The story of how the Laffer Curve got its name begins with a 1978 article by Jude Wanniski in The Public Interest entitled, "Taxes, Revenues, and the 'Laffer Curve.'"1 As recounted by Wanniski (associate editor of The Wall Street Journal at the time), in December 1974, he had dinner with me (then professor at the University of Chicago), Donald Rumsfeld (Chief of Staff to President Gerald Ford), and Dick Cheney (Rumsfeld's deputy and my former classmate at Yale) at the Two Continents Restaurant at the Washington Hotel in Washington, D.C. While discussing President Ford's "WIN" (Whip Inflation Now) proposal for tax increases, I supposedly grabbed my napkin and a pen and sketched a curve on the napkin illustrating the trade-off between tax rates and tax revenues. Wanniski named the trade-off "The Laffer Curve."

I personally do not remember the details of that evening, but Wanniski's version could well be true. I used the so-called Laffer Curve all the time in my classes and with anyone else who would listen to me to illustrate the trade-off between tax rates and tax revenues. My only question about Wanniski's version of the story is that the restaurant used cloth napkins and my mother had raised me not to desecrate nice things.

The Historical Origins of the Laffer Curve

The Laffer Curve, by the way, was not invented by me. For example, Ibn Khaldun, a 14th century Muslim philosopher, wrote in his work The Muqaddimah: "It should be known that at the beginning of the dynasty, taxation yields a large revenue from small assessments. At the end of the dynasty, taxation yields a small revenue from large assessments."

A more recent version (of incredible clarity) was written by John Maynard Keynes:

When, on the contrary, I show, a little elaborately, as in the ensuing chapter, that to create wealth will increase the national income and that a large proportion of any increase in the national income will accrue to an Exchequer, amongst whose largest outgoings is the payment of incomes to those who are unemployed and whose receipts are a proportion of the incomes of those who are occupied...

Nor should the argument seem strange that taxation may be so high as to defeat its object, and that, given sufficient time to gather the fruits, a reduction of taxation will run a better chance than an increase of balancing the budget. For to take the opposite view today is to resemble a manufacturer who, running at a loss, decides to raise his price, and when his declining sales increase the loss, wrapping himself in the rectitude of plain arithmetic, decides that prudence requires him to raise the price still more--and who, when at last his account is balanced with nought on both sides, is still found righteously declaring that it would have been the act of a gambler to reduce the price when you were already making a loss.2

Theory Basics

The basic idea behind the relationship between tax rates and tax revenues is that changes in tax rates have two effects on revenues: the arithmetic effect and the economic effect. The arithmetic effect is simply that if tax rates are lowered, tax revenues (per dollar of tax base) will be lowered by the amount of the decrease in the rate. The reverse is true for an increase in tax rates. The economic effect, however, recognizes the positive impact that lower tax rates have on work, output, and employment--and thereby the tax base--by providing incentives to increase these activities. Raising tax rates has the opposite economic effect by penalizing participation in the taxed activities. The arithmetic effect always works in the opposite direction from the economic effect. Therefore, when the economic and the arithmetic effects of tax-rate changes are combined, the consequences of the change in tax rates on total tax revenues are no longer quite so obvious.

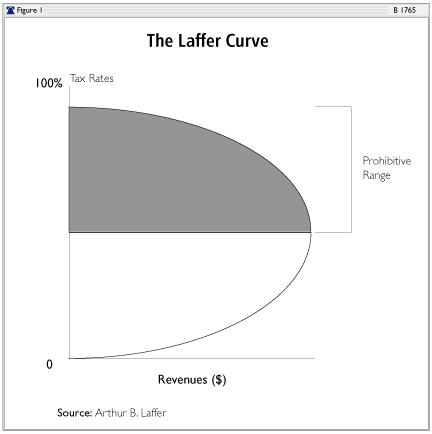

Figure 1 is a graphic illustration of the concept of the Laffer Curve--not the exact levels of taxation corresponding to specific levels of revenues. At a tax rate of 0 percent, the government would collect no tax revenues, no matter how large the tax base. Likewise, at a tax rate of 100 percent, the government would also collect no tax revenues because no one would willingly work for an after-tax wage of zero (i.e., there would be no tax base). Between these two extremes there are two tax rates that will collect the same amount of revenue: a high tax rate on a small tax base and a low tax rate on a large tax base.

The Laffer Curve itself does not say whether a tax cut will raise or lower revenues. Revenue responses to a tax rate change will depend upon the tax system in place, the time period being considered, the ease of movement into underground activities, the level of tax rates already in place, the prevalence of legal and accounting-driven tax loopholes, and the proclivities of the productive factors. If the existing tax rate is too high--in the "prohibitive range" shown above--then a tax-rate cut would result in increased tax revenues. The economic effect of the tax cut would outweigh the arithmetic effect of the tax cut.

Moving from total tax revenues to budgets, there is one expenditure effect in addition to the two effects that tax-rate changes have on revenues. Because tax cuts create an incentive to increase output, employment, and production, they also help balance the budget by reducing means-tested government expenditures. A faster-growing economy means lower unemployment and higher incomes, resulting in reduced unemployment benefits and other social welfare programs.

Over the past 100 years, there have been three major periods of tax-rate cuts in the U.S.: the Harding-Coolidge cuts of the mid-1920s; the Kennedy cuts of the mid-1960s; and the Reagan cuts of the early 1980s. Each of these periods of tax cuts was remarkably successful as measured by virtually any public policy metric.

Prior to discussing and measuring these three major periods of U.S. tax cuts, three critical points should be made regarding the size, timing, and location of tax cuts.

Size of Tax Cuts

People do not work, consume, or invest to pay taxes. They work and invest to earn after-tax income, and they consume to get the best buys after tax. Therefore, people are not concerned per se with taxes, but with after-tax results. Taxes and after-tax results are very similar, but have crucial differences.

Using the Kennedy tax cuts of the mid-1960s as our example, it is easy to show that identical percentage tax cuts, when and where tax rates are high, are far larger than when and where tax rates are low. When President John F. Kennedy took office in 1961, the highest federal marginal tax rate was 91 percent and the lowest was 20 percent. By earning $1.00 pretax, the highest-bracket income earner would receive $0.09 after tax (the incentive), while the lowest-bracket income earner would receive $0.80 after tax. These after-tax earnings were the relative after-tax incentives to earn the same amount ($1.00) pretax.

By 1965, after the Kennedy tax cuts were fully effective, the highest federal marginal tax rate had been lowered to 70 percent (a drop of 23 percent--or 21 percentage points on a base of 91 percent) and the lowest tax rate was dropped to 14 percent (30 percent lower). Thus, by earning $1.00 pretax, a person in the highest tax bracket would receive $0.30 after tax, or a 233 percent increase from the $0.09 after-tax earned when the tax rate was 91 percent. A person in the lowest tax bracket would receive $0.86 after tax or a 7.5 percent increase from the $0.80 earned when the tax rate was 20 percent.

Putting this all together, the increase in incentives in the highest tax bracket was a whopping 233 percent for a 23 percent cut in tax rates (a ten-to-one benefit/cost ratio) while the increase in incentives in the lowest tax bracket was a mere 7.5 percent for a 30 percent cut in rates--a one-to-four benefit/cost ratio. The lessons here are simple: The higher tax rates are, the greater will be the economic (supply-side) impact of a given percentage reduction in tax rates. Likewise, under a progressive tax structure, an equal across-the-board percentage reduction in tax rates should have its greatest impact in the highest tax bracket and its least impact in the lowest tax bracket.

Timing of Tax Cuts

The second, and equally important, concept of tax cuts concerns the timing of those cuts. In their quest to earn after-tax income, people can change not only how much they work, but when they work, when they invest, and when they spend. Lower expected tax rates in the future will reduce taxable economic activity in the present as people try to shift activity out of the relatively higher-taxed present into the relatively lower-taxed future. People tend not to shop at a store a week before that store has its well-advertised discount sale. Likewise, in the periods before legislated tax cuts take effect, people will defer income and then realize that income when tax rates have fallen to their fullest extent. It has always amazed me how tax cuts do not work until they actually take effect.

When assessing the impact of tax legislation, it is imperative to start the measurement of the tax-cut period after all the tax cuts have been put into effect. As will be obvious when we look at the three major tax-cut periods--and even more so when we look at capital gains tax cuts--timing is essential.

Location of Tax Cuts

As a final point, people can also choose where they earn their after-tax income, where they invest their money, and where they spend their money. Regional and country differences in various tax rates matter.

The Harding-Coolidge Tax Cuts

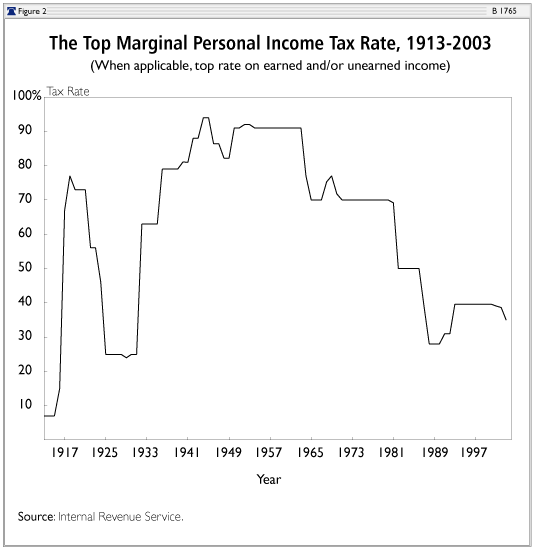

In 1913, the federal progressive income tax was put into place with a top marginal rate of 7 percent. Thanks in part to World War I, this tax rate was quickly increased significantly and peaked at 77 percent in 1918. Then, through a series of tax-rate reductions, the Harding-Coolidge tax cuts dropped the top personal marginal income tax rate to 25 percent in 1925. (See Figure 2.)

Although tax collection data for the National Income and Product Accounts (from the U.S. Bureau of Economic Analysis) do not exist for the 1920s, we do have total federal receipts from the U.S. budget tables. During the four years prior to 1925 (the year that the tax cut was fully implemented), inflation-adjusted revenues declined by an average of 9.2 percent per year (See Table 1). Over the four years following the tax-rate cuts, revenues remained volatile but averaged an inflation-adjusted gain of 0.1 percent per year. The economy responded strongly to the tax cuts, with output nearly doubling and unemployment falling sharply.

In the 1920s, tax rates on the highest-income brackets were reduced the most, which is exactly what economic theory suggests should be done to spur the economy.

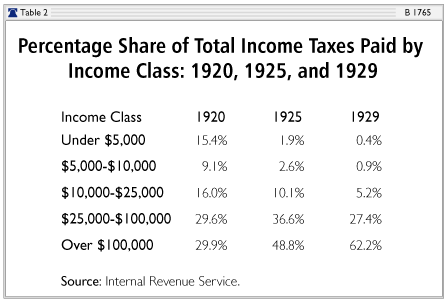

Furthermore, those income classes with lower tax rates were not left out in the cold: The Harding-Coolidge tax-rate cuts reduced effective tax rates on lower-income brackets. Internal Revenue Service data show that the dramatic tax cuts of the 1920s resulted in an increase in the share of total income taxes paid by those making more than $100,000 per year from 29.9 percent in 1920 to 62.2 percent in 1929 (See Table 2). This increase is particularly significant given that the 1920s was a decade of falling prices, and therefore a $100,000 threshold in 1929 corresponds to a higher real income threshold than $100,000 did in 1920. The consumer price index fell a combined 14.5 percent from 1920 to 1929. In this case, the effects of bracket creep that existed prior to the federal income tax brackets being indexed for inflation (in 1985) worked in the opposite direction.

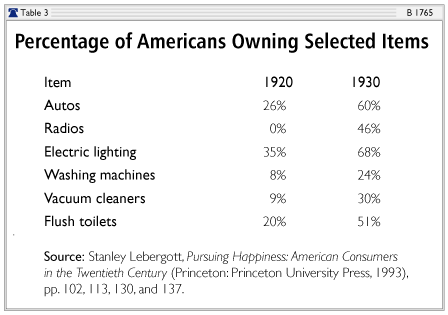

Perhaps most illustrative of the power of the Harding-Coolidge tax cuts was the increase in gross domestic product (GDP), the fall in unemployment, and the improvement in the average American's quality of life during this decade. Table 3 demonstrates the remarkable increase in American quality of life as reflected by the percentage of Americans owning items in 1930 that previously had only been owned by the wealthy (or by no one at all).

The Kennedy Tax Cuts

During the Depression and World War II, the top marginal income tax rate rose steadily, peaking at an incredible 94 percent in 1944 and 1945. The rate remained above 90 percent well into President John F. Kennedy's term. Kennedy's fiscal policy stance made it clear that he believed in pro-growth, supply-side tax measures:

Tax reduction thus sets off a process that can bring gains for everyone, gains won by marshalling resources that would otherwise stand idle--workers without jobs and farm and factory capacity without markets. Yet many taxpayers seemed prepared to deny the nation the fruits of tax reduction because they question the financial soundness of reducing taxes when the federal budget is already in deficit. Let me make clear why, in today's economy, fiscal prudence and responsibility call for tax reduction even if it temporarily enlarged the federal deficit--why reducing taxes is the best way open to us to increase revenues.3

Kennedy reiterated his beliefs in his Tax Message to Congress on January 24, 1963:

In short, this tax program will increase our wealth far more than it increases our public debt. The actual burden of that debt--as measured in relation to our total output--will decline. To continue to increase our debt as a result of inadequate earnings is a sign of weakness. But to borrow prudently in order to invest in a tax revision that will greatly increase our earning power can be a source of strength.

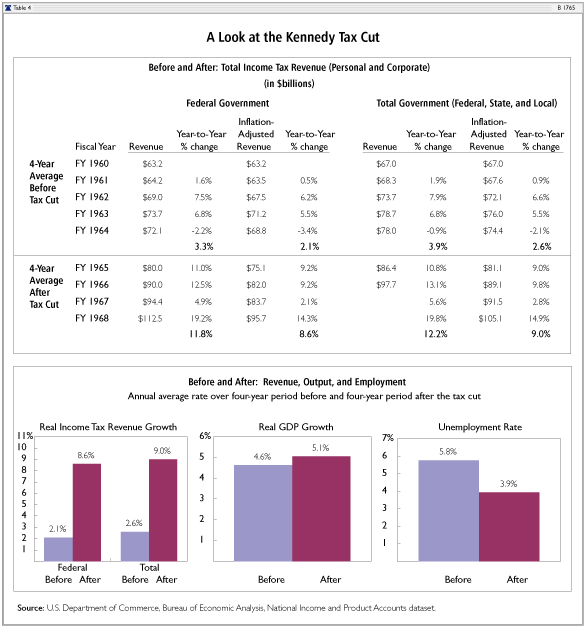

President Kennedy proposed massive tax-rate reductions, which were passed by Congress and became law after he was assassinated. The 1964 tax cut reduced the top marginal personal income tax rate from 91 percent to 70 percent by 1965. The cut reduced lower-bracket rates as well. In the four years prior to the 1965 tax-rate cuts, federal government income tax revenue--adjusted for inflation--increased at an average annual rate of 2.1 percent, while total government income tax revenue (federal plus state and local) increased by 2.6 percent per year (See Table 4). In the four years following the tax cut, federal government income tax revenue increased by 8.6 percent annually and total government income tax revenue increased by 9.0 percent annually. Government income tax revenue not only increased in the years following the tax cut, it increased at a much faster rate.

The Kennedy tax cut set the example that President Ronald Reagan would follow some 17 years later. By increasing incentives to work, produce, and invest, real GDP growth increased in the years following the tax cuts: More people worked, and the tax base expanded. Additionally, the expenditure side of the budget benefited as well because the unemployment rate was significantly reduced.

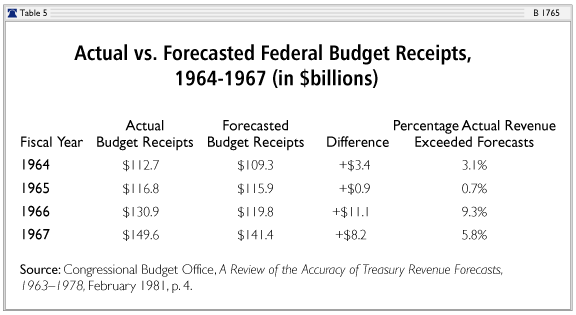

Using the Congressional Budget Office's revenue forecasts (made with the full knowledge of the future tax cuts), revenues came in much higher than had been anticipated, even after the "cost" of the tax cut had been taken into account (See Table 5).

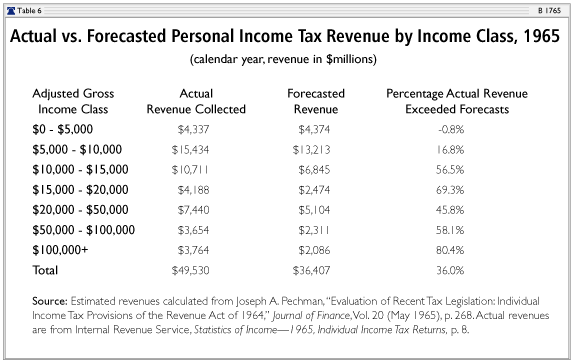

Additionally, in 1965--one year following the tax cut--personal income tax revenue data exceeded expectations by the greatest amounts in the highest income classes (See Table 6).

Testifying before Congress in 1977, Walter Heller, President Kennedy's Chairman of the Council of Economic Advisers, summarized:

What happened to the tax cut in 1965 is difficult to pin down, but insofar as we are able to isolate it, it did seem to have a tremendously stimulative effect, a multiplied effect on the economy. It was the major factor that led to our running a $3 billion surplus by the middle of 1965 before escalation in Vietnam struck us. It was a $12 billion tax cut, which would be about $33 or $34 billion in today's terms, and within one year the revenues into the Federal Treasury were already above what they had been before the tax cut.

Did the tax cut pay for itself in increased revenues? I think the evidence is very strong that it did.4

The Reagan Tax Cuts

In August 1981, President Reagan signed into law the Economic Recovery Tax Act (ERTA, also known as the Kemp-Roth Tax Cut). The ERTA slashed marginal earned income tax rates by 25 percent across the board over a three-year period. The highest marginal tax rate on unearned income dropped to 50 percent from 70 percent (as a result of the Broadhead Amendment), and the tax rate on capital gains also fell immediately from 28 percent to 20 percent. Five percentage points of the 25 percent cut went into effect on October 1, 1981. An additional 10 percentage points of the cut then went into effect on July 1, 1982. The final 10 percentage points of the cut began on July 1, 1983.

Looking at the cumulative effects of the ERTA in terms of tax (calendar) years, the tax cut reduced tax rates by 1.25 percent through the entirety of 1981, 10 percent through 1982, 20 percent through 1983, and the full 25 percent through 1984.

A provision of ERTA also ensured that tax brackets were indexed for inflation beginning in 1985.

To properly discern the effects of the tax-rate cuts on the economy, I use the starting date of January 1, 1983--when the bulk of the cuts were already in place. However, a case could be made for a starting date of January 1, 1984--when the full cut was in effect.

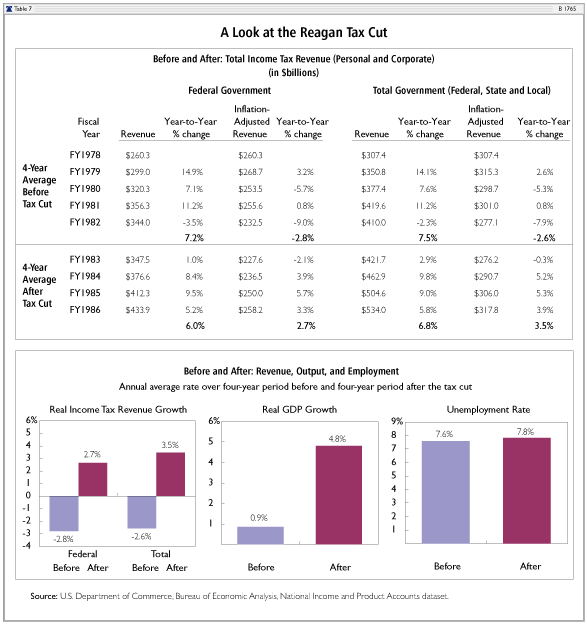

These across-the-board marginal tax-rate cuts resulted in higher incentives to work, produce, and invest, and the economy responded (See Table 7). Between 1978 and 1982, the economy grew at a 0.9 percent annual rate in real terms, but from 1983 to 1986 this annual growth rate increased to 4.8 percent.

Prior to the tax cut, the economy was choking on high inflation, high Interest rates, and high unemployment. All three of these economic bellwethers dropped sharply after the tax cuts. The unemployment rate, which peaked at 9.7 percent in 1982, began a steady decline, reaching 7.0 percent by 1986 and 5.3 percent when Reagan left office in January 1989.

Inflation-adjusted revenue growth dramatically improved. Over the four years prior to 1983, federal income tax revenue declined at an average rate of 2.8 percent per year, and total government income tax revenue declined at an annual rate of 2.6 percent. Between 1983 and 1986, federal income tax revenue increased by 2.7 percent annually, and total government income tax revenue increased by 3.5 percent annually.

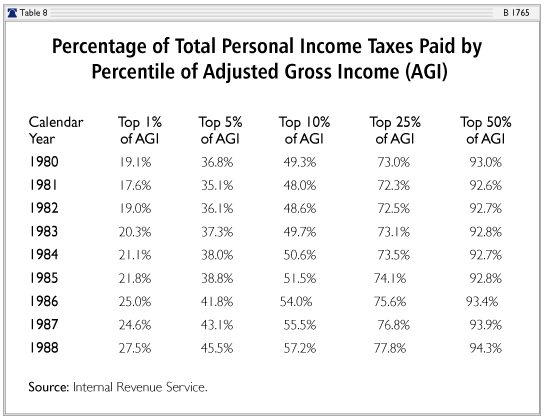

The most controversial portion of Reagan's tax revolution was reducing the highest marginal income tax rate from 70 percent (when he took office in 1981) to 28 percent in 1988. However, Internal Revenue Service data reveal that tax collections from the wealthy, as measured by personal income taxes paid by top percentile earners, increased between 1980 and 1988--despite significantly lower tax rates (See Table 8).

The Laffer Curve and the Capital Gains Tax

Changes in the capital gains maximum tax rate provide a unique opportunity to study the effects of taxation on taxpayer behavior. Taxation of capital gains is different from taxation of most other sources of income because people have more control over the timing of the realization of capital gains (i.e., when the gains are actually taxed).

The historical data on changes in the capital gains tax rate show an incredibly consistent pattern. Just after a capital gains tax-rate cut, there is a surge in revenues: Just after a capital gains tax-rate increase, revenues take a dive. As would also be expected, just before a capital gains tax-rate cut there is a sharp decline in revenues: Just before a tax-rate increase there is an increase in revenues. Timing really does matter.

This all makes total sense. If an investor could choose when to realize capital gains for tax purposes, the investor would clearly realize capital gains before tax rates are raised. No one wants to pay higher taxes.

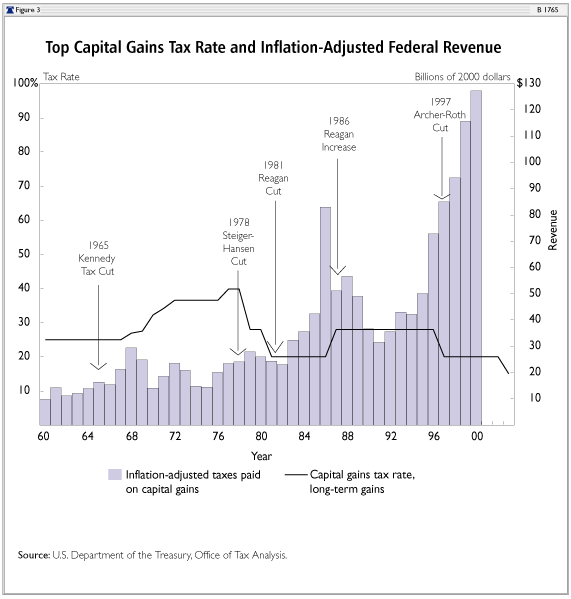

In the 1960s and 1970s, capital gains tax receipts averaged around 0.4 percent of GDP, with a nice surge in the mid-1960s following President Kennedy's tax cuts and another surge in 1978-1979 after the Steiger-Hansen capital gains tax-cut legislation went into effect (See Figure 3).

Following the 1981 capital gains cut from 28 percent to 20 percent, capital gains revenues leapt from $12.5 billion in 1980 to $18.7 billion by 1983--a 50 percent increase--and rose to approximately 0.6 percent of GDP. Reducing income and capital gains tax rates in 1981 helped to launch what we now appreciate as the greatest and longest period of wealth creation in world history. In 1981, the stock market bottomed out at about 1,000--compared to nearly 10,000 today (See Figure 4).

As expected, increasing the capital gains tax rate from 20 percent to 28 percent in 1986 led to a surge in revenues prior to the increase ($328 billion in 1986) and a collapse in revenues after the increase took effect ($112 billion in 1991).

Reducing the capital gains tax rate from 28 percent back to 20 percent in 1997 was an unqualified success, and every claim made by the critics was wrong. The tax cut, which went into effect in May 1997, increased asset values and contributed to the largest gain in productivity and private sector capital investment in a decade. It did not lose revenue for the federal Treasury.

In 1996, the year before the tax rate cut and the last year with the 28 percent rate, total taxes paid on assets sold was $66.4 billion (Table 9). A year later, tax receipts jumped to $79.3 billion, and in 1998, they jumped again to $89.1 billion. The capital gains tax-rate reduction played a big part in the 91 percent increase in tax receipts collected from capital gains between 1996 and 2000--a percentage far greater than even the most ardent supply-siders expected.

Seldom in economics does real life conform so conveniently to theory as this capital gains example does to the Laffer Curve. Lower tax rates change people's economic behavior and stimulate economic growth, which can create more--not less--tax revenues.

The Story in the States

California

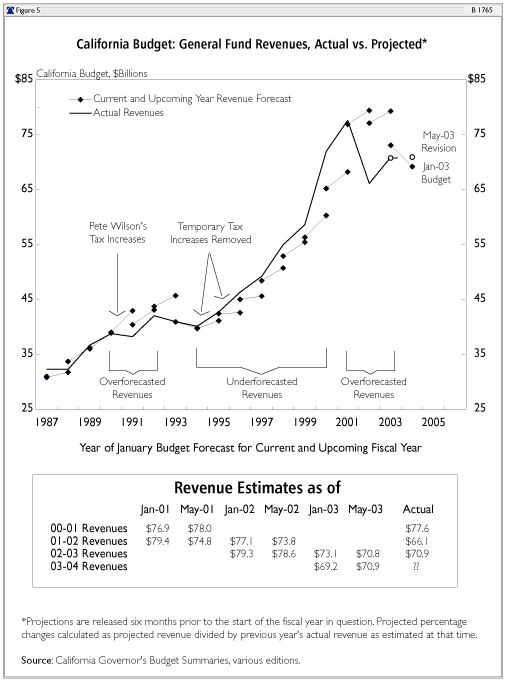

My home state of California has an extremely progressive tax structure, which lends itself to Laffer Curve types of analyses.5 During periods of tax increases and economic slowdowns, the state's budget office almost always overestimates revenues because they fail to consider the economic feedback effects incorporated in the Laffer Curve analysis (the economic effect). Likewise, the state's budget office also underestimates revenues by wide margins during periods of tax cuts and economic expansion. The consistency and size of the misestimates are quite striking. Figure 5 demonstrates this effect by showing current-year and budget-year revenue forecasts taken from each year's January budget proposal and compared to actual revenues collected.

State Fiscal Crises of 2002-2003

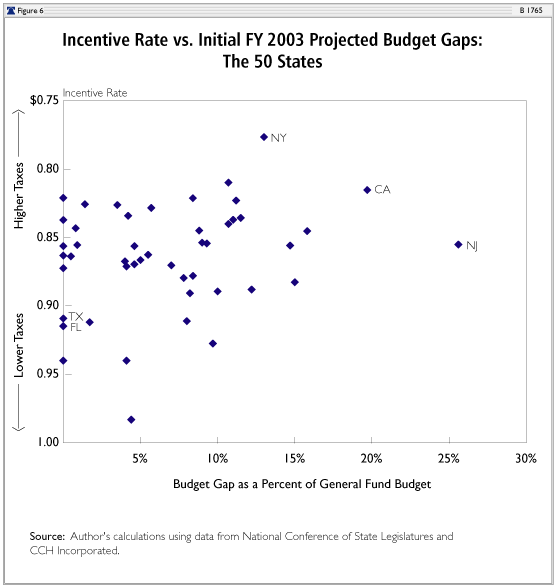

The National Conference of State Legislatures (NCSL) conducts surveys of state fiscal conditions by contacting legislative fiscal directors from each state on a fairly regular basis. It is revealing to look at the NCSL survey of November 2002, at about the time when state fiscal conditions were hitting rock bottom. In the survey, each state's fiscal director reported his or her state's projected budget gap--the deficit between projected revenues and projected expenditures for the coming year, which is used when hashing out a state's fiscal year (FY) 2003 budget. As of November 2002, 40 states reported that they faced a projected budget deficit, and eight states reported that they did not. Two states (Indiana and Kentucky) did not respond.

Figure 6 plots each state's budget gap (as a share of the state's general fund budget) versus a measure of the degree of taxation faced by taxpayers in each state (the "incentive rate"). This incentive rate is the value of one dollar of income after passing through the major state and local taxes. This measure takes into account the state's highest tax rates on corporate income, personal income, and sales.6 (These three taxes account for 73 percent of total state tax collections.)7

These data have all sorts of limitations. Each state has a unique budgeting process, and no one knows what assumptions were made when projecting revenues and expenditures. As California has repeatedly shown, budget projections change with the political tides and are often worth less than the paper on which they are printed. In addition, some states may have taken significant budget steps (such as cutting spending) prior to FY 2003 and eliminated problems for FY 2003. Furthermore, each state has a unique reliance on various taxes, and the incentive rate does not factor in property taxes and a myriad of minor taxes.

Even with these limitations, FY 2003 was a unique period in state history, given the degree that the states--almost without exception--experienced budget difficulties. Thus, it provides a good opportunity for comparison. In Figure 6, states with high rates of taxation tended to have greater problems than states with lower tax rates. California, New Jersey, and New York--three large states with relatively high tax rates--were among those states with the largest budget gaps. In contrast, Florida and Texas--two large states with no personal income tax at all--somehow found themselves with relatively few fiscal problems when preparing their budgets.

Impact of Taxes on State Performance Over Time

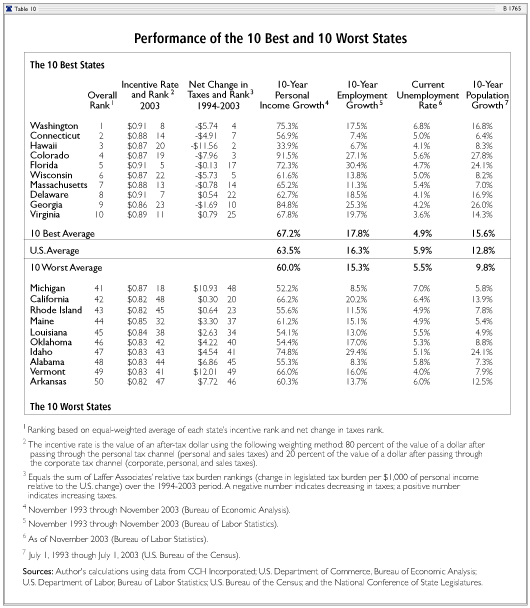

Over the years, Laffer Associates has chronicled the relationship between tax rates and economic performance at the state level. This relationship is more fully explored in our research covering the Laffer Associates State Competitive Environment model.8 Table 10 demonstrates this relationship and reflects the importance of taxation--both the level of tax rates and changes in relative competitiveness due to changes in tax rates--on economic perforance.

Combining each state's current incentive rate (the value of a dollar after passing through a state's major taxes) with the sum of each state's net legislated tax changes over the past 10 years (taken from our historical State Competitive Environment rankings) allows a composite ranking of which states have the best combination of low and/or falling taxes and which have the worst combination of high and/or rising taxes. Those states with the best combination made the top 10 of our rankings (1 = best), while those with the worst combination made the bottom 10 (50 = worst). Table 10 shows how the "10 Best States" and the "10 Worst States" have fared over the past 10 years in terms of income growth, employment growth, unemployment, and population growth. The 10 best states have outperformed the bottom 10 states in each category examined.

Looking Globally

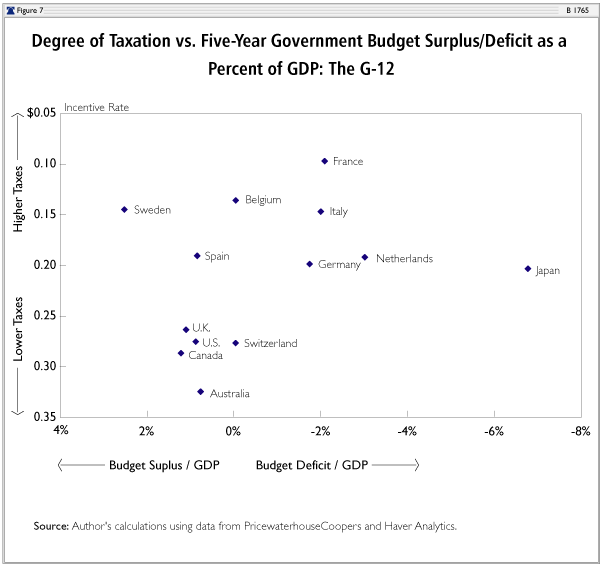

For all the brouhaha surrounding the Maastricht Treaty, budget deficits, and the like, it is revealing--to say the least--that G-12 countries with the highest tax rates have as many, if not more, fiscal problems (deficits) than the countries with lower tax rates (See Figure 7). While not shown here, examples such as Ireland (where tax rates were dramatically lowered and yet the budget moved into huge surplus) are fairly commonplace. Also not shown here, yet probably true, is that countries with the highest tax rates probably also have the highest unemployment rates. High tax rates certainly do not guarantee fiscal solvency.

Tax Trends in Other Countries: The Flat-Tax Fever

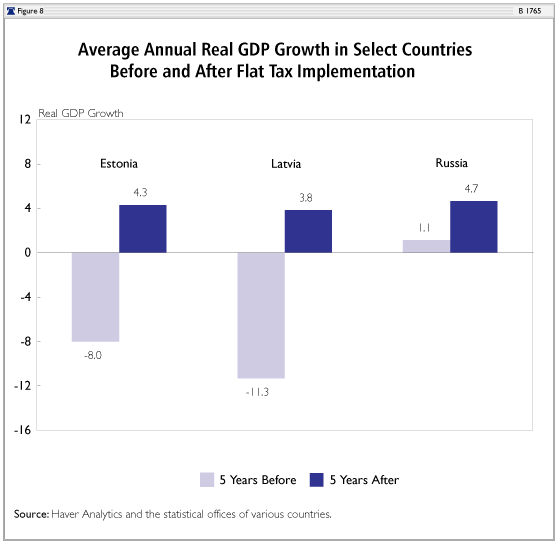

For many years, I have lobbied for implementing a flat tax, not only in California, but also for the entire U.S. Hong Kong adopted a flat tax ages ago and has performed like gangbusters ever since. Seeing a flat-tax fever seemingly infect Europe in recent years is truly exciting. In 1994, Estonia became the first European country to adopt a flat tax, and its 26 percent flat tax dramatically energized what had been a faltering economy. Before adopting the flat tax, Estonia had an impoverished economy that was literally shrinking--making the gains following the flat tax implementation even more impressive. In the eight years after 1994, Estonia sustained real economic growth averaging 5.2 percent per year.

Latvia followed Estonia's lead one year later with a 25 percent flat tax. In the five years before adopting the flat tax, Latvia's real GDP had shrunk by more than 50 percent. In the five years after adopting the flat tax, Latvia's real GDP has grown at an average annual rate of 3.8 percent (See Figure 8). Lithuania has followed with a 33 percent flat tax and has experienced similar positive results.

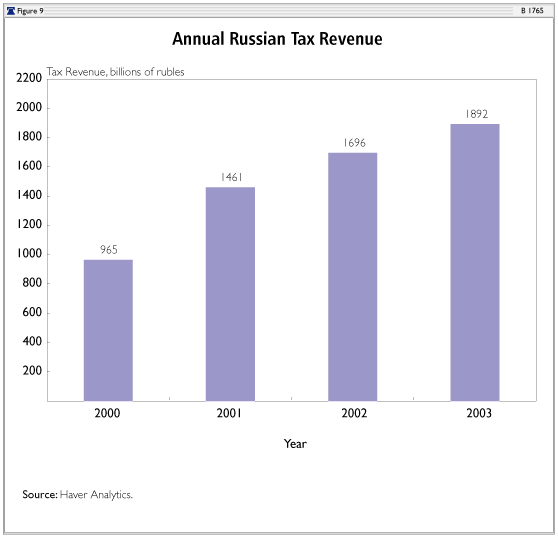

Russia has become one of the latest Eastern Bloc countries to institute a flat tax. Since the advent of the 13 percent flat personal tax (on January 1, 2001) and the 24 percent corporate tax (on January 1, 2002), the Russian economy has had amazing results. Tax revenue in Russia has increased dramatically (See Figure 9). The new Russian system is simple, fair, and much more rational and effective than what they previously used. An individual whose income is from wages only does not have to file an annual return. The employer deducts the tax from the employee's paycheck and transfers it to the Tax Authority every month.

Due largely to Russia's and other Eastern European countries' successes with flat tax reform, Ukraine and the Slovak Republic implemented their own 13 percent and 19 percent flat taxes, respectively, on January 1, 2004.

Arthur B. Laffer is the founder and chairman of Laffer Associates, an economic research and consulting firm. This paper was written and originally published by Laffer Associates. The author thanks Bruce Bartlett, whose paper "The Impact of Federal Tax Cuts on Growth" provided inspiration.

{kind=link}

{kind=link}

;){kind=link}

;){kind=link}

;){kind=link}

;){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

;){kind=link}

;){kind=link}

;){kind=link}

;){kind=link}

;){kind=link}

;){kind=link}

;){kind=link}