(Archived document, may contain errors)

c 878 Revistd: November 9,1992 CONSUMER CHOICE IN HEALTH: LEARNING FROM THE FEDERAL EMPLOYEE HEALTH BE" PROGRAM

INTRODUCTION

In the debate over national health care reform, there is good news and bad news.

The good news is that Congress actually has discovered the answer to America's health care problem, and the answer is a system that already exists.This system gives consumers wide choice of health plans and "user friendly" advice on how to choose among rival plans.It promotes intense competition among health insurance carriers. Is controls costs. It incorporates excellent benefits. And those who are enrolled in it are pleased with the system.

The bad news is that Congress has been keeping this system exclusively for itself and federal workers while considering ways to impose vastly inferior systems on almost all other Americans.What would be fair is for Congress to allow all Americans to have a version of what lawmakers and federal workers reserve for themselves.

Anxious Workers. Surveys show that most Americans arc anxious about their job-related health benefits. Many workers worry that if they. an laid off, they will lose their cur rent health benefits and may not qualify for coverage at a new job because of their medical condition. Others have no coverage at all, because their company does not offer it, and these workers must try to pay for their own care or insurance without any help from the government.

Problems like these do not worry the President, members of Congress, cabinet secretaries, congressional staff, and the millions of federal employees, retirees, and dependents who enjoy a system known as the Federal Employee Health Benefits Program (FEHBP). As President George Bush has stated: "The FEHBP system currently allows federal employees to choose from a variety of competitive health plan options to obtain the best coverage for the best price."[REF] The bad news is that Congress has been keeping this system exclusively in itself and fed

(This is a revised and updated version of a study published on February 6.1992.)

Consumer Choice Showcase. Like any government program, the FEHBP is far from perfect. Yet it is an excellent showcase of how consumer choice works in health care, and how I system for all Americans based on choice, such as the plan proposed by The Heritage Foundation, would work in practice.[REF]

Under the FEHBP, some nine million Americans of widely differing income levels and backgrounds, from blue collar messengers on Capitol Hill to the President and each member of the President's cabinet, each year can pick and choose from a wide range of health care plans. From November 9 until December 14 this year, a period known as "open-season," these Americans will be able to choose the plan they want for 1993. Unlike most Americans these congressional and federal employees, as well as retired federal workers enjoy the unique opportunity to decide what combination of services and price is best for themselves and their families.

Throughout the United States, these fortunate Americans can choose among almost 400 health care plans, typically with two dozen choices available in any particular city or county. These range from traditional insurance plans, like Blue Cross and Blue Shield, to over 350 Health Maintenance Organizations (HMOs), including such giants as Kaiser Permanente, to union-sponsored health care plans, such as those offered by the huge American Postal Workers Union or the smaller National Association of Letter Carriers.

This system base d on consumer choice and competing providers works smoothly and is popular with lawmakers and civil servants alike. This is why few ordinary Americans ever hear their senator or congressman complain about his health benefits.

Among the key features of the FEHBP:

The FEHBP makes it easy for consumers to choose

Every fall, federal employees receive a simple form listing the plans available in their area. They check off the plan they want. They cannot be wed down by the plan or be required to pay a higher premium. Consumer organizations and the local press give employees the information they need to make informed decisions.

The FEHBP gives help to pay for coverage.

In making a selection, the employee is quoted a premium price. However, the federal government makes a contribution to the plan, according to a formula and with a maximum dollar limit.

The FEHBP makes it easy for the employee.

The employees agency, or congressional of f ice, automatically deducts the employees share of the premium from each paycheck and sends it to a central government fund A check then is cut by the government for all the employees in a particular plan and Sent to that plan.

The FEHBP encourages health plans sponsored by unions and other employee organizations.

Such plans accounted in 1992 for 32 percent of all enrollees. These plans also are avail able for non-union members. Example: only 5.6 percent of the enrollees in the Mail Handlers Plan are members of the union. By extending their plan to non-union members, the unions can earn a profit. In 1988, for instance, the Mail Handlers Plan made a $14 million profit or $280 for every union member. Some employee organizations, such as the Government Employees Health Association, exist solely for the purpose of sponsoring a plan for themselves.

The FEHBP promotes managed care.

Managed care plans known as Health Maintenance Organizations (HMOs), which are low-cost plans in which families accept certain limits on their choice of doctor and hospital but normally receive no bills for any treatment, accounted for 28 percent of all FEHBP enrollees in 1991. In America as a whole, only 15 percent of Americans are enrolled in HMOs.

The FEHBP rules are simple.

In a refreshing contrast to most large government programs, the FEHBP is relatively free of red tape. The law governing the FEHBP is only 24 pages long, with 54 pages of regulations and 93 pages of instructions. By contrast, the law covering Medicare is 319 pages long, with 1,104 pages of regulations, plus a continually expanding body of instructions and guidelines numbering many .thousands of pages confusing to doctors and patients alike.

The FEHBP keeps costs down.

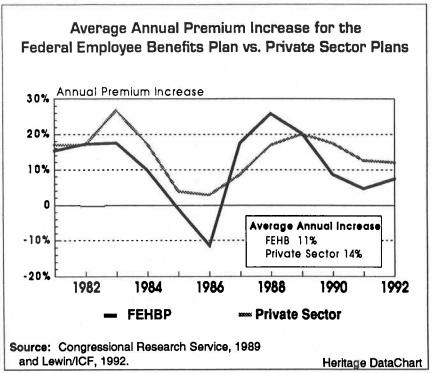

According to the United States Office of Personnel Management (OPM), the federal agency which runs the FEHBP, "The average 1993 premium paid by active non-postal employees and annuitants will increase by only 9 percent, the third consecutive year the in crease has been under 10 percent. This increase is less than half the 20 percent trend seen in the health insurance industry."[REF] In 1992, the average premium increase in the FEHBP was 7.4 percent; in 1991,4.7 percent. By contrast, premium increases in plans sponsored by U.S. corporations increased 12.5 percent in 1991 and 12 percent in 1992. During the 1980s, the FEHBP also generally outperformed private sector plans in holding down health care costs, based on data supplied by the Congressional Research Service, the chief re search agency of Congress, and Lewin/ICF, a leading econometric firm whose services are used by Congress, government agencies, and major corporations. This performance is all the more remarkable because the FEHBP covers a growing number of retirees, including retirees without Medicare, whose health care costs have been rising much faster than for younger Americans. Typical plans offered by private firms do not.

What is the secret of FEHBP? It promotes consumer choice and a competitive insurance market. The law governing private sector workers, by contrast does not.

The tax code affecting the private sector gives tax relief normally only to a plan offered by a company to its employees. If the employee would prefer another, more economical plan, he or she receives no tax break and thus has no incentive to switch to it. Yet congress men and other government workers receive the same financial assistance whichever of doz ens of plans they choose. This gives them incentive to seek good values for money.

To make matters worse, giving tax relief only for "employer-paid" plans, which in fact becomes part of the workers compensation package, creates the illusion among many workers that their health care is free and thus encourages health cost inflation. Federal workers choose plans according to price and quality, and so have strong incentives to economize.

Skeptics Proved Wrong. Skeptics of the idea of a consumer-choice universal health system in America often claim that Americans are not capable of choosing their own health coverage. A New York Times editorial complains that consumer-choice plans "rely on individuals to buy their own coverage. But the complexity of insurance plans makes comparison shopping virtually impossible by anyone other than an experienced professional."[REF] The FEHBP system, through over three decades of operation, proves this view to be dead wrong. If low-skilled congressional messengers can choose their plan, so can other Americans.

Congressmen like their system so much that they often insist that they be exempted from any new health system that they would impose on other Americans.[REF] This is especially true of bills in Congress mandating that private employers either prod& health insurance for their workers or pay an additional payroll tax to finance a new public insurance program. Faced with this "play or pay" option, many companies likely would pay the new payroll tax and millions of Americans would thus be involuntarily separated from their private insurance and dumped into a huge Medicaid-like program. But not members of Congress or their staffs. For example, one of the leading "play or pay" reform bills in the Senate (S. 1227), sponsored by Majority Leader George Mitchell, the Maine Democrat, like many other health bills explicitly exempts lawmakers and other federal workers from coverage, and thus the consequences, of the bill. Rather than keeping their excellent health care system a special privilege for themselves and other federal workers, lawmakers should allow other Americans in effect to join the system. What is good enough for Congress should be good enough for the American people. cans

To open an FEHBP-like system to the uninsured and other working-age Americans, Congress needs to take two basic steps:

First, Congress needs to change the tax treatment of medical benefits to allow tax breaks to Americans wherever they obtain health coverage. This would enable Americans to choose a plan offered by their union, or a managed care plan, or a "high option" insurance plan, wherever they work -- a range of choices taken for granted by federal employees and retirees but unavailable to private sector workers.

Second, Congress needs to require working-age Americans not covered by Medicare or Medicaid to purchase at least a basic health plan, and to provide assistance to families who otherwise would be unable to afford cm.

The Heritage Foundation's proposed Consumer Choice Health Plan would accomplish this. Under the Heritage plan, the current tax exclusion for company-based plans would be replaced with a refundable tax credit for a health plan obtained from any licensed source and for out-of-pocket medical expenses. In addition, all heads of households would be required to obtain at least a basic plan. This would give ordinary Americans the same kind of options for health coverage as congressmen and federal workers now enjoy.

The Heritage Foundation Consumer Choice Health Plan is embodied in "The Health Care Access and Affordability Act of 1992 " (S. 3348), sponsored by Senator Orrin Hatch, the Utah Republican, and cosponsored by Senator Malcolm Wallop, the Wyoming Republican, Senator Robert Smith, the New Hampshire Republican, and Senators Ted Stevens and Frank Murkowski both Alaska Republicans.

Lawmakers assume that the U.S. health system needs major surgery, and Congress now is debating the nature of the required operation. What the patient really needs is a strong dose of consumer choice and competition. Congressmen know this from their personal experience with their own health system based on these powerful dynamics The way to solve the national health care problem is for Congress to let all Americans have a similar system

HOW THE FEHBP WORKS

Created in 1959, the Federal Employees Health Benefit Plan is open to all members of Congress and congressional staff, the President, cabinet members, other executive branch appointees, federal judges, judicial staff, and all federal civil service employees and postal service workers. In addition, federal retirees, survivors of deceased federal employees and retirees, and the dependents of active federal employees and retirees are covered. Employees of the District of Columbia also are eligible. Approximately nine million individuals are in the nationwide system. The decision to enroll is up to the employee, and about 85 percent of the active federal workforce is in the program.[REF] The majority of those not covered by the FEHBP are covered by the plan of a working spouse not in the federal workforce.

In a four-week period each fall known as "open season," federal workers can choose which health care plan will cover them. They can choose any private plan in the system. Most do not change their plan from year to year, but if the worker decides to change plans he or she has the right to enroll at the same premium as any other plan enrollee, without regard to health condition.

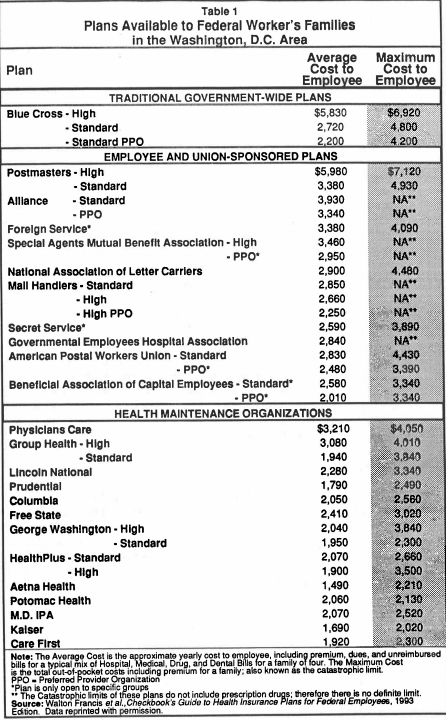

The choice available to federal workers is far wider than for employees of even the largest private corporations. According to economist Walton Francis, author of Checkbooks Guide to Health Insurance Plans for Federal Employees, a comprehensive guide to plans published by a Washington, D.C.-based consumer organization, federal workers across the country can choose among almost 400 plans. In the Washington, D.C area, federal workers can choose from 36 different plans.[REF]

The range of plans offered to federal workers is remarkable, as is the range of organizations sponsoring the plans. There are traditional "fee-for-service" insurance plans, offered by such major insurers as Blue Cross and Blue Shield. But the FEHBP law also authorizes employee organizations, like unions, to offer plans.

Union Plans. Union-sponsored plans started to compete successfully with the traditional big insurance companies in the 1970s. Today, seventeen employee-sponsored plans are available to federal workers, including union plans, and several of these plans are available to those who are not regular members of the union. In the latter case, the union or employee organization normally requires outside enrollees to pay modest "associate membership" fees, normally between $30 and $35 per year.[REF]

The marketing success of these employee organizations has been phenomenal; by 1990 they included almost 36 percent of all FEHBP enrollees. A good example is the Mail Handlers union. According to a 1988 study conducted for the Office of Personnel Management:

The Mail Handlers Benefit Plan has been so successful that the plan now dwarfs the union that sponsors it. There are approximately 30,000 regular members of the union in the health plan and nearly 500,000 enrollees. With associate membership dues of $30 per year, the plan generates approximately $14 million in revenue for the union, or $280 for every regular dues paying member. A representative of the Mail Handlers Plan advised us during an interview that most of the plans enrollees are not postal workers; thy are civilian employees in various agencies of the Executive Branch.[REF]

Another example of a successful employee organization plan is the Government Employees Hospital Association (GEHA). This plan was developed by a group of federal employees not associated directly with any union. In fact, according to a study for OPM, "This organization's sole purpose appears to be the offering of a health insurance plan under FEHBP.[REF] And the organization itself simply is the group of employees who have chosen the plan.

Managed Care. Another type of plan growing rapidly among federal employees is managed care. In managed care plans, enrollees accept certain restrictions on their choice of physicians and hospitals in return for lower premiums. The best known from of managed care plan is a Health Maintenance Organization or HMO. The patient in an HMO normally receives no bills for treatment. He or she simply pays a fixed monthly fee for all care.

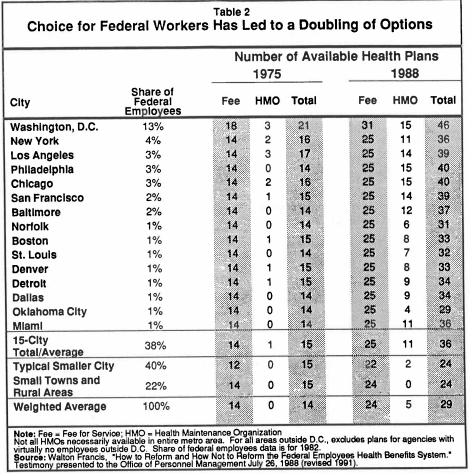

Table 2 shows the growth in the range of options available nationally to federal workers during the 1970s and 1980s. Per enrollee, the number of choices doubled from roughly a dozen to two dozen plans. Since 1988, the average number available per enrollee has declined to less than two dozen. The growth in HMO options has been dramatic.

While HMOs in the private sector have been growing fast, they are doing so faster in the FEHBP.[REF] One reason for this is that in the private sector, where employees often used to generous "free" plans "paid for" by their employers, employees resist being assigned to more restrictive plans, even though they generally cost less (to the employer, that is). In the FEHBP system, by contrast, employees can shop around among plans according to their combination of price and quality and keep the premium savings from lower-cost plans. In this open market, the price advantage of HMOs proves very attractive.

How the Government Helps to Pay Premiums

The same is true for most While the employee makes a decision on the basis of the stated premium price and benefits package, the government makes a contribution to the cost. The same is true for most workers in the private sector, because company-provided health plans are a tax-free fringe benefit -- although if a family has no company plan and buys insurance directly, there is usually no tax break. In the federal sector, the help takes the form not of a tax break, but a direct payment calculated according to what is called the "Big Six" formula.

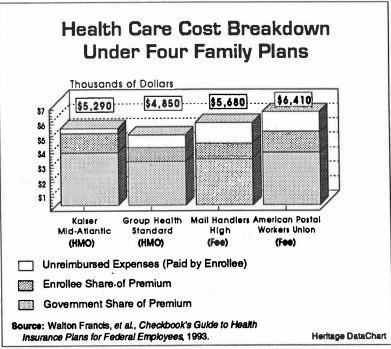

Under this formula, the government will contribute an amount equal to 60 percent of the "simple average" of the premiums for individual and family coverage of the six largest plans in the program. This means the federal government contributes a fixed dollar amount. The law further specifies that the contribution cannot exceed 75 per cent of the premium, up to the formula dollar amount.[REF] For next year, the maximum is $1,675 for single employees and $3,630 for families. Federal employees and retirees then pay the difference between the contribution and the premium cost. The above chart shows a breakdown of costs to employees and the government in four typical plans.

The federal employee does not even have to write a check to his or her insurance company or request reimbursement from the government for its share. Instead, the agency makes a payroll deduction each pay period for the employees share of the premium adds its own contribution, and transmits this money to an FEHBP Trust Fund, which then pays the plan chosen by the employee. For retired federal personnel, payments are made by the Office of Personnel Management from a special account.

The Benefits Available to Federal Workers

The FEHBP law gives the Office of Personnel Management, the federal governments central personnel agency, flexibility to negotiate rates and benefits of plans, consistent with Congress's intent to provide a sound package of benefits at reasonable cost. Congress has on occasion, recommended that OPM press for certain specific benefits, but generally has stopped short of mandating them. OPM, which is responsible for the program, can require certain items to be included in all plans offered during open season.

This is quite different from the pattern at the state level, where state legislatures rarely have hesitated to enact sweeping mandates requiring insurers to include certain services in any plan they offer in the state.[REF] Why this difference between the states and the federal government in their propensity to mandate benefits? When a state mandates a benefit, companies foot the bill, and employees applaud state lawmakers for increasing their "free" employer-provided benefits. By contrast, if Congress mandates a benefit in all plans, there is no free lunch, and the taxpayers and federal employees pay more.

This does not mean that federal plans offer only "bare bones" coverage. In fact, federal workers often demand, and receive, the reasonably generous benefits they choose to pay for. But they can also choose plans that will save them money. Notes Mike Causey, the Washington Posts veteran reporter on civil service affairs: "All of the health plans are good, but picking the best one can save individuals $1,000 or more in premiums and out-of pocket costs next year."[REF] Virtually all the competing federal plans offer a wide range of services, including hospital and physician services, tests, immunizations and preventive examinations, kidney dialysis, and a limit on total out-of pocket costs.

HELPING CONSUMERS CHOOSE

Some critics of consumer choice in health care claim that a big difference between medical purchases and, say, buying a car, is that easily digestible information for consumers regarding health care does not exist. This, they say, makes informed choices impossible.

To be sure, there is little information to help private sector employees buy health plans. But this is because few families have the chance to make a choice from a wide range of plans. Without a market for advice, products offering advice will not develop. Such products, of course, have been developed offering advice for how to purchase other sophisticated or complicated goods and services like life insurance, real estate, automobiles, or stocks and bonds.

Similarly there is plenty of advice for the nine-million-strong consumer market for FEHBP health plans. So me comes from the federal government. The Office of Personnel Management sends each employee an unbiased description of the benefits and employee cost of each plan. Federal agencies add to this information by distributing material to employees and sponsoring health fairs that outline what is available to employees and their families. Members of Congress with large concentrations of federal employees or retirees in their districts even hold weekend health fairs, inviting private health insurance and government analysts to discuss the merits and drawbacks of the various FEHBP plans.

The Private Sector Information Explosion

Official efforts pale by comparison to the sophisticated and ubiquitous private information available to federal employees and the public discussion that takes place each open sea son. For instance, from daily columns in the Washington Post to programs on talk radio, federal employees in the Washington, D.C., area can obtain the latest information on each years health care offerings -- how much plans are going to cost, which has the best dental benefits, which has the best catastrophic coverage, and so on. In addition, the companies and employee organizations market their plans through brochures and advertising, especially in areas where there are heavy concentrations of federal employees. Carriers take to the airwaves, post billboards in strategic locations, or advertise in newspapers, buses, and subways. And they respond to the demand for quality information in plain English, with minimal jargon.

Even more significant is that major consumer organizations provide the same kind of information to federal workers buying heath plans as they do for other Americans purchasing a new car. Each year in the Washington, D.C., area, for example, congressional and federal employees can purchase the Checkbook's Guide to Health Insurance Plans for Federal Employees, with detailed ratings and cost analyses of all the health insurance options available. This annually makes the best seller book list in Washington, and is published by Washington Consumers Checkbook, the same consumer organization that publishes information on where Washingtonians can get the best bargains on everything from VCRs to autos to household appliances.

Federal employee organizations, meanwhile, distribute information to their members. The National Association of Retired Federal Employees (NARFE), for instance, publishes an annual "Open Season Guide." And, of course, federal employees do in health care what they and other Americans do when they make other major purchases: they talk to experts they trust and they talk to their coworkers. They ask their family physicians their agency benefits expert about rival health plans, and they talk to each other about their experiences with plans.

During open season, the cafeterias of the Treasury, the shuttlebuses to the State Department, and the subways to the suburbs are scenes of countless discussions and debates about the pros and cons of different health plans. It happens because federal employees have the right to choose and the incentive to choose wisely.

Refuting Experts. The wide availability of understandable information and expert advisors refutes the contention that only experts can make intelligent decisions about health plans 11 care insurance. And even though some federal employees, like consumers in other markets actually grumble that the wide range of annual options is annoying or confusing, very few would want OPM to end open season. In fact, serious proposals to postpone open season have met with implacable employee opposition.[REF]

Employees use the information available to them to change plans when they find it advantageous and to save money. One effect has been a steady move to lower cost options such as managed care plans, including HMOs. In 1987, for example, approximately 175,000 enrollees moved from fee-for-service plans to HMO plans, with costs that were approximately 20 percent less than comparable fee-for-service plans.[REF] As economist Walton Francis notes, with average enrollee premiums in 1988 dollars (both employee and government share) running about $2,430 for fee-for-service plans, and about $2,100 for HMOs, the $330 in savings per enrollee, for HMO enrollment alone generated "savings for both the employees and the taxpayers on the order of $50 million in 1987."[REF] Says Francis, "Those non-expert federal employees who supposedly cannot choose rationally among a large number of plans have succeeded in becoming well enough informed to better their own health insurance while saving both themselves and the government hundreds of millions of dollars annually."[REF]

THE LACK OF RED TAPE IN THE FEHBP SYSTEM

Compared to most government programs, which are accompanied by thousands of pages of detailed and confusing regulation, there is little red tape in the FEHBP. Just 1 percent of each plans' premium cost is set aside for OPMs administration of the system.This covers such things as OPMs role in running the annual "open season" and operating the Federal Employees Health Benefits Trust Fund, out of which premiums are paid to the carriers, as well as administering a wide range of services for retirees. OPM also requires plans to put aside three percent of premiums income in a reserve to pay for "current and future claims liabilities" and to strengthen the financial position of the program.

Compared with the giant Medicare program, which is the prototype for the government payer system for national health insurance advocated by some in Congress, the consumer driven FEHBP is administratively far simpler despite the existence of an enormous number of plans.

Cumbersome Medicare. In Medicare, the government literally dictates what benefits will or will not be included, such as catastrophic coverage, through a cumbersome and often controversial legislative and regulatory process. In contrast, the addition of benefits in the FEHBP is relatively painless, effected through private sector-style negotiations, and finalized for each and every employee through personal choice. While Congress and the managers of Medicare program devote enormous resources to implementing intrusive and complex "cost control" features, the managers of the FEHBP historically have refiained froin such intervention. Nevertheless, truly efficient market forces, such as employees voluntary choice of low-cost plans with higher coinsurance and deductibles, makes this unique federal program a leader in health cm cost control. While Medicare employs thousands of personnel to administer the program, including the negotiation and monitoring of carrier con tracts, the promulgation of thousands of pages of detailed guidelines, rules and regulations the FEHBP plans themselves do much of the actual administration, including claims processing, and the governments administrative staff is small. Meanwhile, OPM has helped to keep overhead costs down by making some significant managerial improvements during the past two years.[REF]

COST CONTROL IN THE FEHBP

Like ordinary Americans, most lawmakers recognize that the best mechanism to control costs without sacrificing economic efficiency is through consumer choice in a competitive market. But there has been an assumption that this mechanism cannot operate in health care because consumers and providers are not greatly influenced by differences in prices in making choices. In Medicare, Medicaid, and even many private company plans, this has led to the price controls, regulation, and other features of central planning. But these have proven no mm effective in achieving efficiency in the U.S. health cm system than in the communist economies of Eastern Europe.

FEHBP explodes the myth that consumer choice is not the key to cost control in health care. From FEHBP's inception, consumer sensitivity to price and quality -- not regulation or price controls --has been at the heart of cost control.

This sharply distinguishes FEHBP from conventional, employer-based health insurance. In these private sector plans, consumer choice based on price does not generally funtion because very few employees have any idea of the price of their health benefits. And, because the tax code gives no breaks to an employee who would buy a more economical, non-company plan to that offered by the employer, in the private sector health insurance world, there is no incentive to shop around in the way that federal workers do. Instead, a health care plan is treated as a "free" benefit that comes with the job.

Twin Principles. Congress explicitly based FEHBP on the twin principles of consumer choice and market competition. Liberal lawmakers have emphasized these principles within the federal system covering themselves, even while many of these lawmakers seem to reject the same principles when considering a new system for all other Americans. Said Representative Mary Rose Oakar, the Ohio Democrat and former Chairwoman of the House Subcommittee on Compensation and Employee Benefits, in 1984:

The two fundamental principles that grew out of enactment of the 1959 law were: freedom of choice and competition... To ensure this variety of benefit packages to all federal employees, retirees and dependents, at a reasonable cost, the Congress designed a system that promoted competition among a large number of carriers.[REF]

Three years earlier, then Representative Michael Barnes, the Maryland Democrat, who chaired the Congressional Federal Government Services Task Force, told a congressional panel:

Freedom to choose among plans, and thereby to maintain competition among plans, has been the system's first line of defense against skyrocketing premiums. It is a theme sounded repeatedly throughout the Act's legislative history.[REF]

This dynamic of consumer choice within a wide range of competing health plans has helped keep costs in check in the FEHBP. Based on data supplied by Lewin/ICF, the fol lowing chart shows FEHBP premium increases averaged 11 percent from 1981 to 1992 compared to 14.4 percent in private-sector employer-sponsored plans. This trend is a continuation of the generally favorable pattern of FEHBP performance revealed by CRS figures for the 1981 to 1989 period.[REF] While private sector plans annual premium increases have been in double digits, the FEHBP averages in recent years have been in single digits. Far 1993, average premium increases in the FEHBP are projected at 9 percent.[REF] The 1992 average FEHBP premium increase was 7.4 percent, while the private sector plans averaged 12 percent. For 1991 the FEHBP premium increase was 4.7 percent, while private employers plans increased by 12.5 percent.

But the relative performance of the FEHBP is even better than the total numbers show. A number of factors, for example, should be driving up FEHBP costs. FEHBP imposes no pre-existing condition requirements on its enrollees, and FEHBP covers 1.5 million retirees, plus their spouses and survivors.

In the private sector only one-third of companies offer health care coverage to their retirees, and the companies that do are cutting back on these benefits.[REF] But in the FEHBP, retirees make up about 40 per cent of total enrollees, including a large number of federal workers, including a large number of federal workers ineligible for Medicare, including those who retire early at age 55 with thirty years of service.[REF]

Retirees, of course, consume more health care services than do those of working age. [REF]

Why the FEHBP Out-performs the Private Sector

It is not often that a federal program is a better model of a free market in action than the equivalent private sector program But the FEHBP is for two reasons. First, the federal government created a system based on consumer choice and market competition-a system in which market forces, not regulation, force improvements in efficiency and encourage innovation among providers. Second, the tax system affecting non-federal workers has so distorted the market for health care in the private sector that the power of consumer choice has been suffocated.

The tax code gives American workers an unlimited tax break on health plans if -- and only if -- the health plans are provided by their employer If the employer does not offer a plan or if a worker noticed that some other plan actually was better value for money, in almost no instance does the tax code give the worker any tax relief for selecting a better plan.

The tax benefits for private sector workers, moreover grow as the generosity of the company plan grows. So, union bargainers have an incentive to press for tax free health benefits rather than for taxable wage increases. This tends to push up health spending and health costs, and blunts employee sensitivity to these costs. By contrast, the federal government contributes a maximum amount to each employee. Historically , members of Congress and federal emploees have paid more out of pocket for health insurance than employees in the private sector.[REF] Unlike .the unlimited tax break for free company plans in the private sec tor, this means there is a much greater sensitivity to the price of health benefits by enrollees in the FEHBP.

Private employer-based insurance practices, heavily and artificially influenced by the federal tax code, have led to two characteristics of private coverage that now am routinely described as a crisis. One is soaring health care costs, due to the lack of price sensitivity by employees. The other is that a family's employer is the key to its health care. This not the case in other areas of insurance, like life insurance, car insurance or home-owners insurance. Only in health care is the extent and availability of insurance determined by mes employer. And only health benefits suddenly are at risk if an American changes jobs or is temporarily unemployed.

HOW TO MAKE THE FEHBP BETTER

The 1989 Congressional Research Service Study of the FEHBP, the most comprehensive analysis ever conducted, notes "That FEHBP has continued to 'work' over the years, despite major changes in the environment in which it has operated, reflects the soundness of its basic design."[REF] Nevertheless, Congress can take steps to make the program work even better. It can improve addressing the programs administration. And it can reduce the "adverse selection" problem. Adverse selection is the gravitation of younger and healthier employees to lower cost plans, leaving older, sicker and more costly enrollees concentrated in progressively higher cost plans As economist Walton Francis notes, the FEHBP, "has only one major problem -- adverse risk selection created by the failure to experience rate premiums to the radically differing actuarial costs posed by different pups of enrollees. This problem creates others, but they are derivative."

Some wish to "solve" this problem by eliminating or drastically reducing the employee choice and carrier competition But this would trade in the efficiencies of market forces for the disadvantages of a Medicare-style system, plagued by rising costs, reams of red-tape and congressional benefit setting. A far better approach, building on the solid success of consumer choice and competition in the FEHBP, would be to allow premiums to reflect more closely the actual cost of serving retirees and active employers, and to subsidize higher cost retirees directly.

Specifically, to make the FEHBP work even better, Congress should 1) Establish separate premiums for employees and retirees Active employees and federal retirees currently pay the same premiums for their health insurance, despite the fact that the costs for these pups very different. Older persons and families typically have much higher health care costs than younger persons and families. The FEHB P does provide different premium rates for individuals and families, reflecting the fact that costs incuxred by a family normally are higher than for single individuals But it does not allow for different rates between employees and retirees, or between retirees who are eligible for Medicare and those who are not Today, older, higher-risk retirees gravitate toward a particular health care plan, they raise disproportionately the costs of that plan and yet do not pay higher premiums and thereby contribute mo re revenue to cover their higher costs. When a large number of mtirees pick a particular plan, the effect is to force the plan to raise its premiums to cover the added cost.

But the effect of higher premiums is to encourage lower-risk employees, with low medical costs to leave it for a cheaper plan. High cost individuals thus end up being concentrated in fewer and fewer plans; and these plans, covering higher cost enrollees paying artificially low premiums, find it progressively more difficult to compete with lower-cost plans with younger enrollees As Walton Francis and other economists argue, if these premiums for higher risk rethees reflected their actuarial cost, then the decision of a large number of retirees to pick a particular plan would not necessarily force higher premiums for lower-cost active employees, or Medicare-eligible annuitants, already enrolled in the same plan. The cmnt problems of ad verse selection thus would disappear.

Because higher premiums for retirees would increase their financial burden, the government could offset the impact on these elderly citizens by making a larger government contribution to the cost of their premiums, with perhaps slightly lower contributions for active employees, so that the net cost to government remained the same 29 Francis, op. cir p. 8 17 I 2) Enhance competition and simplify administration New fee-for-service plans today must win approval from Congress before being allowed to compete in the federal insurance program, while HMOs do not. Although Congress traditionally has been inclined to permit such new plans to join the system, especially if they are sponsored by union or employee groups, there is always a danger that access could be un duly politicized. In any case, the decision as to whether a plan is qualified to enter into FEHBP competition should be an administrative decision of the civil service, guided by standards of consumer protection, rather than a legislative decision influenced by political connections or lobbying standardized and simplified, and greater ease of entry should be established. OPM, not Congress, should determine qualifications for entry of all types of plans into the FEHBP.

And instead of meddling in the details of rates and benefits of almost 400 plans, OPMs authority should be limited to establishing and enforcing common basic ground rules far market competition. These rules should be confined to establishing minimum benefit requirements, including catastrophic protection, fiscal solvency requirements, the promotion of consumer information and the protection of consumers hm fraud. With every plan required to provide at least a basic benefits package within the ground rules, any plan meeting OPM administrative standards should be permitted to compete Thus the current requirements for all plans to enter and stay within the FEHBP should be

LESSONS FOR HEALTH CARE REFORM

Opponents of consumer-based health care reform in Congress and the press often argue that Americans just are not competent to make wise choices about health care plans. They say that Americans cannot weigh price, value and benefits. They also say that such a system would not constrain costs. Therefore ey insist, while consumer choice may sound good in theory, and works in the rest of the economy, it could not work in health care.

This is flatly contradicted by the experience of the FEHBP. And it is especially ironic that the lawmakers who reject the idea of consumer choice in health care actually exercise choice themselves every year in the FEHBP and resist every effm to take away that choice.

The experience of the FEHBP has many lessons far lawmakers now engaged in the debate over reforming the U.S. health care system-and each of these lessons points to the workability and desirability of a universal health care system based on the kind of consumer choice taken for granted for federal workers-and members of Congress. Among the salient lessons Lesson #1: Ordinary Americans are quite capable of making sensible choices regarding their health care plans Federal workers are not the wide-eyed hapless consumers pmtrayed by opponents of consumer choice in health care. They do not shop around in a bewildering market, falling prey to powerful insurance companies. On the contrary, consumers indisputably have the upper hand and force plan providers to adapt to their demands or suffer the consequences. Big insurance carriers like Blue Cross and Blue Shield find themselves, each year, in a bruising battle for market share with plans offered by entrepreneurial employee organizations like the Mail Handlers and managed care plans 18 One valid criticism of the FEHBP actually underscores the power of consumer choice rhat is the problem of adverse selection, meaning that lower risk enrollees, free to shop among competing health care plans each year, tend to gravitate to leaner, lower cost plans resulting in the cost of serving higher-risk individuals, concentrated in comphensive plans pushing up the cost of more comprehensive plans. But as Ben Lytle, President and CEO of the Associated Group, an insurance company based in Indianapolis, Indiana, explains, ad verse selection is the insurance industry's term for the consumer outsmarted us. He figured out that he could buy a policy and get more in benefits than we charged him in premiums.

Adverse selection, however, would be largely avoided if the governments sha of plan Eosts were revised to allow plans to charge higher prices for high-risk individuals, such as retirees, without the enrollees share of these costs rising significantly. For opponents of consumer choice, adverse selection presents the supreme conundrum: they cannot logically argue that adverse selection resulted from consumer choice based on self-interest, while simultaneously holding the position that consumers are incapable of making rational choices Lesson #t2: Consumer information becomes readily available once consumers are permitted to make choices.

The ready availability of consumer information in the FEHBP exists because nine million Americans have the right to choose a plan. If consumer choice of health plans were avail able to all Americans, there would be an explosion of usable consumer information Lesson 3: Consumer choice is a simpler and more effective way to control costs than regulation and price controls.

While the huge federal Medica program, Americas foremost experiment with single payer government health care insurance, is characterized by mountains of increasingly unintelligible regulations governing doctors and patients, FEHBP remains simple. Medica is moving actively toward price controls an48ther features of centralized planning. FEHBP meanwhile, has been relatively passive. And largely devoid of consumer choice, private sector health care plans are finding it hard to control costs, with larger average premium increases than the FEHBP, even though most private sector health care plans do not even cover high cost retirees Lesson #4: When consumers pay premiums directly, albeit with government help, they resist mandates which raise health costs.

If Congress mandates a benefit in a system where there is direct and immediate cost-shar ing between the government and the employees and retirees, the kt and immediate finan cial impact of this mandate shows up in higher costs f or both, as well as for the taxpayers.

This has made Congress very resistant to the kind of special interest medical lobbying that has been so successful elsewhere 30 CRS Report. p. 239 19 Lesson #5: A consumer choice system is simple and inexpensive to administer Even though they individually purchase their health insurance package, congressional and federal employees and retirees in the EHBP do not have to wony about making sure that their insurance premiums are paid; the federal government, as employer , pays them to the carriers A payroll deduction is made by the federal government each pay period, and the funds are deposited in a government account for transmission to the private carriers.

In designing a consumer-based health care system for America, w here families would have the option to choose among many different types of plans with the same tax breaks employers, like federal agencies in the FEHBP, also could be required to make payroll deductions for premiums for workers and transmit these premium payments to the insurance carriers of the employees choice Lesson M: A consumer-choice system is better than regulation in encouraging cost saving health care innovations, like managed care When consumers can choose health plans on the basis of quality and price, providers that use innovative ways to deliver care at lower cost have a competitive advantage. When employers pay for the plans, consumers understandably want generous plans without regard for value. That is why managed care, union plans, and ot her innovations are common in the FEHBP but rarer in the private sector or in all-payer programs like Medicare. Innovation similar to the FEHBP could be expected if all Americans had a choice of health plan.

If a federal worker moves from the Treasury to t he Pentagon, or takes a job on Capitol Hill, he or she keeps the same health plan and there is no interruption in benefits. If private sector employees lose their jobs or change jobs, they do not lose their homeowners insurance, their auto insurance or their life insurance. They only lose what is arguably their most important insurance their family's health insurance. With a consumer-based system, in which the tax relief goes directly to individuals and their families, either in the form of cred its orvouchers, irrespective of where they work, employees could choose a health coverage that had nothing to do with their place of work, and would accompany them from job to job HOW CONGRESS SHOULD REFORM AMERICAS HEALTH CARE SYSTEM It would be Rlatively simple f o r Congress to amend current law so that every working American family in effect would have the same type of choices available to Congress and other federal employees. Doing so would require three basic steps. First, the tax treatment of health care would have to be reformed, such that families would have the same system of tax lief wherever they chose their health plan and wherever they worked. Second, the tax relief would have to be changed to give more help to lower-paid workers and those facing higher insurance and medical costs, and a limit placed on the tax break for plans purchased by affluent Americans. These changes would deal with most of the adverse selection problem experienced in the FEHBP system 20 And third, there would have to be some changes in insurance regulations to discourage plans from turning down potentially high cost enrollees or charging them prohibitive premiums.

A proposal to accomplish this has been advanced by The Heritage Foundation. Known as the Consumer Choice Health Plan, this would replace the current tax-free fringe benefit status of company-provided plans with a refundable tax credit for buying health insurance or medical services. All families would be required to obtain at least a basic plan. And insurance companies could not cancel coverage because of high claims, nor could they refuse to cover an individual or apply a premium surcharge higher than a specific percentage. In addition, just as in the FEHBP, employers would be required to make a payroll deduction on be half of each employee and send premium payments to the plan chosen by the worker The Heritage Consumer Choice Health Plan not only would guarantee all American workers and their families access to coverage, but would do so without Equiring massive tax increases or deficits. According to an analysis on the plan conducted by Lewin/ICF, one of the nation's leading econometrics firms, the tax and market changes proposed by The Heritage Foundation would result in a net savings of $10.8 billion in the health care system in first year. And most American families would be better off than they are today. Using a combination of tax credits and vouchers, a typical family earning between $30,000 and 40,000 per year would benefit most by The Heritage Foundation's propose d tax and insurance market changes.

The Heritage Foundation's Consumer Choice Health Plan is embodied in S. 3348, introduced this fall by Senator Orrin Hatch, the Utah Republican. Under the Hatch bill, each family would be eligible for a refundable credit for the purchase of insurance and the payment of out of pocket expenses. And like members of Congress and federal employees American families would be able to pick and choose the kind of health cam plan that best fits their needs. Moreover, every American family would benefit from a comprehensive set of insurance market reforms. Like members of Congress and federal employees, for in stance, American families would have the right to renew their coverage each year 31 CONCLUSION Members of Congress would not even think of giving up the benefits of choice and com petition in their own health care system. Indeed, they have taken pains to exeqt them selves from many of the "reforms" they would impose on all other Americans. Lawmakers should reflect on this in developing a national health care system for all Americans.

Instead of trying to build upon the employer-based model that does not restrain costs and contains many other flaws, or instead of introducing a massive nationalized system based being rejected by t heir former admirers throughout the world, Congress should adapt and re I I on rationing, price controls and all the other crude instruments of central planning now 31 See Butler, Talking Points Part II, p. 21 32 For example, Senator George Mitchell's "play or pay" proposal (S. 1227 which is one of the leading hdth uue reform proposals now before Congress, explicitly exempts members of Congress, their staffs, and other federal employees. See Edmund F. Haislmaier, "The Mitchell HealthAmerica Act A Bait and Switch for American Workers Heritage Foundation Issue Bullerin No. 170, January 17,19

92. See also Moffit, op. ur 21 fine the system that works so well for federal workers: a system characterized by consumer Ehoice and competition. This system should be pe rmitted to all Americans By building upon these principles, Congress would improve its model Federal Employee Health Benefits Program and also lay the foundation for a genuine consumer-based national health program. Driven by the same dynamics of consumer choice and market competition that work so well in the rest of the economy, such a consumer-based system would mean af fordable and adequate coverage for every American family. What is available for Congress and its employees should be ma& available to ev ery American family.

Robert E. Moffit, Ph.D.

Deputy Director of Domestic Policy Studies 22