Abstract: In May 2010, the U.K. general election resulted in a hung Parliament from which emerged a Conservative–Liberal Democrat coalition with Conservative leader David Cameron as Prime Minister. The experiment was widely justified by the evident need to cope with the economic crisis and, in particular, the unsustainable budget deficit inherited from the outgoing Labour government. Mr. Cameron and his Liberal Democrat Deputy Prime Minister, Nick Clegg, also claimed to be introducing a new and better kind of politics, one based on reasoned discussion and a rejection of “tribal loyalties.” In practical terms, both sides then made a series of policy compromises.

It is now clear how this bipartisan model of governing has fared. First, little or no progress has been made in tackling either the budget deficit or the British economy’s underlying weaknesses. Second, no credible, coherent, or convincing path toward national recovery has yet been presented. The latter is consequential, both in terms of the Conservative Party’s failure when in opposition to think seriously about large policy questions and now in terms of the inability of a coalition, hampered by incessant compromise, to react to major changes in circumstances—as with the unresolved, and arguably unresolvable, euro-zone crisis.

For the United States, with its different constitutional system and electoral cycle, the applicable lessons would seem to be twofold. The first conclusion is encouraging. In the United Kingdom, an electorate not dissimilar from that in the U.S. has proved to be stoical if not enthusiastic when convinced that unpalatable economic medicine is required. The second conclusion constitutes a possibly timely warning: Failure to devise and present a clear analysis of the country’s ills before achieving power will leave even a well-intentioned and right-thinking government floundering as new, unforeseen challenges threaten to throw it off course.

Section I

Introduction

In May 2010, the U.K. general election resulted in a hung Parliament from which emerged a Conservative–Liberal Democrat coalition with David Cameron, the Conservative leader, as Prime Minister. Britain has a long history of coalitions that were not unsuccessful, but since the Second World War, British party politics has been sharply polarized. So the 2010 outcome was a novelty.

The experiment was, however, widely justified by the evident need to cope with the economic crisis and, in particular, the unsustainable budget deficit inherited from the outgoing Labour government. Mr. Cameron and his Liberal Democrat Deputy Prime Minister, Nick Clegg, also claimed to be introducing a new and better kind of politics, one based on reasoned discussion and a rejection of “tribal loyalties.” In practical terms, both sides then made a series of policy compromises.

It is now clear how this bipartisan model of governing has fared.

The overall judgement must so far be a qualified negative, though the final outcome remains unclear. Certainly, the worst predictions have gone unfulfilled. Opposition to public expenditure cuts has been relatively muted; trade union protests and strike action have had little effect; and there is widespread public acceptance, in the short term at least, of the sharp pressure on living standards. Moreover, both the still-fresh recollection of the shortcomings of Gordon Brown’s government and the perceived failings of the present Labour opposition have kept up the coalition’s political ratings.

The problem is, first, that little or no progress has been made in tackling either the budget deficit or the British economy’s underlying weaknesses and, second, that no credible, coherent, or convincing path toward national recovery has yet been presented. The latter is consequential, both in terms of the Conservative Party’s failure when in opposition to think seriously about large policy questions and now in terms of the inability of a coalition, hampered by incessant compromise, to react to major changes in circumstances—as with the unresolved, and arguably irresolvable, euro-zone crisis.

For the United States, with its different constitutional system and electoral cycle, the applicable lessons would seem to be twofold. The first conclusion is encouraging. In the United Kingdom, an electorate not dissimilar from that in the U.S. has proved to be stoical if not enthusiastic when convinced that unpalatable economic medicine is required. The second conclusion constitutes a possibly timely warning. This is that failure to devise and present a clear analysis of the country’s ills before achieving power will leave even a well-intentioned and right-thinking government floundering as new, unforeseen challenges threaten to throw it off course.

Section II

The Legacy from Labour and the Compromises Reached Between the Governing Coalition Parties

The Labour government had overspent under both Tony Blair and Gordon Brown.[1] An inherited budget surplus had become a regular budget deficit, predictions of economic growth were overly optimistic, and plans for public spending were unaffordable. When the financial crisis and recession of 2007–2009 hit, Mr. Brown, true to his prejudices and convictions, then spent much more. This dramatically worsened the state of public finances without avoiding recession.

On the eve of the 2010 general election, Labour finally promised to rein back the deficit, but without providing details. The Conservatives in the election campaign were equally—and deliberately—reticent, though they promised quicker action to curb borrowing. This urgency was amply justified. The U.K. budget deficit in Labour’s last year rose to 11 percent of gross domestic product (GDP), the highest in the country’s peacetime history and the largest structural deficit in Europe.

An emergency budget introduced on June 22, 2010, by the new Chancellor of the Exchequer, George Osborne, promised to eliminate the U.K.’s structural deficit in 2014–2015. Debt was by then supposed to be falling as a share of GDP, with 80 percent of the deficit reduction to be secured by spending cuts and 20 percent by tax increases. This approach showed courage, but one should not exaggerate the severity of what was planned (let alone achieved). Total public spending in 2014–2015 would still have been higher in real terms than it was in 2008–2009. In any case, this announcement, with the underlying intent it signified, reassured financial markets. The confidence thus engendered has since kept down the cost of servicing existing debt and new borrowing.

But the Conservatives, in exchange for agreement from their coalition partners, also made a series of concessions. Here many of the current difficulties find their origin. Tax cuts were avoided or slanted toward groups favored by the Liberal Democrats. Upgrading of the Trident independent nuclear deterrent was postponed. Measures to check the inroads of the European Court of Human Rights were all but abandoned.

Of greatest current political significance, promises to curb the powers of the European Union (EU) were diluted. This, it should be noted, was very much in line with David Cameron’s own tactical preference. In his 2006 Conservative Party Conference speech, his first as party leader, he had encapsulated his explanation of the party’s failure to win the previous year’s election in a telling sentence: “While parents worried about childcare, getting kids to school, balancing work and family life—we were banging on about Europe.”[2] (Of course, the Prime Minister is now himself “banging on about Europe.”) David Cameron also seriously damaged his credibility in the eyes of his Euro-skeptical party by failing to honor what was seen as a firm undertaking, made in opposition, to hold a referendum on the European Union’s Lisbon Treaty.

The Prime Minister’s compromises on other fronts have come back to haunt him.[3] His inability (in coalition with the Liberal Democrats) to press ahead with curbing the impact of European human rights law has led to a rash of embarrassing failures to deport serious criminals, including those linked to terrorism. Similarly, limiting the government’s efforts to curb immigration—again in deference to Liberal Democrat sensibilities—has seen the government fail spectacularly to reduce net immigration to “tens of thousands.” In fact, net migration is at a six-year high.[4] This is particularly unsettling, since recent figures show that migrants currently take nine out of 10 new jobs.[5]

The Liberal Democrats, naturally, made their own compromises. They achieved key Cabinet posts. In exchange, however, they accepted not just the program of spending curbs and deficit reduction, but both the introduction of university tuition fees—which they had promised to oppose outright—and their introduction at a high level. They thereby did themselves great and possibly irreversible electoral harm.

This has had a paradoxical effect on the politics of the coalition. The collapse in Liberal Democrat support made its leaders fearful of an early election yet even more disposed to criticize particulars so as to achieve a higher public profile. Generally, however, Liberal Democrat priorities have largely coincided with those of Mr. Cameron and the group of “modernizers” who control (but are unrepresentative of) the Conservative Party. As a result, priority within public spending was given to the National Health Service (NHS) and overseas aid over defense and the police. Priority was also given to reducing CO2 emissions and tackling climate change over industrial competitiveness.

Unfolding events have since demonstrated that these priorities were the wrong ones.

Section III

The Story So Far

Foreign and defense policy under the coalition have been bedevilled by strategic incoherence. In response to the “Arab Spring,” Britain took the lead with France in an ambitious military initiative, under disputable U.N. cover, to bring down the Lybian régime of Colonel Muammar Gaddafi. This was a success, but the eventual outcome in Libya (as elsewhere in the Middle East, where differing degrees and brands of Islamism have benefited from the disorder) is far from clear. Certainly, the operation was begun with a very imperfect assessment of the risks and commitment required. In a number of respects, it served as a bad precedent.[6]

This forward foreign policy was and is being played out against very sharp cuts in defense spending and capability—cuts that went against what the Conservatives had pledged in opposition. Britain’s defense spending fell to 2 percent of GDP. Substantial manpower cuts in all three services were made. The Navy was particularly badly hit. Britain’s existing carrier, Ark Royal, is being scrapped; the Harrier aircraft have gone; and the country will have no carrier-borne strike force until 2020. These cuts are set to continue, as was confirmed in the Chancellor of the Exchequer’s 2011 Autumn Statement. Nor is the wider strategic environment neutral.

The problems of the euro-zone countries mean that the contributions of continental European countries to NATO may shrink still further, imposing more strain on Britain—and, of course, on America, where President Barack Obama has also announced a scaling down of commitment to Europe and a shift of strategic attention to the Asia–Pacific region.[7] The subordination of Britain’s defense effort to government budget cutting has been accepted by British military chiefs, but the strains they face are now acute.[8]

Questions have even been raised about how the Falkland Islands would be defended in the event of a renewed conflict with Argentina, which Argentine sabre-rattling suggests is not beyond the range of possibilities.[9] It was recently revealed that last summer, because of the demands of the Libyan war and defense cuts, no warship was available to guard Britain’s home waters for the first time in 30 years.[10] An unforeseen military crisis in some distant theater can never be ruled out. For example, it has recently been announced that in response to Iran’s threat to close the Strait of Hormuz, the Navy is deploying Britain’s most advanced warship, the Type 45 Destroyer HMS Daring, to the Gulf.[11]

At the same time that it has been downgrading its defense effort, Britain has heavily increased its overseas aid budget—by 37 percent. Aid was not only protected against economies imposed elsewhere, but singled out as epitomizing the coalition’s (and the Conservative Party’s) values and priorities. The Prime Minister defends it robustly and has sharply criticized party doubters who object that it makes no sense to send aid to an upwardly mobile superpower like India, which is currently developing its own overseas aid program. There are even plans to legislate so that the internationally agreed target of 0.7 percent of GDP will continue to be met whatever the prevailing financial circumstances might be.[12]

In home policy, a similar incoherence has been evident, though there have been some successes. Far from shrinking the functions of the state and concentrating resources on basic tasks that cannot be performed well or easily by the private sector, the government has continued to increase spending on, for example, the National Health Service. There is, of course, no reason to consider most health provision a pure public good that requires delivery by what amounts to near monopoly provision organized by government.

Early plans for radical reform of the NHS had to be watered down in the light of pressure from vested interests and patients’ groups, but the current reforms still depend on giving general practitioners (i.e., family doctors, the gateway to the system) much greater powers to purchase care for patients from a variety of providers. Unfortunately, as has occurred with other public-sector reforms in the past, a high price has been demanded by those who are expected to exercise more responsibility. In this case, it is envisaged that the pay for general practitioners, which rose sharply under the previous government, is to increase further—by a more than 25 percent.[13]

By contrast, expenditure on law and order has been cut, leading to a reduction in police numbers. The dangers involved were demonstrated by the shocking urban riots of August 2011, which involved several deaths, injuries to police and members of the public, and widespread looting and arson on a scale not seen in Britain for 30 years. More than 3,000 people were arrested. The police initially failed to gain a grip on the disorder, which then rapidly spread in classic copycat fashion. Although various theories circulated as to the root cause of what occurred, the most significant indicator is probably that three-quarters of those charged already had criminal records. Those with criminal records had, on average, committed 15 previous offenses.[14]

In other words, the riots were the unpleasant tip of a much larger and more menacing iceberg of criminality that the authorities have been unable to tackle. A long list of social policy measures was announced in reaction to these events, but the obvious response—lengthening sentences, increasing police numbers and enlarging prison capacity—would require reordering spending priorities in a way that is impossible while the Liberal Democrats, always enthusiasts for liberal penology, remain in the coalition.

In two areas of domestic policy where ministers have set out a guiding philosophy rather than embarked on a series of ad hoc measures, recognizably Conservative priorities are being reflected in policy. Work and Pensions Secretary Iain Duncan Smith has been seeking to ensure that it is always worthwhile to work rather than to live on welfare. Long-term welfare dependence has rightly been identified as a social scourge, not merely a burden on public spending and diversion from wealth creation. The Department for Work and Pensions has recently cast light on the well-known but rarely mentioned connection between welfare and criminality, releasing figures which show that a third of those claiming unemployment benefit have criminal records.[15]

The method adopted by Mr. Duncan Smith to achieve radical reform of the system involves replacing dozens of existing benefits with a single Universal Credit. There are, however, two significant problems with this radicalism.

- The first problem is inherent in what is proposed. Unless significant numbers of poorer people are to receive less in benefits than they do at present, then making it always worthwhile to work will involve at least short-term increases in public spending (or in tax revenues foregone). So there will be an adverse effect on the already swollen budget deficit. Naturally, the Treasury will resist or frustrate such measures—as has been the case in several instances.[16]

- The second problem is technical but no less serious. In order to give effect to the highly complex changes involving amalgamation of taxes and benefits, a new IT system is required. Past experience of such projects in the public sector has been far from encouraging. Already, Members of Parliament and others have voiced their worries about the timetable and practicability of what is now proposed.[17]

By contrast, headway has already been made by Michael Gove, the Conservative Education Secretary. Mr. Gove is engaged in a number of semi-public quarrels with his own officials and teachers’ interests on a wide range of education issues, the outcome of which is still unclear. One area where progress has been swifter than many envisaged is in promoting a model of schools that are government-funded but free of most government—especially local government—interference.

So far, building on the previous Labour government’s model of independent “Academies” (which itself resurrected the previously abandoned Thatcher government’s concept of “Grant-Maintained Schools”), more than 1,500 existing schools have adopted independent academy status under Mr. Gove’s initiative. The difficulty has been in trying to persuade new providers to start schools. In fact, fewer than 50 have done so. Yet this is crucial if the existing vested interests and the egalitarian ethos they encourage are to be challenged through competition. Supply has to exceed demand if parental choice is to be real.

A new “free schools” model, based improbably enough on Swedish experience, is also receiving the Education Secretary’s quiet encouragement. These schools, in addition to being independent, could be run on behalf of parents by professionals, commercially and at a profit. The first—itself only a halfway house to the fully functioning free school—has long awaited Departmental approval. Liberal Democrat obstruction within the coalition, joined to bureaucratic inertia, is a problem. The fact remains that introducing some degree of profit motive is obviously the best way both to set new schools on a sound financial basis and then to help those that prove successful to expand.[18]

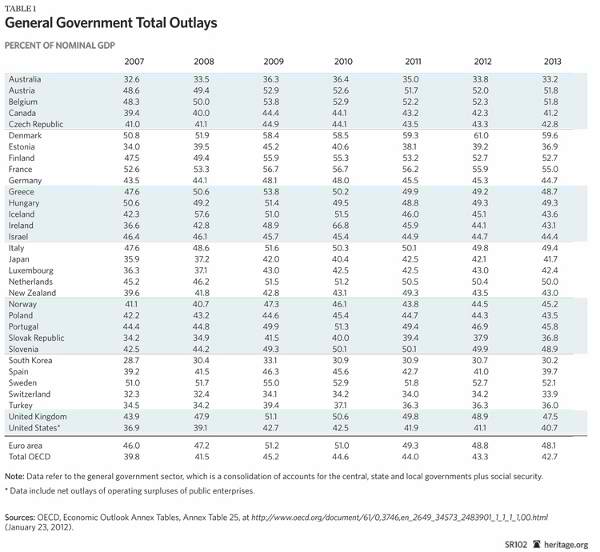

The country’s and the coalition government’s most serious worries, however, concern economic policy.[19] This is not, it should be noted, simply a question of the failure to achieve the planned budget deficit cut (itself dependent on growth and bedevilled by the lack of it). It is also the result of still-untackled structural problems. Britain remains hampered by high public spending. For three years, government has been spending 50 percent or more of national income. (See Table 1.)

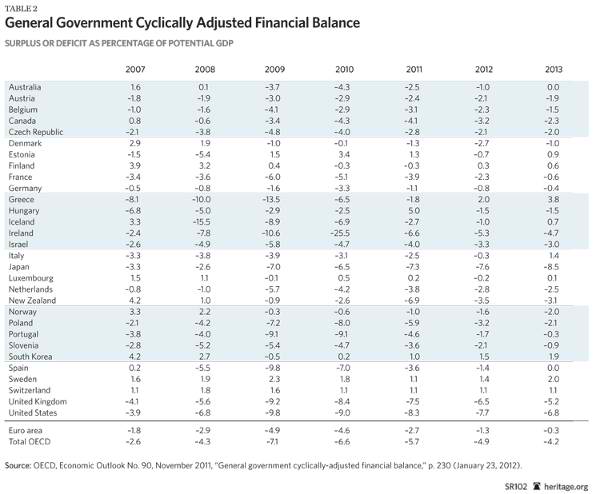

Overspending is the root cause of the swollen government budget deficit. The latest Organisation for Economic Co-operation and Development figures show that on this score, Britain is relatively badly placed. (See Table 2.)

A further result of an excessive share of national income taken by government is usually low growth, because productivity is characteristically lower in the public sector than in the private sector. Yet another, of course, is that high public expenditure over time leads to high taxes, which again discourage wealth creation—as has happened in economically stagnating Britain. For example, the latest World Economic Forum’s Global Competitiveness Report finds that tax rates are viewed as the most problematic factor for doing business in the U.K.[20] Similarly, the most recent Heritage Foundation/Wall Street Journal Index of Economic Freedom marks down the U.K. on both government spending and monetary freedom.[21]

The 50 percent top income tax rate, introduced in 2010 by the Labour government but retained by the coalition, remains a significant disincentive to those who might be minded to locate to or stay in Britain. It is, with Japan’s top rate, the highest of all the G8 countries. The Centre for Economics and Business Research estimates that it is set to cost the government £1 billion a year in lost revenues by the middle of the next decade.[22]

No major progress on tax or deregulation seems possible, however, while the Liberal Democrats remain in the coalition. If, as expected, a Treasury report on the 50 pence rate this coming spring shows that it (even now) yields little or no revenue to the Exchequer, it is still likely to be retained. Even if it is ended, some equally socialistic and damaging measure—a “mansions tax” has been mooted by the Liberal Democrats—is likely to be introduced in its place.

Britain also suffers from a surfeit of regulation. Labor-market regulation currently inhibits job creation—something that is particularly serious at a time of high and rising unemployment. (A review of the current law relating to employee dismissal has been announced, but the Liberal Democrats are opposed to any far-reaching measures). Energy policy, where the Cabinet minister in charge is also a Liberal Democrat, is forcing up costs to industrial and private consumers.[23] This is another inhibitor of growth.

Finally, the flow of European regulation, which the government has been unable to check—despite the Conservative Party’s earlier pledge to negotiate the return of social and employment legislation powers to Britain—is also reducing flexibility and pushing up costs. The Open Europe think tank, for example, has estimated the cost of EU social law to U.K. business and the public sector at £8.6 billion a year. The point is not, of course, that all these regulations could or should be repealed, but that the U.K. is currently effectively prevented from deciding what deregulation in these areas makes sense in order to make business more competitive and government smaller.[24]

Section IV

The Current Crisis

The Chancellor’s Autumn Statement, delivered on November 29, 2011, confirmed that no progress has been made in either curbing the deficit or generating growth. To the contrary, the Office of Budget Responsibility (OBR), set up the previous year by the government to provide an authoritative and independent analysis of the public finances, radically revised its earlier estimates. (See Table 3.)

- The OBR cut its growth predictions from 1.7 percent to 0.9 percent in 2011, from 2.5 percent to 0.7 percent in 2012, and from 2.9 percent to 2.1 percent in 2013.

- It forecast that unemployment would rise from 8.3 percent today to 8.7 percent in 2012 but then start to drop back.

- It showed that public-sector net debt would peak at 78 percent of GDP in 2014–2015, which is 7.5 percentage points higher than forecast in the March 2011 budget.

- Most notably, given the high political importance the government has attached to it, the OBR forecast shows that the targeted reduction and elimination (by 2014–2015) of the cyclically adjusted budget deficit was way off track.

The OBR and the government blamed this failure and the lack of growth that explains it on three factors: higher than expected inflation driven by a sharp increase in global commodity increases, instability and uncertainty in the euro zone feeding through into domestic and international lending and consumer spending decisions, and a sharper than expected decline in the trend rate of growth resulting from the damage done by the 2008–2009 financial crisis. It should be noted, however, that these forecasts are also based upon what seems to many people an inordinately optimistic reading of future events. The OBR itself thus qualifies its projections with an obscure but unsettling observation:

The central economic and fiscal forecasts and judgements assume that the euro area finds a way through its current crisis, but a more disorderly outcome is clearly a significant downside risk. This risk cannot be quantified in a meaningful way, as there are numerous different ways in which such an outcome could unfold. Suffice to say, the probability of an outcome much worse than our central forecast is greater than the probability of an outcome much better than our central forecast.[25]

In any case, the question confronting the government was: What could be done to bring the deficit and debt reduction plan back on track? The answer it devised was fourfold.

First, the Chancellor rolled the deficit elimination target forward two years from 2014–2015 to 2016–2017. Had he simply done that, the government’s strategy would have been rendered incredible, with dangerous implications for market confidence. So, second, he also pencilled into his plans £15 billion of spending cuts in 2016–2017, after the expected date of the next election.

The reaction of markets to these announcements was relaxed. Britain continues to borrow to finance its debt much more cheaply than most of the euro zone does. But, apart from the implications of what happens to the euro, there is another reason to worry. The politics of going into an election with the prospect of large spending cuts, and no tax cuts, after it, are so unattractive as to make it likely that the politicians’—especially Liberal Democrat politicians’—resolve may crumble.

Third, the government has announced specific measures intended to stimulate growth and jobs, but these are neither very far-reaching nor necessarily very well focused. There is a concentration on developing Britain’s infrastructure. The Prime Minister is on the record as believing that, “in terms of future productivity [Britain’s] infrastructure deficit is as serious as our budget deficit.”[26] Accordingly, £5 billion is to shift from current to capital spending. This, though, is only part of what the Autumn Statement terms “a new strategy for coordinating public and private investment in UK infrastructure.” The government hopes to persuade the U.K. pension funds, which currently are starved of investment opportunities giving savers a useful return, to channel billions of pounds into such projects.[27]

Questions remain, however. The actual rather than potential sums involved remain modest and will take several years to have an effect. The real economic benefits of such projects are notoriously difficult to judge, are often exaggerated, and typically have little effect on unemployment—as was exhaustively demonstrated when the same debates in similar circumstances occurred in Britain in the early 1980s. Perhaps most important of all for the pension funds managers, it is notoriously difficult to capture or privatize the returns to such investment having privatized some of the financing.

The government also wants to ease credit for business and would-be home buyers, but measures to make it easier for small and medium-sized firms to borrow, through a National Loan Guarantee Scheme, and to make it easier for people to obtain mortgages for newly built homes run the risk of once more encouraging companies and individuals to incur debts they cannot repay. In any case, to demand easier credit from banks that are also under pressure from increased tax and from planned new regulation is arguably to demand the impossible.

A series of other measures of varying benefit and importance were also announced. Reforming the terms of public-sector pensions (whose benefits are well out of line with their private-sector equivalents); bringing forward the planned change in the state retirement age (to 67); and reform of employment law (if pursued vigorously despite Liberal Democrat obstruction) may all contribute to improvements in economic efficiency but will have little or no impact in the immediate future. A new “Youth Contract” scheme worth almost £1 billion will fund employers to take on young people.

This may help provide employment to a population that is particularly at risk, but as government must borrow the funds to provide these jobs, thereby destroying other jobs in the private sector, this should not be confused as a net job creator. It is not. The Chancellor also announced a number of fiscal bribes to various vocal groups—cutting one region’s water bills, restricting rail fare increases, and enlarging the scope of subsidized child care. These will have no effect on growth, but rather suggest a basic lack of seriousness reminiscent of Gordon Brown at his worst, as commentators have noted.

Finally, underpinning the whole approach to reviving growth is the continued commitment of the Bank of England, strongly endorsed by the government, to “Quantitative Easing” (QE). In 2009, George Osborne, then Shadow Chancellor, described printing money as “the last resort of desperate governments when all other policies have failed.” In office as Chancellor, however, Mr. Osborne has shown no such reticence and has repeatedly urged a continuation of the program.

The Bank of England has dismissed fears that QE will lead to future inflation (now standing at more than twice the official 2 percent target). However, the London-based Centre for Policy Studies notes that the Bank’s Monetary Policy Committee has recently had a poor record of prediction, significantly underrating the actual inflation outturn.[28] High inflation, among other effects, redistributes wealth in favor of overindebted government and banks, and those on indexed benefits, and against savers and those in work. It also threatens consumer and business confidence, thus depressing the actions necessary for growth, and lays in the necessity of a growth-depleting subsequent disinflation. The strategy is, therefore, far from risk-free in the short run and inherently self-defeating after only a couple of years in practice.

The only sure way to generate growth in the current circumstances, in which demand at home and abroad is depressed, is through radical supply-side reform to increase efficiency. This is not currently occurring; nor is there any evidence that it can occur, given the political constraints of coalition.

Section V

The European Dimension

Britain’s economic and, in the long run, strategic problems intersect with those of Europe in a number of ways. The reaction to the euro-zone crisis and specifically to the British Prime Minister’s effective veto of a new treaty at the Brussels summit on December 9, 2011, highlighted some of these difficulties.

The fact that Britain is outside of the euro and thus able to set its own interest rates and pursue its own monetary policy, reflecting its own interests, is arguably the single most important guarantee of the country’s economic stability. Monetary sovereignty is a necessary, albeit necessarily insufficient, condition for prosperity, which ultimately depends on selling goods and services that people wish to buy. This is because it allows Britain to respond to external shocks with flexibility and without the kind of endemic crisis that now afflicts even the stronger countries in the euro zone. The markets’ perception of this advantage currently allows Britain to continue to borrow cheaply to fund its borrowing, despite the lack of progress so far in bringing down the budget deficit and the increases in debt.

By contrast, the AAA sovereign credit ratings of not just the weakest euro-zone members, but now France—joint leader of the pack with Germany—have been downgraded. Recognition of this divergence of fortunes with those of the euro zone has led in Britain to the wholesale discrediting of politicians and pundits who have argued over the years for closer integration with Europe. Indeed, their predictions have been held up to humiliating ridicule.[29] It has, similarly, led to acceptance of the fact that Margaret Thatcher was correct when she fought in 1990 to keep Britain out of the emerging euro and, indeed, when, 12 years after leaving office, she predicted: “The European single currency is bound to fail, economically, politically and indeed socially.”[30]

On the other hand, the coalition government had not, at least until the Brussels summit, seriously grasped where events were leading and which options were opening—and which closing—for Britain. For months, both the Prime Minister and the Chancellor had publicly called on the euro-zone countries to move much closer toward a single economic government. While leaving the prescriptive details to others, the British government was also strident in its criticisms of European leaders’ failure to create what was termed a “firewall” against speculation at the expense of the weaker members of the system. This tactic caused deep resentment among euro-zone leaders, as Mr. Cameron would later discover.

It was apparently assumed by Britain that the only risk to British national interests was to be found in a possible collapse of confidence, including a collapse of European banks, arising from the crisis. That eventuality, it was reckoned, would still further postpone British economic recovery. The government seems, however, to have given little or no serious thought to three other questions that should go to the heart of British strategic calculations in Europe:

- Is it compatible with British national interest to see a tightly controlled, German-dominated, single power bloc emerge in Europe in place of the malfunctioning but largely unthreatening European Union in its present form?

- If, for well-known reasons—above all, because of the difference in productive potential between member states—the euro simply cannot work, is it not a recipe for chaos rather than order to urge and support its retention?[31]

- Of most immediate significance, how can Britain’s interests be safeguarded within the European Union under current treaty arrangements, which largely provide for majority voting rather than decision by consensus, if the euro-zone countries, joined by aspirant members and other dependents making up the great majority, henceforth act as a united bloc?

Such is the background of the diplomatic crisis in Europe that is now imposed on the economic crisis. Mr. Cameron went to Brussels in December poorly prepared in every sense. He had not resolved how he was to respond to the demands of his own party for a return of powers to Britain from Europe in exchange for agreement to treaty changes required for a European fiscal union. He had not prepared the Germans for the demands he was to make for a protocol to be added to the proposed new treaty so as to protect the interests of the City of London from damaging regulation and a proposed new tax on financial transactions.

He also had not reckoned at all, it seems, with French plans to force Britain out of the cockpit in Europe—plans that fit in well with President Nicolas Sarkozy’s desire for a noisy coup that would help his re-election prospects and with a well-entrenched resentment in Paris at London’s primacy in financial services. The British Prime Minister’s own hope was, it appears, to strike a deal with German Chancellor Angela Merkel, then agree in principle to the treaty changes, and then return to the House of Commons and try to bulldoze through a compromise that his already rebellious backbenchers would certainly have regarded as a sellout. Luckily for him and for Britain, the plan did not materialize because Mrs. Merkel did not deliver, so he had no choice but to use the veto, which he did.

In France, the British Prime Minister’s veto led to an outburst of undignified name-calling. President Sarkozy described him as a “stubborn child.”[32] The French Finance Minister said that Britain was “marginalised” and attacked the coalition government’s economic policy. The Governor of the Bank of France called for Britain’s sovereign credit rating to be downgraded rather than that of France.[33] In Britain, the Liberal Democrats expressed various degrees of dissent from the Prime Minister’s veto.

Deputy Prime Minister Nick Clegg first supported it, then criticized it, then modified his criticism. He absented himself from the House of Commons while Mr. Cameron justified himself.[34] Finally, he let it be known that on future occasions, he would attend such summits and conduct his own diplomacy.[35] By contrast, the Prime Minister was lionized by his own party in and out of Parliament. In the country, opinion polls showed overwhelming approval of his stance, and the Conservative Party achieved a significant lead over the Labour Party in an opinion poll.[36]

It is not yet clear where the euro zone, the European Union, or Britain goes from here. First, the Brussels diplomatic débâcle served to obscure how little progress was made by the euro-zone countries in resolving their own crisis. Commentators and markets have remained unimpressed by schemes that, in essence, center on reviving the now widely discredited approach of the Maastricht Treaty’s Stability and Growth Pact without the European Central Bank adopting a much more active role in support of—and lender of last resort to—euro-zone member states.

Second, the European Union itself looks increasingly artificial—a framework of arrangements that emerged out of past events and (more or less) suited past requirements but no longer corresponds to today’s global realities. The EU contains too many contradictions and states with too many incompatible interests to stay as it is. There has to be parting of several ways. One way or another, such a parting will certainly and crucially involve Britain.[37]

For political reasons, the Prime Minister is desperate to avoid any decisive shifts in the compromise policies adopted by the coalition. He fears that a referendum on Britain’s future relations with the EU, demanded by much of his party and (as polling data show) desired by most people in the country, would open the road to Britain’s exit and, more immediately, also precipitate the collapse of his alliance with the Liberal Democrats. Nor is he willing to press for a significant repatriation of powers from the EU to Britain, despite his previous pledges to do so. He knows that in present conditions, he has no goodwill to use with—and insufficient weapons to use against—the euro-zone bloc and its hangers-on (though, of course, there is still a possibility that several countries may shy away from the new fiscal union proposals when once the full details emerge).

Mr. Cameron would clearly prefer to continue the indeterminate policy he was pursuing before Brussels, yet this may not be viable. Other things being equal, Britain would clearly benefit from a resolution of the crisis in the euro zone. On the other hand, Britain’s ability to influence events is extremely limited. It cannot, for example, afford to collaborate in large bailouts, whether through the IMF or otherwise. Its main focus has to be on preserving its own economic interests. But is this possible without fundamental change?

Decisive in making that assessment will be how Britain now fares in ensuring that the European Single Market provisions are not used against its economic interests. This goes to the heart of a long-standing complaint. But if a tightly controlled bloc of euro-zone members and others, deciding as a caucus, effectively uses European institutions and mechanisms to outvote Britain on a regular basis, the country’s position will become impossible.

The immediate matter of dispute—and the one that precipitated the Cameron veto, on which Britain cannot afford to compromise—is taxation and regulation of the City of London. It is a battlefield that the government would certainly rather not have chosen. That is partly because, as an element of its “fairness” agenda, it has spent much time chastising financiers for their alleged misdeeds in the run-up to the banking crisis and recession. At the same time, a core element of European (and particularly French) ideology is that the root of all current problems is the excessive exuberance of unregulated Anglo–Saxon capitalism.

The Europeans will thus pursue this particular vendetta with relish. Significantly, in the wake of the veto, the EU’s Economic Affairs Commissioner, Olli Rehn, commented: “If [Britain’s] move was intended to prevent bankers and financial corporations of the City from being regulated, that’s not going to happen.”[38]

The economic facts speak for themselves, and they show that Britain cannot afford to see the City strangled.[39] In 2009–2010, the U.K. financial services sector made a tax contribution of £53.4 billion—11.2 percent of total tax receipts—to the Exchequer. Financial services accounted for a £35.2 billion trade surplus. Although it is fishing and agriculture that are always mentioned in domestic political discussion of powers abandoned to Brussels, these two sectors now account for just 0.7 percent of U.K. GDP. Financial services, by contrast, account for at least 10 percent.

In the past, there was a more balanced trade-off between accepting regulation from Europe and gaining access to European financial markets. London both influenced regulation within European countries and acted as the main entry point to the EU’s single market in financial services. In current and likely future conditions, with the depressed outlook in the euro zone, British business—including financial business—will increasingly look elsewhere.

Accepting burdensome rules motivated by an increasingly hostile attitude to financial services as such becomes much less attractive. At least 49 new EU regulatory proposals affecting the City are either in the pipeline or being discussed. Notable specific threats are a proposed EU-wide financial transaction tax, possible short-selling bans, and the European Central Bank’s insistence that transactions in euro-denominated financial products be cleared within the euro zone rather than in London.

More generally, and irrespective of the agonies of the euro zone, Britain clearly needs to rethink from scratch its relations with the European Union. This is an historic opportunity as well as an obvious necessity.[40] Such a review needs to take account of non-European opportunities as well as European-focused problems. The fact that the Liberal Democrats in the coalition will oppose it by all possible means may well suggest an early election—which also, of course, would allow the Conservative Party to rectify its economic program in the light of events and with a view to putting economic growth through supply-side reform at the head of a new mandate.

Section VI

The Future

A fundamental rethinking of Britain’s relations with Europe is something that should be welcomed rather than, as hitherto, discouraged by the United States. The U.S. has its own large problems. Like Britain, it cannot do much to help solve Europe’s. But in the years ahead, it should be a priority in Washington to reset U.S. relations with Europe. That reassessment will need to take into account the economic potential and stability of individual countries, not just treat all alike.

The assumption that has governed the U.S. view of European developments more or less since the Treaty of Rome in 1957—that countries will move, albeit at an uneven pace, toward “ever closer union”—no longer applies. Whether Europe splits into different currency zones, or countries reissue their own currencies, or some other new geometry of relationships emerges, nothing can ever be the same again after the euro-zone crisis. Moreover, whatever the shape of Europe that finally emerges over the next few years, the U.S. will be better served by having a British ally that is financially stable, economically prosperous, unencumbered by onerous obligations to support unsustainable arrangements in Europe, and clear about its priorities and its position in the world.

As for the immediate prospects for the U.K. coalition government, these will be determined by two short-term and two long-term factors. In the short term, it is not at all clear how the traditionally Euro-enthusiastic Liberal Democrats can be rallied to what amounts to a bitter war of attrition against the euro-zone core in defense of British interests. If they cannot, and despite the technical problem presented by the coalition’s Fixed-term Parliaments Act, an early election could result.[41] The other short-term factor pointing in the same direction is the increasingly fragile position of Labour Party leader Ed Miliband, whose poor ratings might tempt Mr. Cameron—and certainly do tempt his backbenchers—toward an early poll.

An interesting opinion survey from last autumn is also relevant here. This suggested that in a referendum on EU membership, 49 percent would vote to leave against 40 percent who would vote to stay. This shows the depth of popular disillusionment with Europe, on which a Euro-sceptic Tory Party could draw. The same survey demonstrated, even at a time when Labour was four points ahead of the Conservatives (now reversed), that by 37 percent to 26 percent, voters preferred Mr. Cameron and Mr. Osborne to Mr. Miliband and his Shadow Chancellor, Ed Balls, to manage the country’s economic affairs.

In the longer term, the two determining factors will be, first, the state of the economy—if there is no sustained improvement at least a year before the pencilled-in 2015 election date, the coalition parties will probably lose, whoever leads Labour—and, second, a possible intriguing, if intangible, long-run change in attitudes. This is the sort of thing to which political pragmatists, like those in charge of the three main parties, habitually attach small importance. But such transformations, as was demonstrated with the shift under Margaret Thatcher in the 1980s against socialism and in favor of small-government individualism, can be seismic.

A recent report from the National Centre for Social Research suggests that, under pressure of economic austerity, underlying “Thatcherite” values in Britain may have resurfaced. Its British Social Attitudes Survey found a shift in sentiment against greater government intervention to rectify inequalities; a reduction in popular hostility to private health and education; a marked drop (to less than a third) in the number of people favoring tax rises in order to improve public services; another notable drop in the number willing to support high taxes to protect the environment; and a clear majority view that unemployment benefits were too high.[42]

This suggests a return to reality. Upon such changes—in whatever country they occur—conservative successes may be built. It remains to be seen whether they will be.