Under federal tax law, individuals may deduct the income and property taxes that they pay to their state and local governments. In recent years, individuals have been allowed to choose between deducting their income tax or sales taxes.[1] Because federal tax deductions effectively spread the costs of these deductions across all taxpayers in the form of higher federal tax rates, the state and local tax deduction forces federal taxpayers in low-tax states to subsidize taxpayers in high-tax states. Distributional impacts within states force low-income residents to subsidize high-income residents.

If the state and local tax deduction were eliminated, federal income tax rates could be reduced by as much as 12.5 percent. Ending the federal subsidy of state and local taxes would help to improve the fiscal discipline and economic efficiency of state and local governments by forcing state and local taxpayers to bear the full burden of their governments’ costs.

The State and Local Tax Deduction

The state and local tax deduction has been around since the inception of the federal income tax in 1913. The rationale for it is that since state and local taxes reduce individuals’ after-tax income, the income used to pay those taxes should be excluded from federal taxation. That argument has merit.

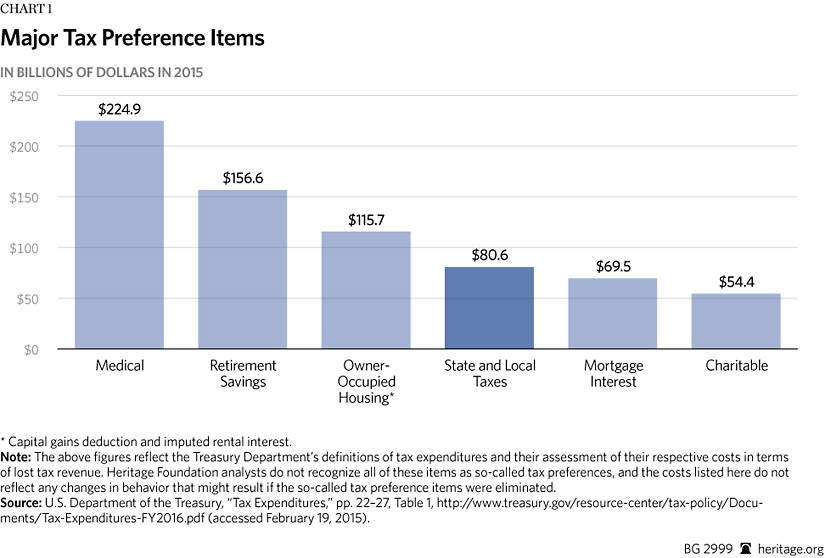

In practice, however, the deduction allows states to raise taxes higher than they otherwise would and has significant perverse distributional impacts, redistributing income from the poor to the rich and from people in low-tax states to people in high-tax states. Despite some efforts to eliminate it, the deduction for state and local taxes remains one of the largest deductions in the federal tax code. According to The Heritage Foundation’s Individual Income Tax Model (HFIITM), the state and local tax deduction will reduce federal tax revenues by an estimated $90 billion in 2015. This makes the state and local deduction one of the largest “tax preference” items.

Economics of the Deduction

Any tax deduction reduces the tax base and therefore requires higher marginal tax rates to maintain the same level of tax revenue. Ideally, deductions should be kept to a minimum after the appropriate tax base has been established. Yet the U.S. tax code is littered with numerous deductions and exemptions as political and special interests have interfered with economically efficient taxation. The federal deduction for state and local taxes turns high-tax states into one of those special interests.

Who Benefits?

The federal deduction for state and local taxes creates both winners and losers.

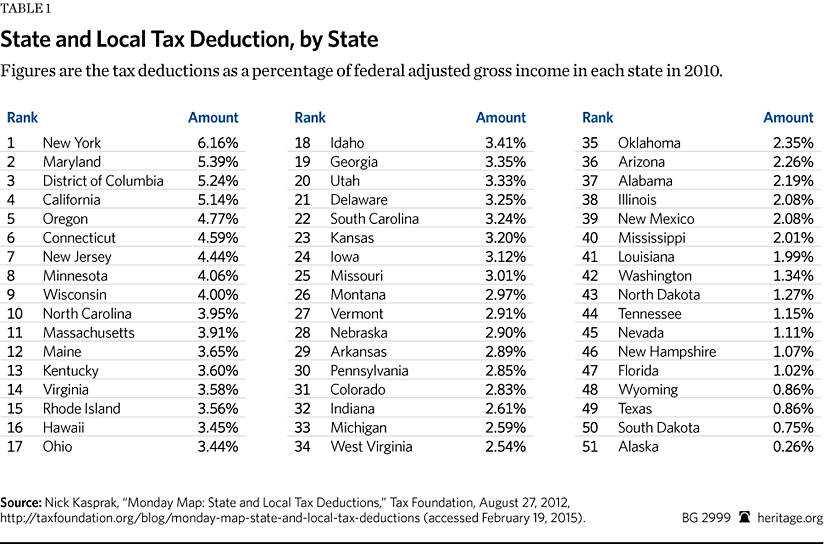

States with High Taxes. States with higher income and property taxes receive the greatest benefit from the state and local tax deduction. According to the Tax Policy Center, New York and California received more than 30 percent of the value of the state and local tax deduction in 2011, yet their residents make up only 12 percent of the U.S. population.[2] Not surprisingly, New York and California place first and fourth, respectively, in total state and local tax burden.[3] Just 10 states receive 62 percent of the value of the state and local tax deduction. On average, taxpayers in these 10 states receive a $4,200 deduction while taxpayers in the remaining 40 states and the District of Columbia receive a $2,300 deduction.[4]

The state and local tax deduction effectively reduces states’ marginal tax rates, allowing them to collect higher taxes while shifting some of the burden from their own taxpayers to taxpayers in other states. For example, the state of California has a top marginal tax rate of 9 percent, but the state and local tax deduction reduces this to an effective 5.4 percent. This is because the federal government reimburses state taxpayers up to 40 cents of each dollar they pay in state taxes. Thus, while California’s government keeps every dollar of state tax revenue, only part of that revenue comes from California residents. The rest comes from the federal government in the form of reduced federal tax receipts.

Higher-Income Taxpayers and Itemizers. The deduction for state and local taxes creates winners and losers within states, too. Higher-income taxpayers win while lower-income taxpayers lose.

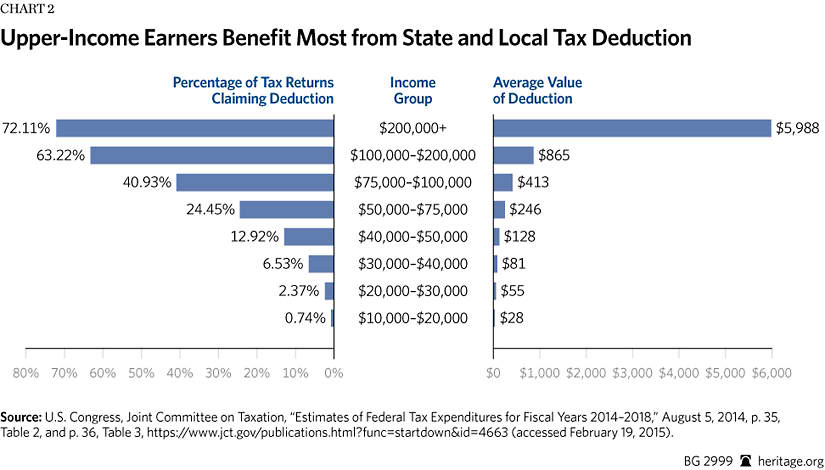

The state and local tax deduction is available only to taxpayers who itemize their deductions: single taxpayers with more than $6,300 in total deductions and married taxpayers with more than $12,600 in deductions for 2015. This means that more than 70 percent of all taxpayers receive no benefit from the state and local tax deduction. Those who receive no benefit tend to have lower incomes: Only 16 percent of taxpayers making less than $30,000 itemize their deductions while more than 95 percent of taxpayers with incomes of $200,000 or more itemize.[5]

The distribution of the value of the state and local tax deduction is even more skewed than that of those claiming it. According to the Congressional Budget Office (CBO), 80 percent of the value of the state and local tax deduction goes to the top 20 percent of taxpayers.[6] This is because higher-income individuals not only pay more state and local taxes, but also face higher marginal tax rates at the federal level. A $10,000 deduction for a middle-income family produces a $1,500 reduction in their federal taxes while a $10,000 deduction for a very high-income family nets them nearly $4,000.

Deduction Subjects Federal Tax Revenues to the Whim of State Governments

By allowing individuals to deduct the taxes paid to their state and local governments, federal revenues become contingent on states’ level of taxation. If states raise taxes, individuals deduct more in state taxes and federal tax revenues decline. On the other hand, if states lower their taxes, individual deductions decline and federal tax revenues rise.

This leaves the federal government with less control over its collection of taxes. For example, the tax increases contained in Illinois’ Taxpayer Accountability and Budget Stabilization Act generated an additional estimated $25.7 billion in tax revenues for the state between 2011 and 2014.[7] But those same tax increases directly reduced federal tax revenues.

While the amount these tax increases reduced federal tax revenues is unknown, the effects were certainly significant and likely amounted to billions of dollars in lost federal tax revenues.[8]

Eliminating the State and Local Tax Deduction

The Heritage Foundation’s Center for Data Analysis estimated the static impact on federal tax revenues of eliminating the state and local tax deduction using The Heritage Foundation Individual Income Tax Model (HFIITM). This analysis marks the first use of the new model, which estimates the static impact of changes in federal tax policy on the overall revenues and distribution of federal taxes. Because this is the first analysis published using the model, we have detailed its structure and capabilities in the Appendix.

We estimate that eliminating the state and local tax deduction would increase federal income tax revenues by about 6.1 percent ($1.3 trillion) over the next 10 years (2016–2025). Previous estimates from the CBO and the Joint Committee on Taxation show smaller revenue gains over a 10-year window, but those estimates reflect earlier periods. For example, the CBO estimated in 2011 that repealing the state and local tax deduction would increase federal tax revenues by $862 billion over 10 years.[9] The Tax Policy Center estimated that a 2013 update to this estimate would translate into about $1.1 trillion in additional revenues.[10] Our current estimate reflects the 2016–2025 time period.

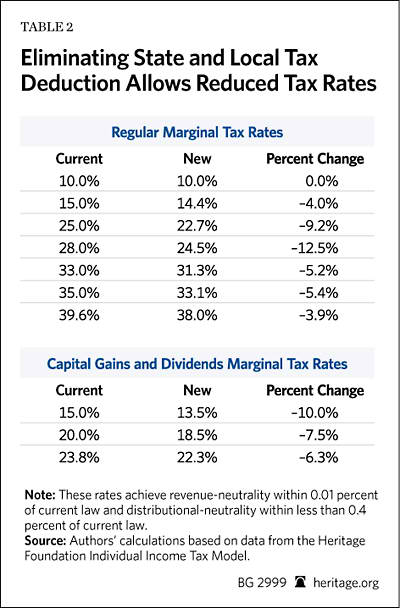

Replacing the Deduction with Reduced Rates. The purpose of eliminating the state and local tax deduction is not to generate new federal tax revenues, but to rid the tax code of inefficient policies. Thus, Congress should offset the removal of any deductions with a reduction in marginal tax rates. If the revenues from eliminating the state and local tax deduction were used to lower rates to maintain revenue neutrality and distributional neutrality with the current tax code, marginal tax rates would decline by up to 12.5 percent.[11]

Our analysis found that removing the state and local tax deduction and replacing it with a revenue-neutral and distribution-neutral reduction in marginal tax rates would produce the largest tax reductions for the 25 percent and 28 percent tax brackets, which would decline by 9.2 percent and 12.5 percent, respectively. The 15 percent and upper-income rates would all decline between 3 percent and 5 percent.

Although we did not dynamically model the macroeconomic effects of replacing the state and local tax deduction with lower marginal income tax rates, such a policy could generate positive macroeconomic impacts. Whereas the state and local tax deduction does not promote economic growth, but rather encourages adverse economic policies at the state level, eliminating it could reduce the negative effects of bad state policies. If accompanied by more efficient state tax and spending policies, replacing the state and local tax deduction with lower federal tax rates would spur economic growth.

The Potential Impact on State Policies

Eliminating the state and local tax deduction could increase accountability in state governance and reduce wasteful spending.

Without the federal government picking up a piece of their state and local tax burden, many taxpayers would face a significantly higher effective state tax burden that could drive some individuals and small businesses out of high-tax states and into lower-tax ones. This competition in state taxation would be good for individuals and businesses because it would make states more accountable for all of the tax revenue they collect.

Increased accountability would lead to more equitable and efficient taxation at both the state and federal level. Absent the deduction, taxes would be distributed more equitably according to services received. When faced with the full cost of services received, taxpayers would likely demand fewer services and a more efficient allocation of their tax dollars, leading to a more optimal overall level of taxation.

The Effect on Individuals

Despite seeming like an increase in federal taxes (or an increase in effective state taxes) for anyone who claims the state and local tax deduction, eliminating the deduction could reduce many of these taxpayers’ federal tax liabilities if coupled with a corresponding reduction in federal marginal tax rates.

The state and local tax deduction has adverse impacts that outweigh its benefits and should be eliminated for that reason. However, Congress should use the additional revenue that would be generated to reduce marginal income tax rates for all federal taxpayers, not simply add it to the federal government’s coffers. If marginal tax rates were reduced in a revenue-neutral and distributionally neutral manner, the more than 70 percent of taxpayers who do not itemize would face lower combined federal and state income tax burdens. Additionally, this could lower overall taxes for some taxpayers who itemize but who have relatively lower incomes or live in lower-tax states.

In addition to the immediate change in federal tax liabilities, eliminating the state and local tax deduction could lead to lower state and local taxes, which could ultimately mean that even those currently receiving large benefits from the deduction would experience an eventual decline in their combined state and local tax burden.

Conclusion

Assuming an appropriate tax base has been established, most tax deductions and exclusions are not efficient because they require higher marginal tax rates. The state and local tax deduction fits this description because it supports detrimental economic policies: high levels of taxation and inefficient and wasteful government spending. Furthermore, it subjects federal tax revenues to the whim of state governments, while benefiting wealthy taxpayers and high-tax states.

Eliminating the state and local tax deduction would encourage a more efficient tax system, and a corresponding reduction in marginal federal income tax rates could boost economic growth. The U.S. tax code needs serious reform, and eliminating the state and local tax deduction is one step in that direction.

—Rachel Greszler is Senior Policy Analyst and Kevin D. Dayaratna, PhD, is Senior Statistician and Research Programmer in the Center for Data Analysis, of the Institute for Economic Freedom and Opportunity, at The Heritage Foundation.

Appendix

The Heritage Foundation’s Individual Income Tax Model (HFIITM) is a statistical model for forecasting tax revenues. The model uses data from the 2007 Statistics of Income Public Use Tax File from the Internal Revenue Service.[12] This is a stratified sample of the American population consisting of approximately 143,142 tax filing records. The data blur certain information, such as state of residency, for high-income tax filers (those with adjusted gross incomes over $200,000).

The model and data are based off the IRS’s 2007 F1040 form and includes most variables, or lines, contained in this form. Some lines are excluded from the IRS dataset and therefore cannot be disaggregated within the model.

To establish a base-case scenario, the HFIITM model generates a random sample (a sequence of independent and identically distributed random variables) from the original 2007 dataset and “ages” each observation of this sample over subsequent years through 2025. Specifically, the sample from the original 2007 data is used to generate subsequent observations of data for 2008, and then the 2008 data are used to generate 2009 data, and the process continues.

Each random sample consists of 1 million observations. Each time an alternative scenario is tested or “scored” by the model, a new base case scenario is developed. Due to the large sample size of 1 million observations, the base case scenario does not differ significantly from one run to another.

The aging of the data from 2007 to 2025 includes both targeted aging based on actual data available from the IRS through 2012 and applied growth rates. For nearly all variables, additional aggregate IRS data from 2012 are used to apply a steady growth rate between 2007 and 2012. Beyond 2012, variables are grown according to what are deemed appropriate growth rates. For example, variables related to income are grown according to presumed income growth rates, and education-related and health-related tax components are grown according to their estimated cost growth. The tax parameters for 2015 and beyond are adjusted for inflation and income as determined by current tax law. Aggregate revenues are computed using the law of large numbers, which states that for a sufficiently large sample size, the mean of a random sample converges to the population mean.[13] Although cyclical growth is expected, the HFIITM—like most other microsimulation models—does not attempt to model such cyclical growth. Instead, the HFIITM assumes steady state growth. Because of this assumption of steady state growth, additional aggregate data from 2012 were used to adjust the growth rates of most variables between 2007 and 2012. Without this adjustment, the estimated growth rates create significantly higher values for many of the variables than actually occurred.

For this first simulation using the HFIITM, we ran a baseline scenario based on current policy and juxtaposed this against an alternative scenario that eliminates state and local tax deductions for years 2015 and beyond. The differences between the two scenarios are based on comparing overall revenues after refunds and credits.