James C. Capretta is a Senior Fellow at the Ethics and Public Policy Center. Kevin D. Dayaratna is Research Programmer and Policy Analyst in the Center for Data Analysis at The Heritage Foundation.