It is not obvious that the Fed should be involved in emergency lending, however, since expectations of such lending can increase the likelihood of crises. Arguments in favor of this role often misread history. Instead, history and experience suggest that the Fed’s balance sheet activities should be restricted to the conduct of monetary policy.

—Renee Haltom, Research Department Editorial Content Manager,

and Jeffrey M. Lacker, President,

Federal Reserve Bank of Richmond, July 2014

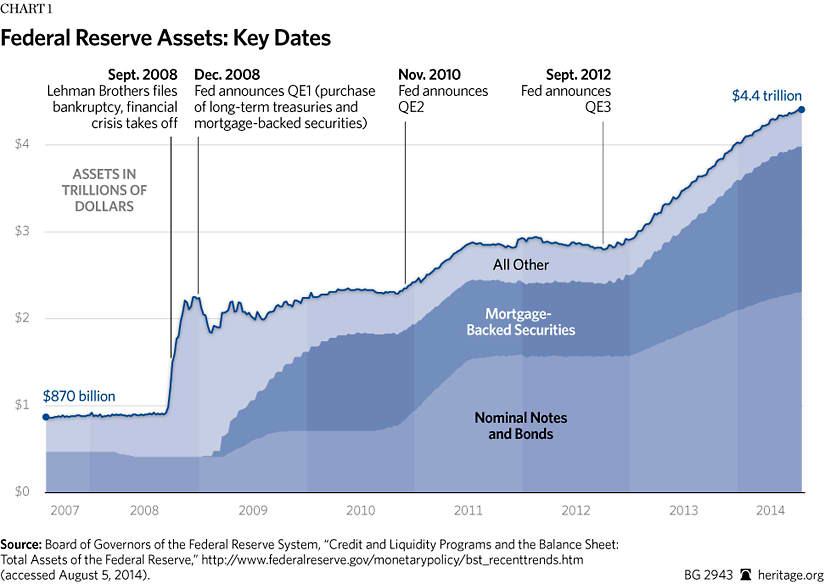

The Federal Reserve’s actions during the 2008 financial crisis have sparked debate over a wide range of monetary policy issues. Policymakers have been actively questioning everything from the effectiveness of the Fed’s policies to the financial strength of the Federal Reserve itself. (See Chart 1.) This Backgrounder focuses on one particular topic in which recent Fed actions have rekindled interest: the Federal Reserve’s role as a lender of last resort.

As the name suggests, a lender of last resort (LLR) is supposed to provide credit when funds are not available from any other source. The classic LLR prescription for a central bank—the very meaning of the term—was developed over the century prior to the Fed’s creation. Even though private institutions had successfully provided LLR services in the U.S., the LLR role was one of the initial functions given to the Fed when it was created in 1913.

The essence of the classic LLR prescription is to avoid lending to financially troubled firms and, whenever possible, avoid lending to specific institutions as opposed to ensuring the systemwide flow of credit. Overall, the Fed has not adhered to the classic LLR prescription. In other words, the Fed has rarely acted as the LLR it was designed to be. During its early years, the Fed likely made the Great Depression worse because it failed to adequately fulfill its LLR role. Furthermore, throughout its history, the Federal Reserve has repeatedly lent to financially troubled firms, thus jeopardizing its operational independence and putting taxpayers at risk.

Most recently, the Fed facilitated bailouts to financially weak firms by invoking its so-called emergency lending authority.[1] Congress can easily avoid these problems by prohibiting the Fed from making these types of loans in the first place. There is, in fact, no clear economic rationale for the Fed to provide direct loans to private firms. Given the development and current sophistication of financial markets, there is even less reason to allow the central bank to serve as a LLR now than there was in 1913.

Brief Historical Perspective: What Is a Lender of Last Resort?

The classic prescription for a lender of last resort was developed in the 19th century. Henry Thornton, a member of Parliament and a monetary theorist, produced the first systematic treatment of the issue in his 1802 work titled An Enquiry Into the Nature and Effects of the Paper Credit of Great Britain. Walter Bagehot, longtime editor of The Economist, later refined and built upon Thornton’s ideas in his 1873 work, Lombard Street.[2]

The combined works of Thornton and Bagehot effectively defined the LLR function and formed what is recognized as the benchmark for any central bank’s LLR policy. The following two norms summarize the essence of this classic LLR policy:

- The central bank should prevent panic-induced contractions of the economy’s stock of money.

- During a crisis, the central bank should provide short-term loans to all solvent institutions, on good collateral, at a high rate of interest.

The main focus is on preventing a short-term shrinkage of the money supply from turning into a full-blown economic contraction. The central bank accomplishes this task by managing the monetary base, a measure that consists of currency in circulation plus commercial banks’ reserves. Economists refer to the base as high-powered money because the central bank controls how much of this money exists, and because the base ultimately determines the maximum quantity of money that can be created in the banking system.[3]

According to the classic prescription, the central bank’s main goal should be to prevent the base from shrinking so that banks can easily expand the currency as needed. During a banking panic, for instance, the base could contract sharply if too many bank customers rush to withdraw deposits from their banks. If, for example, large numbers of bank customers doubted the safety and soundness of their banks, their rush to withdraw deposits would force banks to use reserves to pay customers.[4]

If this demand for base money cannot be accommodated, people may simply hold money rather than spend it, thus leading to a contraction in the goods and services sectors of the economy. By serving as the LLR, the central bank can accommodate this extra money demand to prevent the economic contraction. Thus, the central bank’s LLR function can be seen as a responsibility to the entire economy. That is, the central bank can prevent panic from spreading to the broader economy by ensuring that the entire banking system has enough base money (that is, enough liquidity).

The classic prescription made clear, however, that a central bank had no duty to save specific firms. This idea was particularly important during the 19th century because monetary policy was typically conducted by lending directly to banks. To prevent having to sustain insolvent private banks, the central bank was to lend only at a high rate and only to borrowers who could post sound collateral. Also, any such loans were to be on a very short-term basis, at most a few days. These protections—temporary loans, only to sound institutions at above-market interest rates—were meant to minimize the amount of undue risks that banks would take on account of having access to central bank credit, the so-called moral hazard problem.

In other words, if central banks provide liberal credit to private banks on a regular basis, the knowledge of having easy access to these loans would likely encourage private banks to take on too much risk. Thornton, in particular, recognized that providing such generous credit would likely “encourage their improvidence.”[5] Lending at a high rate of interest also insured that any central bank loans—which effectively served as additional base money—would be removed from the system as quickly as possible, thus guarding against inflation. Prior to the creation of central banks, private markets fulfilled the LLR function on their own through institutions such as clearinghouses.

Pre-Federal Reserve LLR: The Clearinghouse. In the U.S., prior to the creation of the Federal Reserve System, private banks known as clearinghouses acted as bankers’ banks and served as lenders of last resort.[6] Clearinghouses grew out of associations of banks that gave one member the authority to settle—to “clear”—the amounts the association’s banks owed each other. As customers made withdrawals and deposits, the clearing bank transferred the proper amounts among the various banks. (This process is analogous to the modern usage of checks, whereby a bank allows its customers to deposit checks from other banks.) To facilitate this process, member banks kept a portion of their reserves at the bank designated as their central clearinghouse.

By the early 1900s, clearinghouses had played a key role in stemming banking panics by providing short-term loans to member banks. During the panic of 1837, for example, the Suffolk Bank provided LLR services through the Suffolk Banking System. These actions lessened the panic’s impact in the New England area relative to the rest of the country.[7] In the panic of 1857, clearinghouses issued “loan certificates” to commercial banks and used the banks’ own paper currencies as collateral. These loans, in turn, enabled banks to issue new currency and make loans to their own customers, thus containing the panic.[8]

In 1907, the six largest nationally chartered banks in New York used New York Clearing House loan certificates to help stem a panic. These New York banks borrowed “in amounts that appear to have exceeded their own private needs, providing liquidity for the entire New York money market.”[9] The short-term clearinghouse loans ultimately served as “bridge loans,” temporary financing that gave banks time to finance the importation of additional gold to build up their reserves. Even though these clearinghouses acted as a LLR without specific legal authorization to do so, their actions successfully stemmed several panics from spreading.[10]

Clearinghouses even organized their own bank examiners to monitor the safety and soundness of their member banks. Nonetheless, the successful operations of the clearinghouses were not sufficient to outweigh the many problems with the 19th-century U.S. banking system. For starters, branch banking was largely prohibited, thus tying the financial success of each bank to its own local economy. After the Civil war, a key problem was that banks, which at that time issued their own currencies, were prohibited from issuing their notes without adequate backing of U.S. government bonds.

Not only was the process of acquiring bonds cumbersome, but the Treasury maintained a consistent effort to retire the nation’s war debt, thus making the bonds increasingly scarce.[11] After 1865, state-chartered banks faced a similar problem because the federal government placed a prohibitive 10 percent tax on state-chartered banks’ currency issues. Another difficulty was that regulations prohibited even the temporary relief from strict reserve requirements during a crisis. During the panic of 1907, one prominent 20th-century banker noted, “While one thousand millions of dollars were lying idle in our banks and trust companies as so-called reserves, this money, by virtue of the law, could scarcely be touched!”[12]

All of these problems contributed to seasonal currency shortages, which were sometimes severe. The nation’s banks simply could not expand the currency supply quickly enough to meet demand, and the problem was due almost exclusively to restrictive government regulations. As these currency shortages grew more numerous and severe, political momentum grew to “fix” the banking problems. Although the U.S. ended up with a central bank, there were actually several major banking reform proposals around the turn of the 20th century that were closely based on the private clearinghouse system.[13] The Federal Reserve was created by essentially nationalizing the clearinghouses in a way that destroyed their effectiveness—a problem that led to currency shortages during the Great Depression.

The Federal Reserve as a Lender of Last Resort

The Federal Reserve, created in 1913, has used several different methods throughout its history to fulfill its LLR function. The main method has been through the open-market operations that the Fed uses to manage the monetary base. Through these operations, the Fed has regularly provided liquidity to the entire market by purchasing Treasury securities, and these operations can be temporarily expanded in the event of a crisis.

These purchases add reserves to the banking system, thus flooding the federal funds market—a private market where banks lend reserves to each other—with additional funds. This injection of reserves tends to lower the federal funds rate (the rate that banks charge each other to lend in this market) thus providing banks easier access to a highly liquid source of borrowing.[14] The federal funds market, therefore, provides a way for the Fed to add to the monetary base—even if only temporarily—and to allow banks to allocate credit to specific institutions as they see fit.

Unfortunately, it took the federal funds market several years to develop, and the Fed bungled its LLR function twice during the first 25 years of its existence. In particular, the Fed failed to provide any sort of liquidity to the banks it was supposed to serve, and likely made the Great Depression much worse than it otherwise would have been. In 1929, the Federal Reserve Board prohibited the extension of credit to any member bank that it suspected of stock market lending, a decision that ultimately led to a 33 percent decline in the economy’s stock of money.[15] Then, in 1937, the Federal Reserve Board of Governors—in alliance with the U.S. Treasury Department—doubled member banks’ required reserves, again preventing credit from expanding when and where it was needed.[16]

In several specific crises, though, the Fed successfully used open-market purchases to carry out its LLR function. For instance, after the 1987 stock market crash, prior to the Y2K computer scare, and in the wake of the 9/11 terrorist attacks, the Fed temporarily expanded its normal open-market Treasury purchases. In these cases, the Fed also made clear public announcements that it was doing so specifically to provide temporary liquidity.[17] Providing liquidity in this manner, through purchasing additional Treasuries, adhered to the classic LLR prescription because it temporarily expanded the base, thus providing all banks the means to allocate additional credit as needed rather than allowing the Fed to single out particular institutions. These successful examples are outnumbered, though, by many instances of the Fed failing to stick to the classic LLR methods through direct-lending procedures.

The Fed’s Discount Window and Special Programs. The Fed lends directly to banks (depository institutions) through its discount window, a method of lending that was originally envisioned as the main tool of monetary policy.[18] Initially, each District Reserve Bank had a physical discount window in its lobby to make these loans to member banks. The term now refers more generally to the regular provision of credit, as opposed to emergency credit, by the central bank to individual depository institutions on pre-defined terms.[19] Long before the 2008 crisis, the Fed’s discount window lending was the source of much controversy with respect to proper LLR operations.

From its inception, the Fed broke with the classic LLR tradition by lending continuously through the discount window rather than only on a temporary basis. As of August 31, 1925, for instance, 593 member banks had borrowed continuously from the Fed for at least one year. Of these banks, 239 had been borrowing continuously since 1920, and 122 since before 1920.[20] The Fed also estimates that at least 80 percent of the 259 member banks that failed between 1920 and 1925 were habitual borrowers at the discount window prior to their failure.[21] Furthermore, the Fed deviated from the classic LLR prescription with respect to the types of loans permitted as well as the types of borrowers that were extended credit.

One of the first troublesome expansions of discount window lending came in 1932 when the Glass–Steagall Act added Section 13(3) to the Federal Reserve Act.[22] This change opened the Fed’s discount window to nonbanks—individuals, partnerships, and corporations—in “unusual and exigent circumstances.”[23] Another major change was instituted when the 1934 Industrial Advances Act created Section 13(b) in the Federal Reserve Act. Section 13(b) authorized the District Banks to provide working capital loans directly to industrial and commercial businesses, for periods of up to five years without any limitations as to the type of collateral.[24] By 1939, the district banks had provided nearly $200 million in working capital loans to nearly 3,000 applicants.[25] These loans did not fit the classic LLR prescription because they provided firms with a substitute for private capital.

In 1946, the Federal Reserve Board unsuccessfully sought to eliminate its own Section 13(b) authority. Section 13(b) was repealed years later with the passage of the Small Business Investment Act of 1958. During the congressional debate on the 1958 bill, Fed Chairman William McChesney Martin testified to Congress that the Fed should not provide capital to institutions and that its primary objective should be “guiding monetary and credit policy.”[26] Roughly 20 years later, the Fed appropriately refused to open the discount window when the Nixon Administration asked the New York Fed to provide loans to financially troubled Penn Central Railroad.

That success was short-lived, though, and the Fed immediately followed that refusal with what monetary scholar Anna Schwartz called “the ‘too-big-to-fail’ doctrine in embryo.”[27] Ostensibly worried about fallout from Penn Central’s bankruptcy—particularly its default on $82 million in commercial paper—the Fed announced that it would provide discount window lending to banks to assist in meeting the needs of all businesses that could not issue new commercial paper. Thus the Fed showed it would go to great lengths to stem a financial crisis in the event a large firm, not even a financial firm, might fail. This action, of course, implied that the bankruptcy of a large firm would cause a financial crisis, although no analysis, only conjecture, establishes such a position.

Another major break with traditional LLR lending occurred in 1974 when the Fed provided discount window loans to Franklin National Bank until the Federal Deposit Insurance Corporation (FDIC) could find a buyer for the failed bank. For five months, the New York Fed lent continuously to Franklin for a total of $1.75 billion, approximately 50 percent of Franklin’s assets. Schwartz argues that this event marked a shift from short-term assistance to the long-term support of an insolvent institution pending final resolution.[28] A similar approach was taken with regard to Continental Illinois when the Fed lent as much as $8 billion over the course of one year until the FDIC resolved the failed bank in 1985.[29] These actions clearly went well beyond providing temporary liquidity to solvent banks.

Evidence also suggests that the Fed was continuously providing capital loans to many troubled banks during the late 1980s and early 1990s. A House Banking Committee reported that of the 530 depository institutions that failed from January 1985 to May 1991, 437 had been formally rated with the poorest CAMEL rating of “five” (most problem-ridden), and 51 had the next poorest rating of “four.”[30] The whole class of CAMEL-five-rated banks had been allowed to operate for a mean period of one year. At the time of actual failure, 60 percent of the banks had outstanding discount window loans for an aggregate of roughly $8 billion.[31] Since the Fed knew the banks had such poor CAMEL ratings, it clearly failed to follow the classic LLR prescription.

Prelude to the 2008 Financial Crisis: Amendment to Section 13(3) Lending Authority. The next major change to the Fed’s lending authority came when the 1991 Federal Deposit Insurance Corporation Improvement Act (FDICIA) amended Section 13(3) of the Federal Reserve Act. This change weakened the collateral restrictions on emergency lending so that the Fed could lend directly to securities firms in times of financial crises.[32] In 1992, Schwartz predicted “the provision in the FDIC Improvement Act of 1991 portends expanded misuse of the discount window.”[33]

In 1993, Cleveland Fed attorney Walker Todd pointed out that “[i]ronically, while the principal thrust of the FDICIA was to limit or reduce the size and scope of the federal financial safety net…this provision effectively expanded the safety net.”[34] Historically, banks were amenable to lending to securities firms during liquidity crises at least partly because they themselves could rely on the Fed providing liquidity. The 1991 amendment changed this arrangement by making it unnecessary for securities firms to rely on banks for such credit. Schwartz’s and Todd’s warnings proved accurate, and the Fed invoked its expanded Section 13(3) authority in the midst of the 2008 financial crisis.

Fed Lending Programs During the 2008 Financial Crisis. During the recent financial crisis the Fed allocated credit directly to several firms and also provided loans through several broader lending programs. For instance, the Fed provided a $13 billion loan to Bear Sterns, one of the Fed’s largest primary dealers, on March 14, 2008. The loan was repaid in days, but then the Fed provided a $30 billion loan to facilitate JPMorgan Chase’s acquisition of Bear Sterns (via a special purpose vehicle named Maiden Lane, LLC). Shortly after this deal was completed, former Fed chairman Paul Volcker remarked that this loan was “at the very edge” of the Fed’s legal authority.[35]

Separately, the U.S. Government Accountability Office (GAO) estimates that from December 1, 2007, through July 21, 2010, the Federal Reserve lent financial firms more than $16 trillion through its Broad-Based Emergency Programs.[36] To put this figure in perspective: Annual gross domestic product (GDP) reached $16.8 trillion in 2013, an all-time high for non-inflation-adjusted GDP in the U.S. During the crisis, the Fed created more than a dozen special lending programs by invoking its emergency authority under Section 13(3) of the Federal Reserve Act.

Most of these special programs were shut down by 2010, although approximately $2 billion from some of the lending facilities remains on the Fed’s balance sheet.[37] The following list provides just a few examples of the emergency lending carried out by the Fed in the wake of the 2008 crisis.[38]

While Bear Stearns did use the PDCF before the Fed facilitated the Bear Stearns–J.P. Morgan merger, three other primary dealers—(1) Citigroup Global Markets, Inc.; (2) Merrill Lynch Government Securities, Inc.; and (3) Morgan Stanley & Co., Inc.—relied on the PDCF for more than double the amount that Bear Stearns borrowed.[40] Of more than 20 primary dealers, almost 80 percent of all the lending through the PDCF went to just these four firms.[41] Furthermore, the Fed made special concessions on the type of collateral accepted for these loans, and it provided PDCF loans at below market rates.[42]

Prior to the Lehman Brothers failure in 2008, high-grade bonds and government-sponsored enterprise-backed securities accounted for nearly all of the collateral used in these types of borrowings. After the Lehman Brothers failure, however, the Fed accepted equities and speculative grade debt as collateral for PDCF loans.[43] The Fed clearly relaxed credit standards relative to what was normally accepted in this short-term lending market. Although it is difficult to gauge the exact amount, evidence also suggests that the Fed provided favorable rates on most of its emergency lending programs.

Bloomberg Markets, for example, estimates that the Fed’s total emergency loans from 2007 to 2010 charged $13 billion below market rates.[44] Charging below market rates on suspect collateral is the exact opposite of the classic LLR prescription. The goal should be to lend as safely as possible at high rates so that firms have every incentive to stop relying on the Fed for funds. Instead, the Fed effectively provided financial institutions with a source of subsidized capital for up to several years. Critics argue that the 2008 liquidity crisis was atypical because market participants had difficulty determining the value of various securities. This difficulty does not justify emergency Fed loans, however, because the Fed has no particular advantage over anyone else in determining the market value of securities. Regardless of this issue, the recent lending programs are consistent with most of the Fed’s LLR history in that the central bank has regularly failed to adhere to classic LLR principles.

What Can Congress Do?

The bulk of the Fed’s LLR actions have been counter to the very principles that defined the LLR concept. In a few instances, however, the Fed has effectively fulfilled its LLR function by providing liquidity to the entire market rather than allocating credit to specific firms. Congress can improve the effectiveness of the Fed’s LLR activities by restricting the Fed to these types of temporary expansions of open-market operations. Specifically, Congress should:

- Revoke Section 13(3) of the Federal Reserve Act. This section allows the Federal Reserve Board of Governors to authorize Fed District Bank lending to “any participant in any program or facility with broad-based eligibility” in “unusual and exigent circumstances.” The 2010 Dodd–Frank Wall Street Reform and Consumer Protection Act amended this authority after the 2008 crisis, but even if these changes had been in place prior to the crisis, the Fed still would have been able to conduct roughly half of those lending programs.

- Close the Federal Reserve’s Discount Window. The discount window is a relic of the Fed’s founding and is no longer necessary. The Federal Reserve can adequately fulfill its lender-of-last-resort function through open-market operations and it does not need to provide credit to individual firms.

- Study the Federal Reserve’s Current Primary-Dealer System. The current primary-dealer framework was created in the 1960s when there were clearer advantages to having a centralized open-market system in New York. Now, however, there is good reason to believe that allowing all member banks to participate in open-market operations would provide a more liquid interbank lending market. At the very least, expanding the participants in open-market operations would make the federal funds market less dependent on any particular institution. Improvements to the framework should be formally examined.

Conclusion

Overall, the Fed has done a poor job of adhering to the classic lender-of-last-resort prescription. In other words, the Fed has rarely acted as the LLR it was designed to be. Throughout history, the Fed’s LLR policies have jeopardized its operational independence and put taxpayers at risk. These problems are easily avoidable, though, because there is no clear economic rationale for the Fed to provide direct loans to private firms. The implementation of monetary policy involves buying and selling securities to ensure that the federal funds market has sufficient liquidity. Monetary policy does not require the Fed to lend to individual firms.

There is little evidence that Federal Reserve lending to individual institutions is either necessary or proper, but doing so clearly politicizes the Fed’s monetary policy. Congress can easily avoid such politicization by prohibiting the Fed from making these types of loans in the first place. Using public funds in any way to bail out private firms, for any reason, is and should remain a part of the government’s fiscal operations: If Members of Congress want to use taxpayer dollars to save troubled firms, they should do so transparently so that voters may hold them accountable.

—Norbert J. Michel, PhD, is a Research Fellow in Financial Regulations in the Thomas A. Roe Institute for Economic Policy Studies, of the Institute for Economic Freedom and Opportunity, at The Heritage Foundation.